BP Didn't Reshuffle Boxes. It Buried a Strategy.

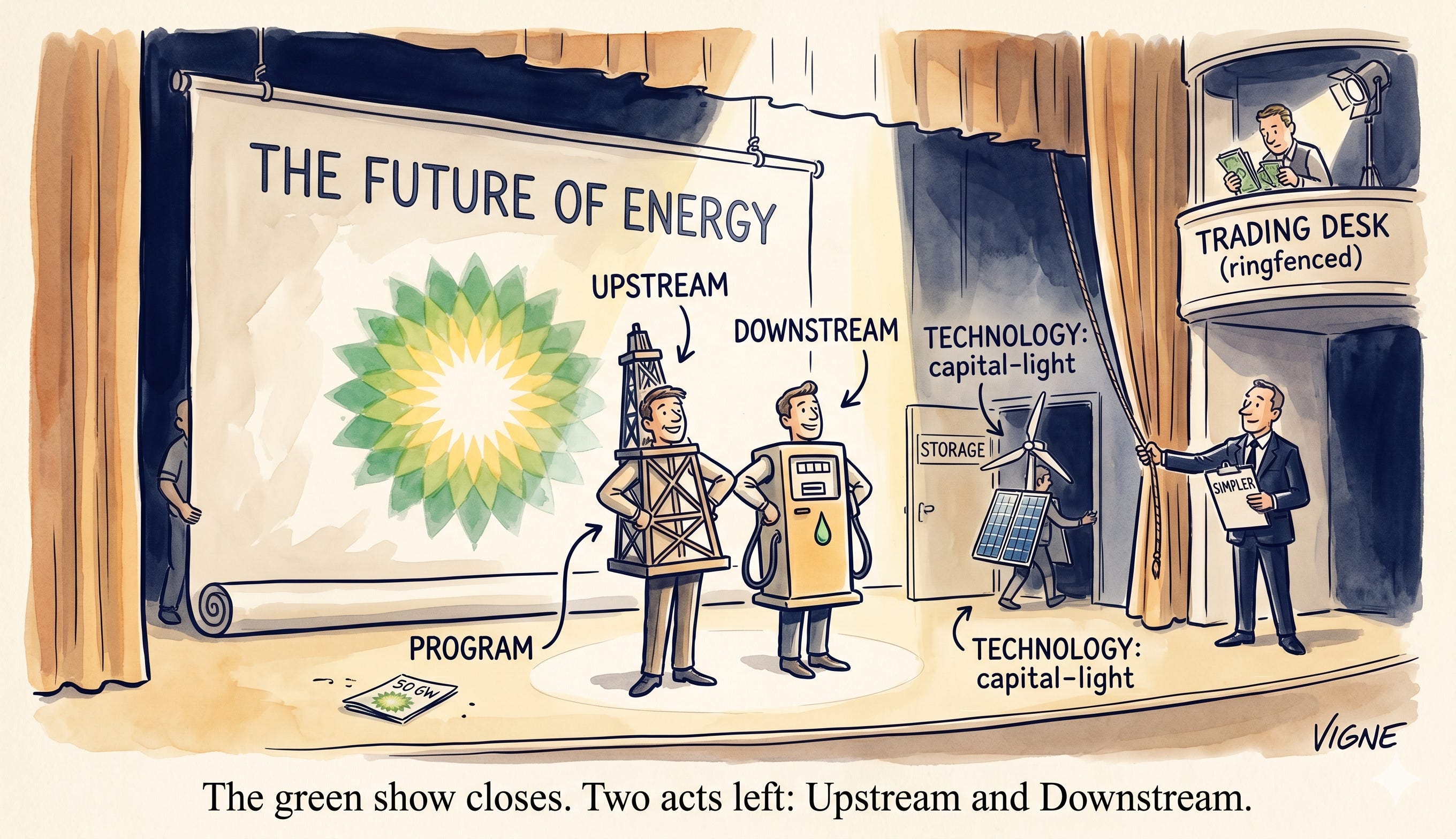

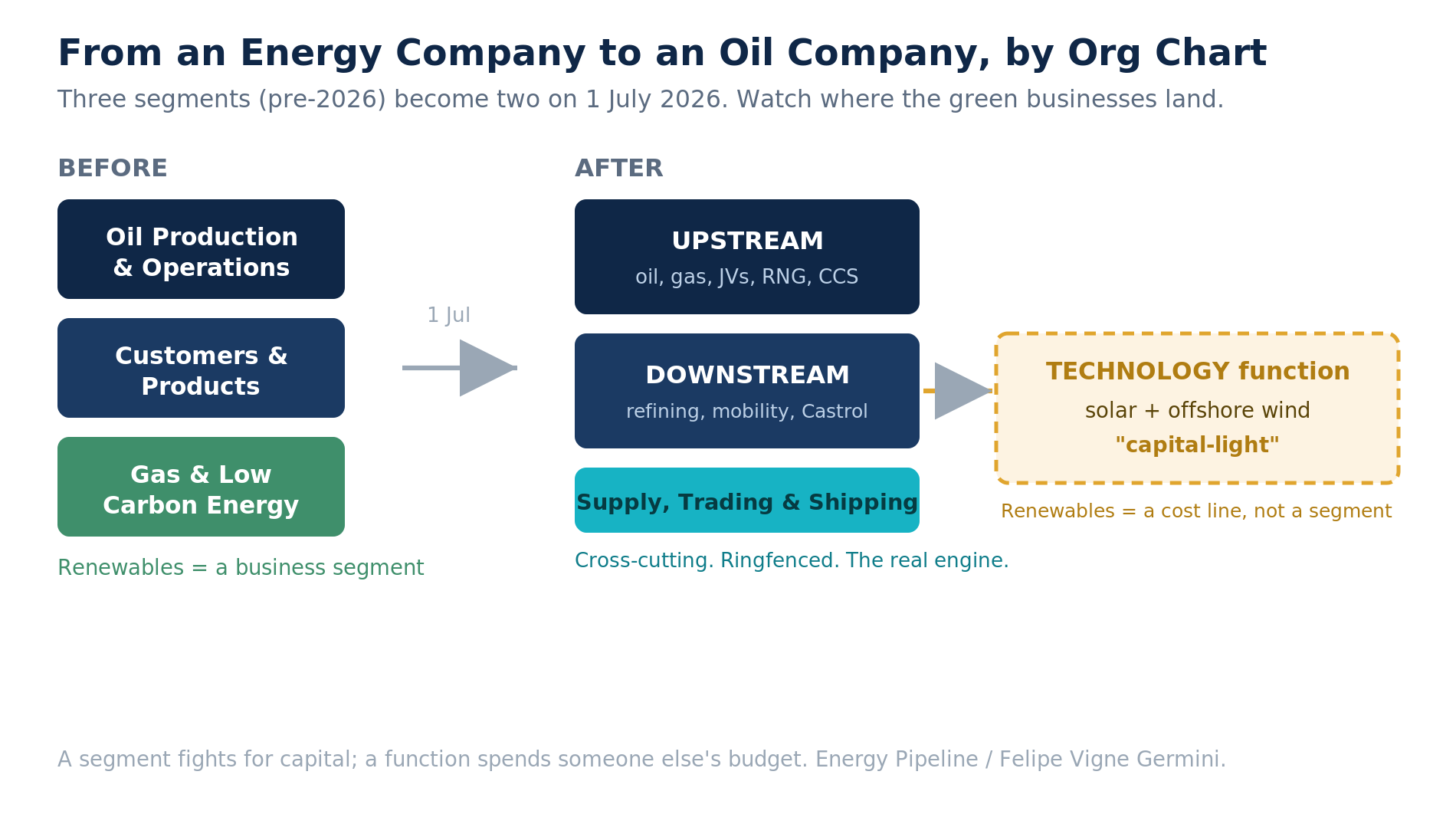

Three segments become two on 1 July. Solar and offshore wind get folded into a "Technology" function on a capital-light model. Read the org chart as a confession, then ask the question that matters.

BP announced a reorganization this week and the market filed it under housekeeping. Three business segments collapse into two, Upstream and Downstream, effective 1 July. Cleaner reporting lines. Fewer committees. A simpler company, the press release says.

I read it differently. An org chart is where a company tells you what it actually is, after the slides stop pretending. And this one says something the investor decks have been dancing around for five years.

The names give it away. Upstream and Downstream. That is the structure of an oil and gas company. It is not the structure of the “integrated energy company” BP sold the market in 2020, the one that was supposed to grow renewables twentyfold and shrink the barrel. That company is being quietly dismantled, and the dismantling is happening through plumbing, not through a podium.

The validation hook: the capital already confessed

You did not need this week’s announcement to see where BP was going. The capital told you in February 2025.

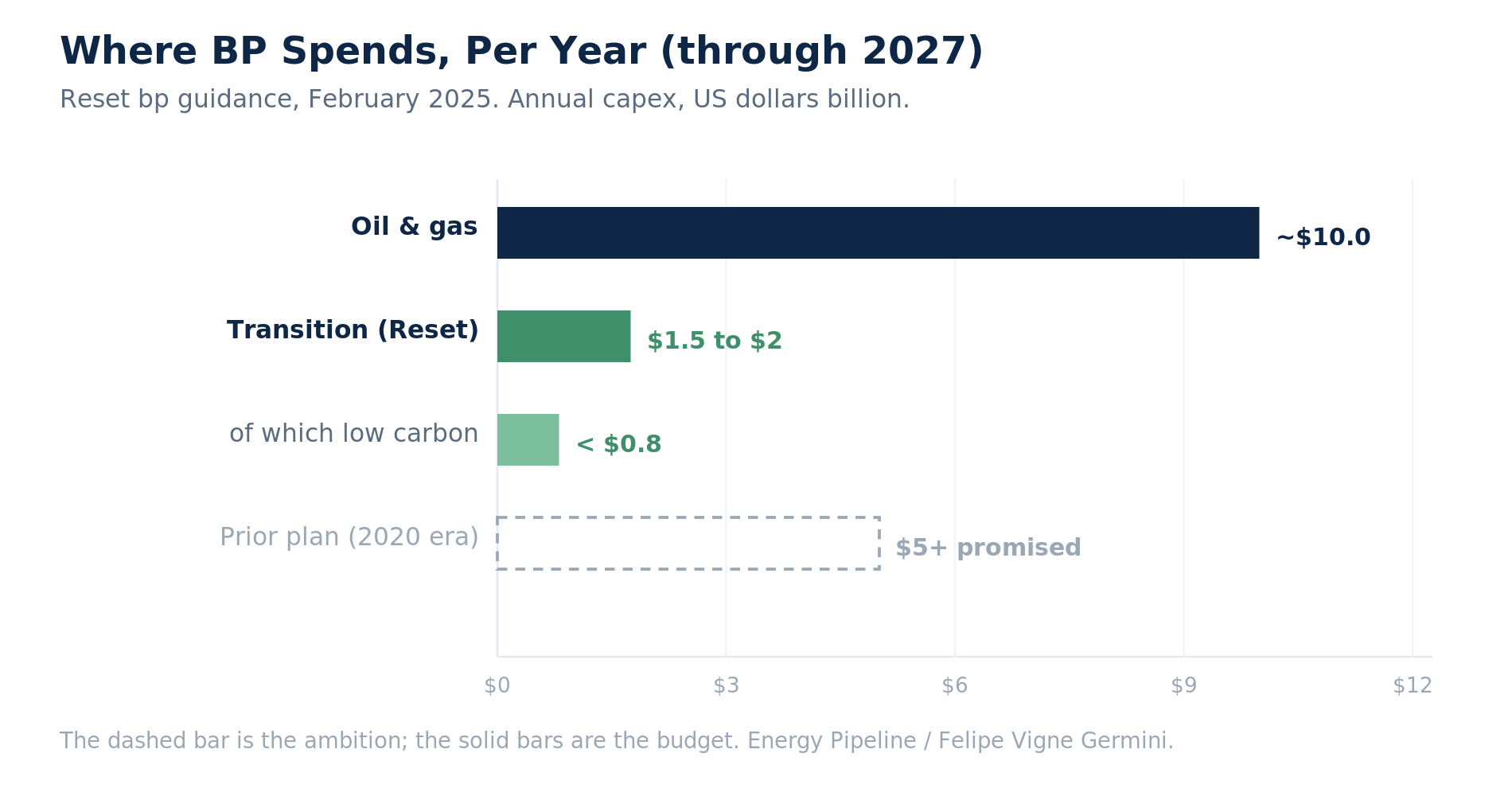

The Reset bp strategy cut transition investment to between $1.5bn and $2bn a year, more than $5bn a year below the prior guidance. Low carbon capex was pushed below $0.8bn a year. Oil and gas investment went the other way, up to roughly $10bn a year. Total capex was capped at $13bn to $15bn through 2027. The 50 GW renewables target, the headline number of the entire 2020 thesis, was scrapped outright.

So the money had already moved. What was left was the architecture, still carrying segments and reporting lines built for a strategy that no longer had a budget. This week the architecture caught up. The reorg is not a new decision. It is the org chart finally agreeing with the cash flow statement.

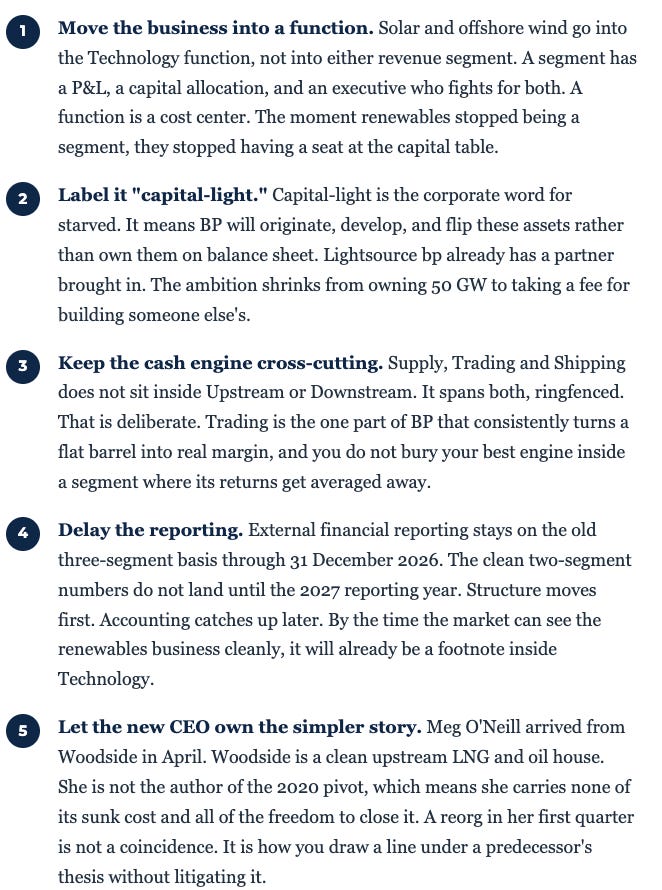

When a business loses its own segment, it loses its own capital. Solar and offshore wind did not get reorganized. They got demoted from a business to a line item.

How a reorg euthanizes a strategy without a funeral

Walk the mechanics the way you would walk a divestment, step by step, because each move sets up the next.

Five moves, one outcome. The integrated energy company becomes an oil and gas company with a world-class trading desk and a small green options book it can sell down whenever it needs cash.

Exhibit 1. The structural demotion. Renewables move out of a revenue segment and into a corporate function, which is where capital ambitions go to be managed down.

Follow the capital, not the slogan

The cleanest way to see a strategy is to watch the money, because budgets do not give interviews. BP’s 2020 plan pointed transition spending toward roughly $5bn a year and beyond. The Reset cut it to a fraction of that. Oil and gas now takes the lion’s share of a shrinking capital pot.

Here is the gap between what was promised and what is funded.

Exhibit 2. The capital confession. Transition spending was cut by more than $5bn a year against the prior plan, while oil and gas climbed to roughly $10bn. The 50 GW target was scrapped.

Where the renewables went, in one trajectory

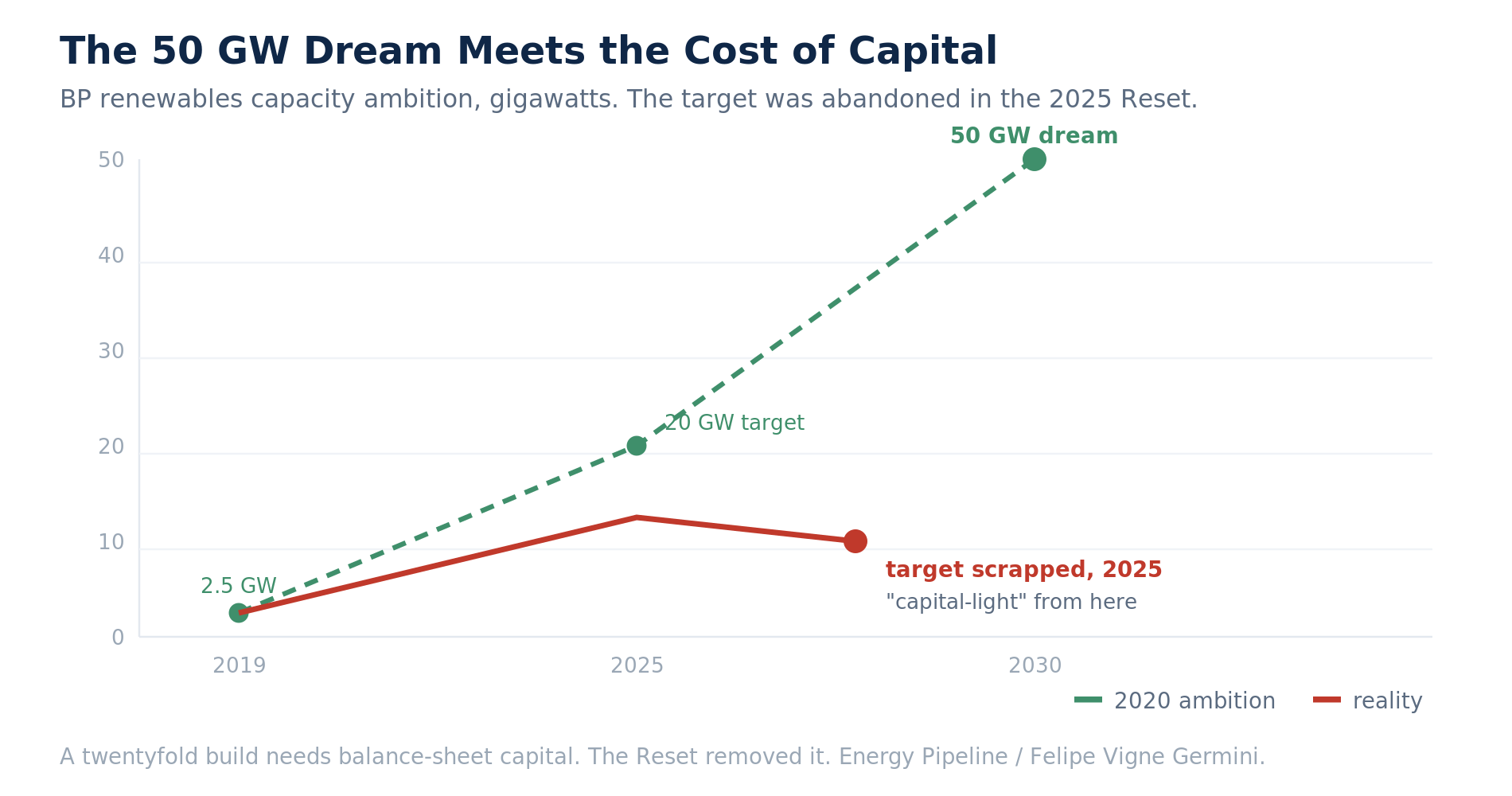

In 2019 BP had about 2.5 GW of renewables. The 2020 plan called for 20 GW by 2025 and 50 GW by 2030, a twentyfold build. It was the most ambitious decarbonization pledge any oil major had put its name to. Then it met the cost of capital, the return on a wind farm versus the return on a barrel, and the patience of an investor base that never bought the premise.

The fair counter-argument deserves a hearing. Capital-light may be the disciplined call, not the cowardly one. BP tried to own 50 GW on an oil major’s cost of capital, and that math never closed. Originating projects and selling them down for a fee is arguably the only sane way an oil balance sheet should ever have touched offshore wind. I take the point. I still call it a retreat, because the company that made the 2020 promise is not the one keeping it, and the capital vote is not ambiguous. Discipline and retreat can be the same move. An honest reader should hold both.

Exhibit 3. Ambition versus reality. The green line is the 2020 pledge. The red line is what the capital allowed. The reorg simply files the green line where it can no longer ask for money.

The engine they ringfenced

The detail most readers will skip past is the one I would circle in red. Supply, Trading and Shipping stays cross-cutting, spanning both new segments rather than sitting inside either one. That structure is a choice, and it tells you what BP values.

Trading is where a major turns a commodity it cannot control into a margin it can. It is the part of BP that out-earns the index in a flat market, the part that monetizes the optionality in a global system of cargoes, storage, and arbitrage. You do not fold that into Upstream, where its returns would be averaged against a depleting field. You ringfence it. You let it run across the whole book. O’Neill is protecting the one engine that consistently beats the cost of capital while she manages everything else for cash.

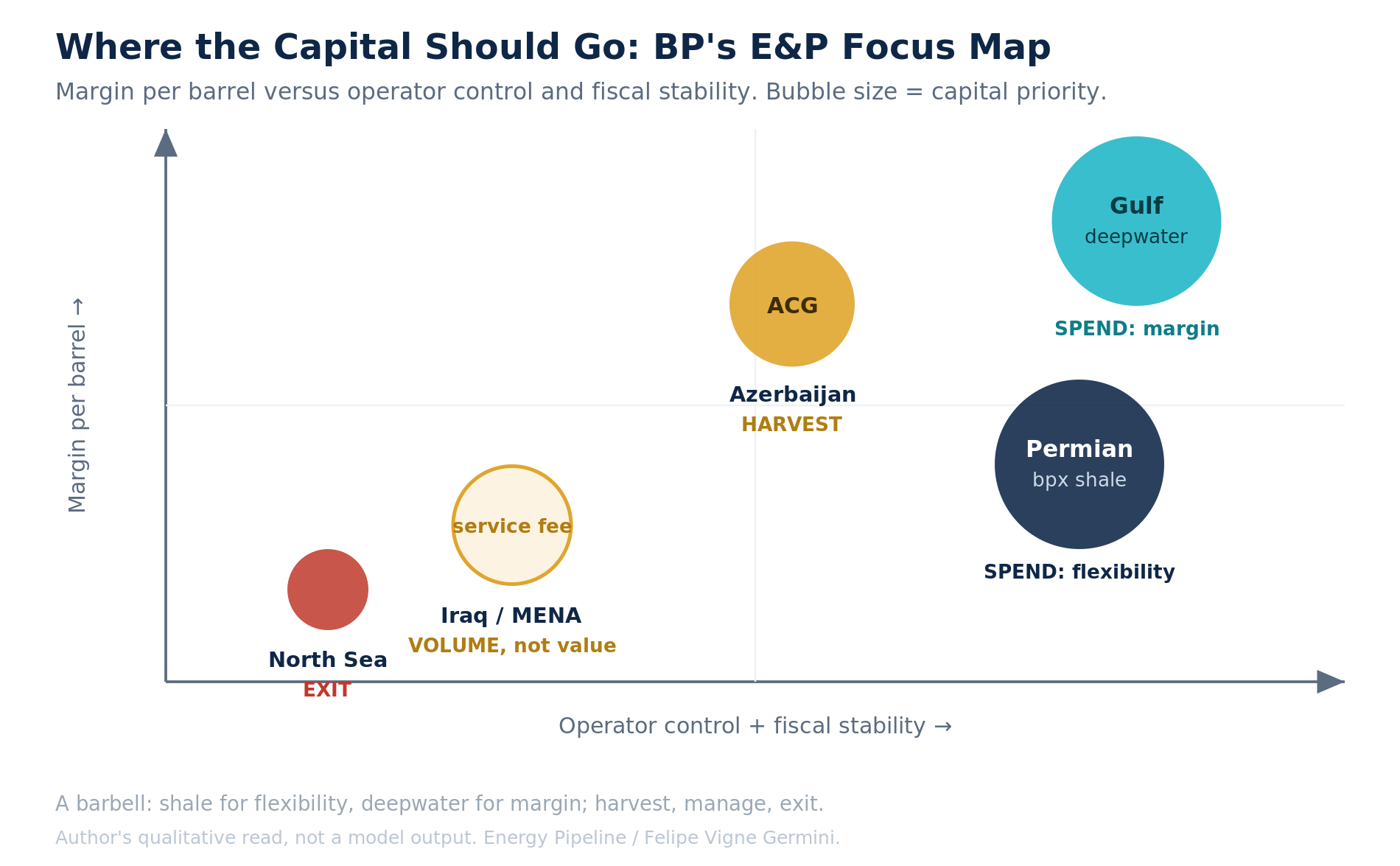

Where the barrels actually earn: a map for the new Upstream

A reorg into one Upstream segment is only as good as the discipline behind it. One executive, Gordon Birrell, now owns the oil and gas. He has about $10bn a year and a finite number of rigs. The press release does not answer the only question an operator cares about. Where does that capital go.

Run BP’s E&P portfolio the way you high-grade a drilling program, by breakeven, by operatorship, and by how stable the fiscal terms are. Do that and the portfolio sorts itself into a barbell.

One end: short-cycle US shale. bpx Energy pumped north of 430,000 barrels of oil equivalent a day in 2024 and is guided toward 650,000 by 2030. Shale is the dial. You can add a rig or drop one inside a quarter, which is why it is where a cash-focused major parks the capital it wants to keep flexible. Not glamorous. Liquid, in both senses.

The other end: advantaged deepwater in the Gulf of America. This is the crown. Mad Dog, Atlantis, Thunder Horse, and now Kaskida, BP’s sixth operated hub there. Tieback economics into existing infrastructure carry some of the lowest breakevens in the portfolio, the barrels are operated so BP sets the pace, and the fiscal regime does not get rewritten after an election. The Atlantis expansion that came on at the end of 2025 added production through subsea wells tied to a platform that is already paid for. That is how you make a high-margin barrel without betting the balance sheet on a new platform.

The cash cow in the middle. Azerbaijan, the Azeri-Chirag-Gunashli complex, is an operated machine BP has run for a generation. It still throws off cash, but it is past its peak and it rides a single export artery, the Baku-Tbilisi-Ceyhan line, through a region that is not quiet. You harvest it. You do not pour growth capital into it.

The volume that looks like value and is not. Iraq, the Rumaila supergiant, is enormous, and BP’s economics there run through a technical service contract. BP collects a fee per incremental barrel. The state keeps the upside. Rumaila is a production number, not a margin engine, and the new Upstream should be honest with itself about the difference. Libya, now re-entering, carries the same volume-over-value caution with a security discount on top.

The exit. The UK North Sea is a mature basin wearing a punitive tax. With the windfall levy stacked on the standard regime, the marginal barrel earns the Treasury more than it earns the operator. BP already sold Culzean and holds much of what is left through a minority stake in Aker BP rather than on its own books. That is the right direction. The North Sea is where a disciplined Upstream stops spending and starts leaving.

So the focus map is not complicated, which is the point. Two engines, the Permian for flexibility and the Gulf for margin. One cash cow to milk, Azerbaijan. One volume play to manage for what it is, the Middle East. One basin to exit, the North Sea. A company that concentrates there, and farms down the scattered non-operated positions that earn neither control nor margin, has actually decided what it is. A company that keeps a little of everything is just an oil major that has not finished the reorg it announced.

Exhibit 4. The focus map. The two engines sit on the right where BP operates and the fiscal terms hold. Iraq and the North Sea sit bottom-left, where the barrel earns the state or the Treasury more than the operator.

The reporting lag is the quiet part

Structure changes on 1 July. External reporting does not. BP keeps publishing on the three-segment basis through the end of 2026, with the new two-segment framework starting in the 2027 reporting year. So for roughly eighteen months the market runs the company on one map while management runs it on another.

That gap matters for anyone trying to value the pieces. By the time clean two-segment numbers arrive, the renewables business will already be inside a function, with no standalone P&L for the market to scrutinize. The transition is being completed in the dark period between structure and disclosure. Tidy.

Exhibit 5. The disclosure lag. The strategic question gets resolved in the window between when the structure changes and when the numbers have to show it.

The other half of the story: selling the furniture

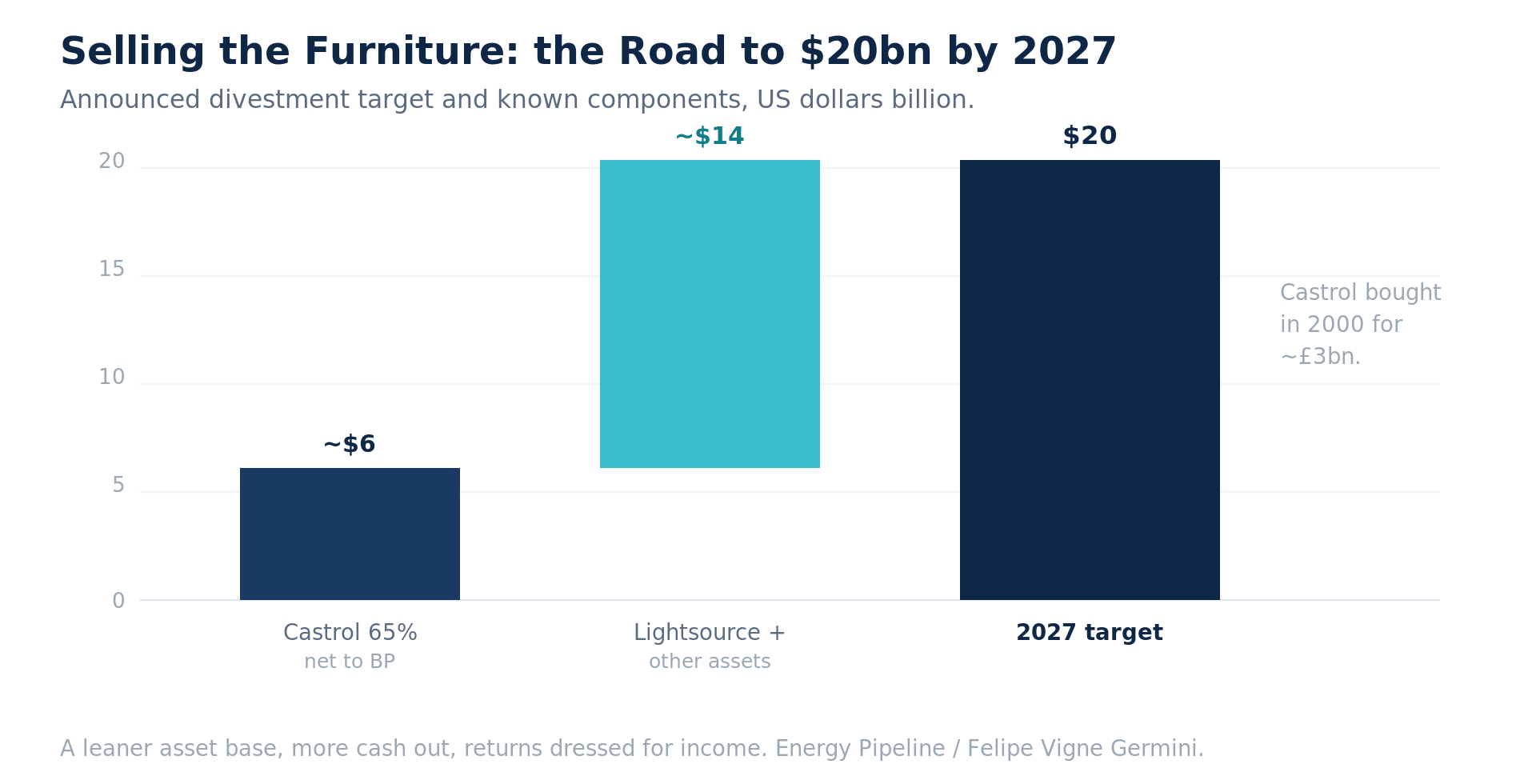

A reorg toward Upstream and Downstream runs alongside a balance-sheet cleanup. BP is targeting $20bn of announced divestments by the end of 2027. The marquee move is Castrol, the lubricants business BP bought in 2000 for around three billion pounds. BP agreed to sell a 65% shareholding to Stonepeak at a $10bn enterprise value, with net proceeds to BP near $6bn. Lightsource bp, the solar arm, takes in a partner. The list goes on.

Downstream is the question I am parking for another piece. Whether the refining, mobility, and biofuels book is worth keeping or grooming for its own sale deserves a full analysis, not a paragraph. For today the point is narrower. The cash these sales raise funds buybacks and deleveraging. It does not fund growth. This is not a company building the future. It is a company grooming itself for yield, aiming free cash flow up more than 20% a year to 2027 and returns on capital above 16%.

Exhibit 6. The cash harvest. Castrol anchors a $20bn divestment program that funds buybacks and deleveraging, not growth.