Hormuz reopens. The system has already moved.

Why the consensus trade on the Iran framework is right on direction and wrong on what happens after.

The trade looks clean and the trade is wrong.

The consensus this week is on the screen. Spot Brent at eighty dollars a barrel by year-end if the Strait of Hormuz normalizes by June. Major Western banks and consultancies have put the number on paper. Bank desks circulated the call. Trading floors ran the math against their forward books and started taking risk off. The President said talks with Iran were in the final stages. Brent sold off five percent in a session.

The trade is right on direction. A framework with Iran does compress the war premium, Iranian barrels do start returning, and tactical Brent does fall. It is wrong on what happens next. The trade assumes the system that gets re-opened is the system that existed before the closure. It is not. The market that absorbed sixty days of de facto Hormuz closure rebuilt itself around the disruption. Insurance markets repriced. Asian refiners signed term contracts they will not unwind. Freight architecture set a new baseline. The producer-side buffer shrank when the UAE left OPEC on May 1. Each of those changes is structural. Each is independent of whether Trump and Tehran sign a piece of paper next month.

I have spent the last week on calls with counterparties across three continents who are pricing this completely differently than the consensus suggests. Their conviction is not soft. It is operational.

What three voices on three continents told me this week

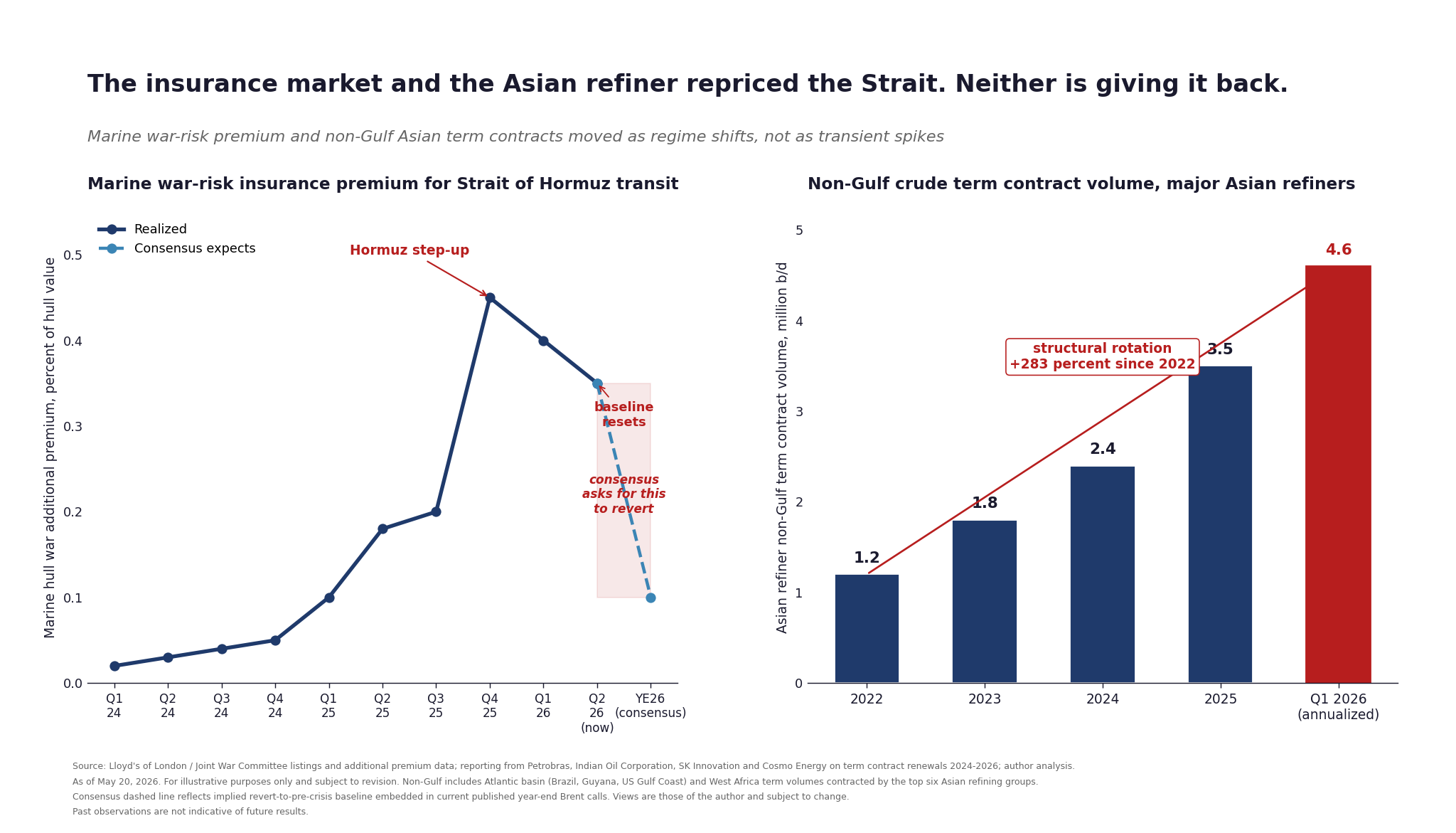

The first was a structurer at a Greek tanker house, the kind of name that quietly handles a significant fraction of VLCC term tonnage in the Gulf-Asia trade. His read, late last week: the war-risk insurance hull-and-machinery premium that spiked when Hormuz closed has now been internalized into one-year term TCE rates. Owners are not unwinding the premium even when the spot war-risk listing drops. They are pricing forward off the assumption that the next ninety days of premium revert, the four hundred days after that do not. The freight market has decided this is the new normal, regardless of what the diplomatic calendar says.

The second was a head of crude trading at an Indian refining group. Last month his group renewed long-haul term contracts with non-Gulf producers covering volumes through March 2027, locking in supply security at last cycle’s pricing. His framing: those contracts are not insurance policies he will tear up the moment Hormuz reopens. They are the new baseline of his supply book. The Asian refining complex has been actively rotating its supply geography for two years, and the Hormuz episode accelerated a structural shift the consensus is treating as a one-off detour.

The third is the read I have been getting from inside the Lloyd’s syndicates this week. The actuarial committee that resets the additional war-risk premium on June 16 will not give the spike back until it has seen four to six clean quarters of Strait transits without an incident. The London insurance market has priced the Strait of Hormuz as a regime change in the underlying risk distribution, not as a transient war zone. The deal-or-no-deal binary that the financial press has been running with is not the question London is asking.

Three professionals. Three continents. Same expected event. Three completely different reads on what comes after.

The mechanical chain, in four steps

The consensus path is the simple one. Strip it down and the mechanics run in four steps.

First, the war premium compresses. This part of the price was tactical, sentiment-driven, and built to unwind quickly. Roughly fifteen dollars of the current Brent strip is geopolitics that prices itself out in days, not quarters.

Second, Iranian barrels start returning. Per the IEA Oil Market Report (May 2026), the pre-sanctions Iranian export run rate was around 3.4 million barrels per day. The current sanctioned-and-shadow rate sits at 1.5 to 1.8 million depending on enforcement. A clean framework with a phased lifting could see incremental volumes of perhaps 500,000 to 800,000 barrels per day within the first ninety days, more over twelve to eighteen months as Kharg Island loading throughput recovers from its current sub-1 mb/d effective rate toward the pre-sanctions 1.6 to 1.8 mb/d range and counterparty risk normalizes.

Third, the insurance markets, term contracts, and freight architecture do not reverse simply because the underlying geopolitical trigger reverses. The Joint War Committee listing, marine hull war rates, and the additional war-risk premium that built into VLCC TCE between February and May have not been priced as transient. They have been priced as a regime shift.

Fourth, the producer-side cushion that would normally absorb a return-of-supply event is itself smaller. The UAE exit from OPEC on May 1 removed roughly 1.3 million barrels per day from the cartel’s 2027 effective spare-capacity forecast (the delta between the prior 3.8 mb/d forecast and the revised 2.5 mb/d, per the U.S. EIA Short-Term Energy Outlook May 2026). Returning Iranian volume into a system with reduced producer-side buffer is structurally different from returning the same volume into the system as it existed eighteen months ago.

Chart 1. Insurance and Asian term contracts: both repriced as regime shifts.

The trade map flows out of those four steps, not out of the headline.

______________________________________________________________________

This is for the trader who has watched a desk go directional on this week’s consensus call and has not yet decided whether to take the other side. Below the cut: the architecture frame on why this crisis lands differently than the seven previous geopolitical premiums that came and went; the pre-mortem on the three scenarios that would invalidate this view, with ranked probabilities including the OPEC+ compensation case the desk notes are not pricing; the dated calendar of six catalysts inside the next twenty-eight days; the trade map with four longs, three shorts, and the cleanest macro expression with explicit sizing rule; the operator-level call on which counterparty types are most exposed when the consensus trade unwinds; and the specific freight-vs-flat-price spread that captures the regime shift without taking directional crude risk.

Paid subscribers also receive this edition’s presentation pack, 10 slides covering the four-step mechanical chain, the freight repricing chart, the term-contract rotation map, the scenario matrix for Brent through Q4 under three Hormuz outcomes, and the trade map with positioning logic. Formatted for boardroom use and counterparty briefings.

Upgrade to read the full edition.