The Deep Dive: Brazil Has Swapped One Chokepoint for Another.

A working broker's note on why Russia at 91 percent of Brazilian diesel imports is the energy security story nobody in Brasília is pricing, and what the next sixty days look like if a single corridor

Brazil did not weather Hormuz. Brazil traded a Middle East shipping risk for a single-counterparty origin risk on a sanctioned trade lane, and Brasília has not yet treated the Russian share number as an energy security variable.

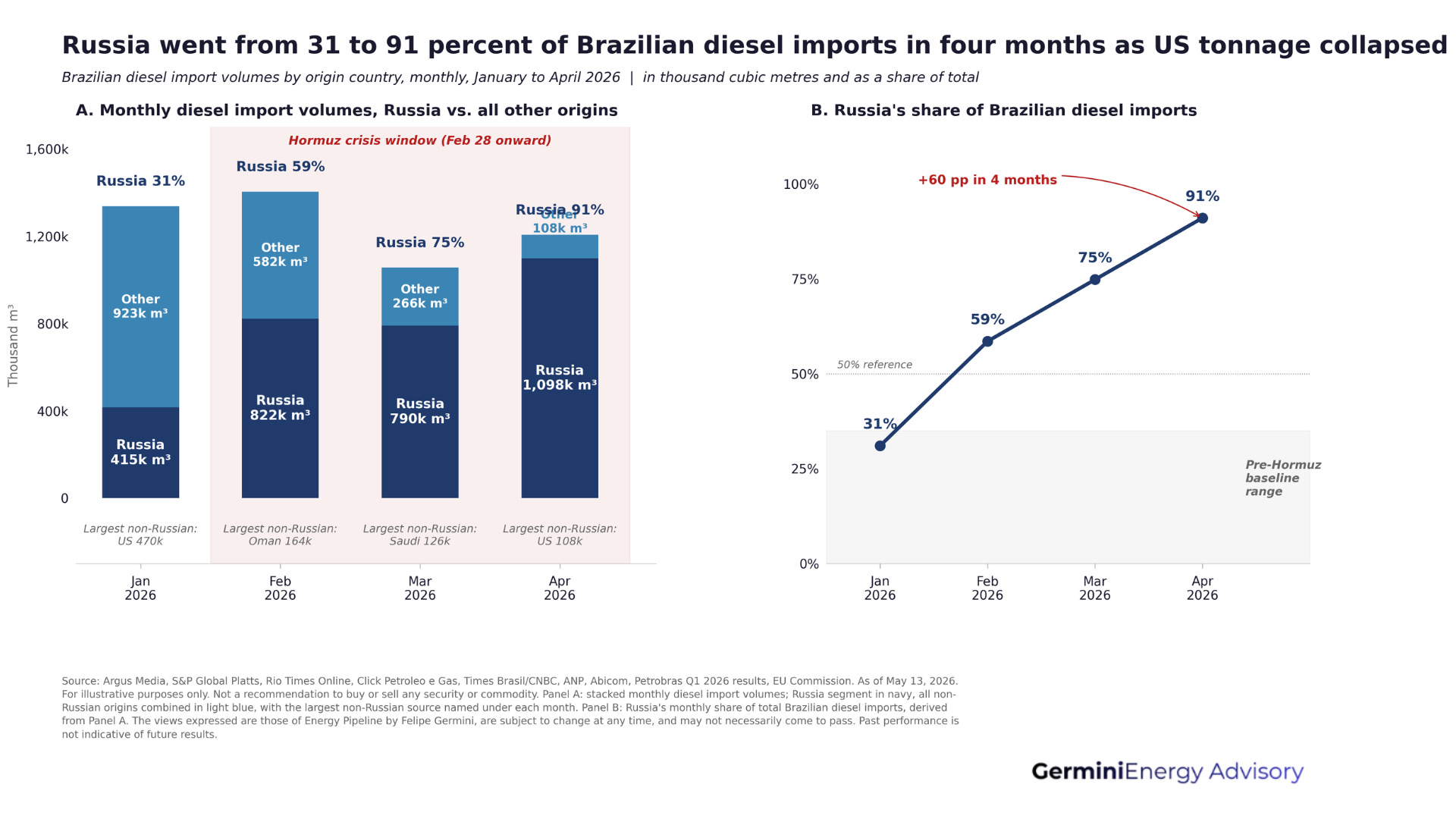

The numbers do not lie about this. In January 2026, Russia supplied 31 percent of Brazil’s diesel imports. The United States, mostly USGC tonnage, led the table at 35 percent, with the UAE behind at 18 percent. By April, Russia was at 91 percent. The US had collapsed to 9 percent. The UAE, Saudi Arabia, and Oman had effectively gone to zero. Volumes tell the same story: Russian-origin diesel went from 415 thousand cubic metres in January to 1,098 thousand cubic metres in April, while US tonnage fell from 470 thousand to 108 thousand cubic metres over the same window.

The pricing math behind that shift is specific, not abstract. Russian ULSD 10ppm FOB Novorossiysk has been clearing at roughly 12 to 15 dollars per barrel below ICE LSGO benchmark on recent term cargoes. Freight to Santos at recent Aframax spot rates sits at 28 to 32 dollars per tonne. Add insurance and demurrage and the all-in delivered price into Santos lands at a level that a private importer can absorb at the prevailing Petrobras gate price. USGC ULSD No.2, priced against Platts USGC and shipped on Suezmax tonnage to Santos at 38 to 44 dollars per tonne, does not. Northwest European cargoes priced against ICE LSGO plus freight do not either. So the compliant origins do not show up, and Russia does. The share goes from 31 percent to 91 percent in four months. That is not a slow shift. That is a regime change.

Chart 1. Russia went from 31 to 91 percent of Brazilian diesel imports in four months as US tonnage collapsed.

What the political math actually looks like

Three things have to be held together to read the present correctly.

First, Petrobras refining capacity ran flat-out through the Hormuz event and that absorbed roughly two-thirds of incremental demand. The startup of P-79, the Búzios 8 FPSO that delivered first oil on May 1 three months ahead of schedule, added 180 kb/d of upstream capacity. Refining throughput at ninety-five percent for the better part of two months kept the diesel pool fed. The Petrobras Q1 numbers, released on May 12, reinforced the operational story: a company hitting record production at 4.65 mboed, with pre-salt at 2.66 mboed. Two months at 95 percent throughput compounds the unplanned downtime risk on the FCC and hydrocracker lines. A REFAP or REDUC upset of even five percent of national capacity doubles the import shortfall on a week’s notice. The upstream story is real. The downstream pricing policy is borrowed time.

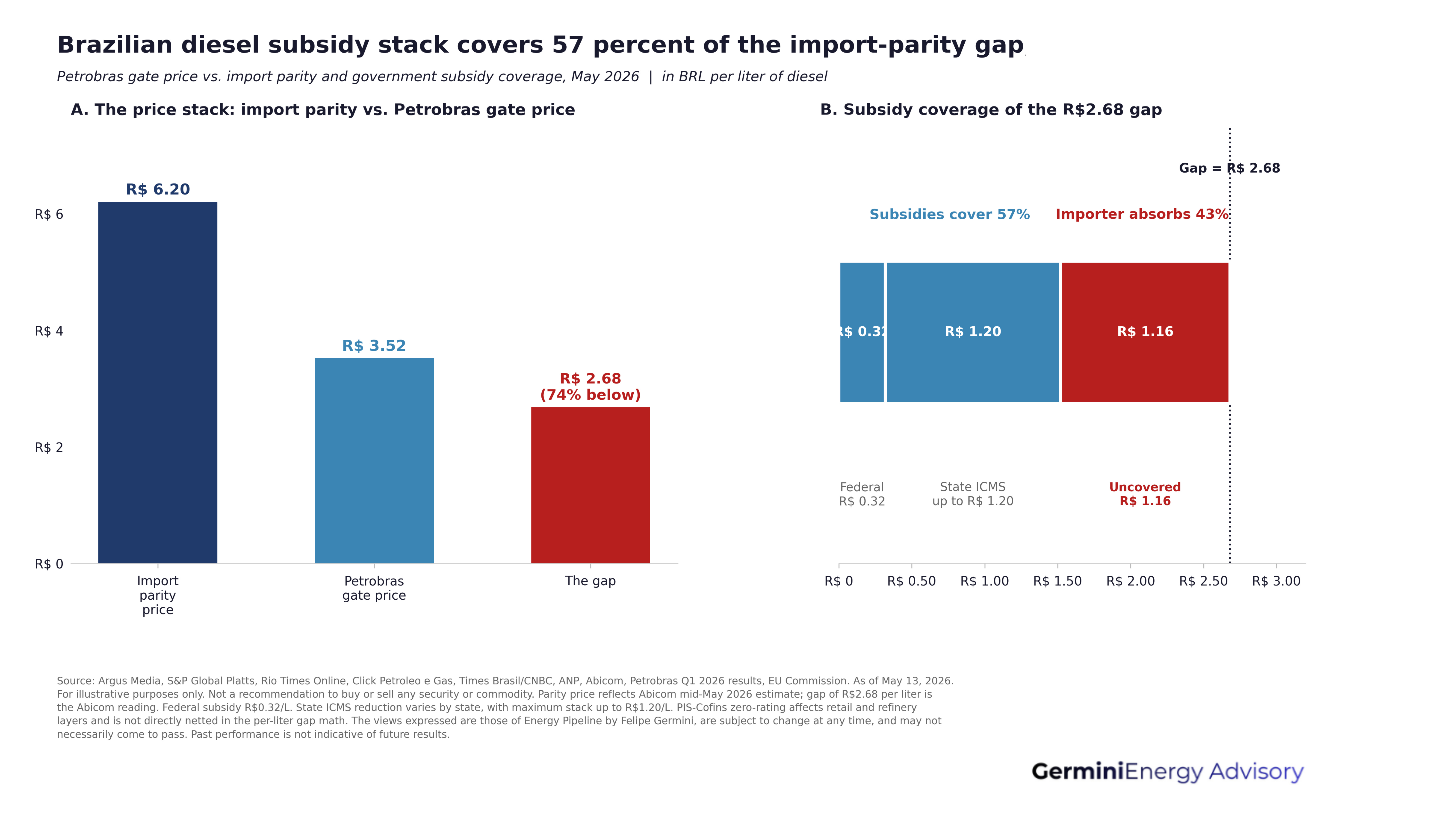

Second, the pricing policy gap blew out exactly when imports were most needed. Abicom has the defasagem at seventy-four percent, with Petrobras selling diesel at the refinery gate two reais and sixty-eight centavos per liter below import parity. To close that gap on a one-shot basis, the price at the gate would have to rise by two reais and fifty-two centavos. Petrobras has not done it. The reason it has not done it is that since 2023, the company has formally abandoned international price parity and adopted a domestic-cost criterion, which in practice means whatever the controlling shareholder wants the price to be that week.

When the gate price is two reais below import parity, the private importer that buys cargo on the international market and lands it at Santos is, by definition, losing money on every drop relative to the domestic offer. Either the importer takes the loss, the state pays the importer to take the loss, or the importer stops importing. The third option is the one that creates physical shortage. Rui Costa at Casa Civil has signed off on a federal subsidy of R$0.32 per liter, a state ICMS-reduction match worth up to R$1.20 in total, and a PIS-Cofins zero-rating on diesel that costs the Treasury something like R$20 billion in foregone receipts. Silveira at MME has handled the price dialogue with the Petrobras board. The Petrobras Pricing Committee decides when the gate moves. CONFAZ holds the ICMS lever state by state. Net coverage of the gap, in the best case stack: about R$1.52 per liter, against a gap of R$2.68. That math is not a small problem. The subsidy stack covers fifty-seven percent of the import-parity gap on a good day, and Abicom has been warning of desabastecimento risk for two months.

The largest private distributor, Vibra Energia, with BNDESPAR among its anchor shareholders, doubled its self-directed diesel imports for April after Petrobras cut its monthly supply quota. That is institutionally significant, not just commercial. A state-linked distributor stopped relying on the state refiner. The marginal barrel of diesel is no longer cleared through the Petrobras counter, and the political class has not yet treated the Russian share number as an energy security variable.

Third, and this is the part most commentators have skipped, the only origin that can profitably backfill that marginal barrel right now is Russia, because Russia is the only producer willing to sell product into Brazil at a discount to a depressed Petrobras gate. The refined diesel coming out of Russian refineries, sailing to Brazil under a mix of G7-flagged tonnage and shadow-fleet tonnage, lands in Santos at a price that the importer can absorb. Compliant origins do not clear at those numbers. So they do not show up. Russia does.

The corridor that fed the Brazilian truck fleet through Hormuz is now structurally Russian. That sentence should make every energy security desk in Brasília sit up. So far, it has not.

Chart 2. The Brazilian diesel subsidy stack covers only 57 percent of the import-parity gap.

Why the comfortable assumption is wrong

The assumption that comforts policymakers and most of the financial press is that diversification across many Russian counterparties, many vessels, and many ports of loading is a form of resilience. It is not. The corridor depends on three commercial conditions, any of which can be broken in under thirty days by an actor outside Brazil’s control. (1) The US Treasury sanctions architecture has to stay where it is. (2) The Russian refining base has to keep producing export-grade diesel at current rates. (3) The Brazilian political license to receive sanctioned-origin product has to hold.

The most misread of the three is the first one. The reflexive instinct is to point at Brussels and the EU sanctions sequence as the trigger. That instinct is geographically wrong. The European Union has issued twenty packages of sanctions against Russia, and the twentieth added 632 shadow-fleet vessels to a port-access ban that applies to EU ports and EU-resident services. Brazilian ports are not affected by that ban. A twenty-first EU package will come, but the European Union has no precedent for sanctioning a major Latin American economy on this kind of trade, and Brazil sits inside BRICS and outside the price-cap framework. The actual mechanism that compresses Brazilian flows is in Washington. An OFAC designation of a Brazilian-resident corporate facilitating shadow-fleet cargoes, or a secondary-sanctions enforcement action against a refinery destination on the corridor, would force the discount apart inside thirty days. The 2024-to-2026 OFAC enforcement pattern against intermediaries is consistent and well-documented. Operators who are reading the EU calendar for the trigger are reading the wrong calendar.

The second condition is the war economy. Ukrainian strikes on refineries inside European Russia have taken down meaningful refining capacity for weeks at a time over the past eighteen months. Russian product exports have been an adjustable variable in this conflict from the start. A serious strike on the Volga-Black Sea cluster, or a Russian decision to cap product exports in response to domestic gasoline pressure of the kind seen last summer, takes Brazilian-bound cargoes off the board first. Brazil is the marginal destination on the Russian product map because Brazil pays the smallest premium. That is precisely why Brazil is the first destination to lose volume in a stress event.

The third condition is political license. Roughly 250 G7-plus tankers and 150 shadow tankers were moving Russian crude and product in March. The Brazilian flow runs because most of it is invisible, on G7-flagged tonnage with insurance and legal cover. The day a vessel arriving at Suape turns out to be on an OFAC-designated hull, the politics get uncomfortable fast. None of the Brazilian distributors want to be the headline. The corridor is built on three commercial conditions, any one of which can be broken in less than thirty days by an actor outside Brazil’s control. That is not resilience. That is dependence under a thin disguise.

The argument against this thesis

The strongest version of the other side runs like this. Under a US administration that has treated Brazil as a hostile BRICS+ economy, with tariff threats and political pressure aimed at Brazilian commodity exports, US tonnage into Brazil is itself politically unreliable. A Brazilian importer looking at the corridor today might reasonably conclude that Russian concentration is the commercially rational hedge against a US administration that could pull supply on a political flashpoint. That is the steelman.

It does not survive contact with the freight curve. Spot Suezmax tonnage from the USGC to Santos has been pricing rich, not cheap, through April and May. If the market believed US-to-Brazil supply was structurally constrained for political reasons, the freight would have collapsed to attract Brazilian volume. It has not. It has done the opposite. The freight curve is the test, and right now the test says the US-unreliable hedge thesis is not what the market is pricing. The thesis also collides with the institutional reality that a Brazilian distributor caught on a sanctioned origin carries a higher reputational and regulatory tail than one carrying volume from an unfriendly but compliant origin. The argument deserves a seat at the table. It does not deserve the verdict.

This is for the Brazilian importer who knows the freight has held this far and is wondering when the corridor compresses, for the trader who watches LSGO cracks and freight forwards but has not yet asked which counterparty stops shipping first if OFAC moves, and for the capital allocator wondering where the directional trade sits.

Below the cut: the three-scenario matrix for Brazilian diesel supply between now and August reframed as market-implied versus our reading, the single Russian refining cluster whose downtime would force an emergency USGC tender within forty-eight hours, the directional trade box for capital allocators with size-and-stop framing, and the specific commercial calls a private distributor should be making this week.

Paid subscribers also receive this edition’s presentation pack, a twelve-slide deck covering the corridor map, the scenario matrix, the Russian refinery risk register, the directional trade box, and the Petrobras-versus-private-importer break-even chart, formatted for distribution at boardroom level.

Upgrade to read the full edition.