The Demolition List

OFF-CYCLE Edition: The White House just published the receipt for the most consolidated regulatory rollback since Reagan. Most of what matters is not what people are arguing about.

Reading the White House fact sheet as a contracts guy, not a pundit

The story is not ANWR. The story is the four-month permit.

Last Friday the White House posted what it called a fact sheet — eight pages of bullet points under the header Trump Administration Actions to Terminate Green Energy Regulations. Read it the way you would read a closing memo at the end of an M&A process, not as a press release, and what you are looking at is the most consolidated rollback of US environmental regulation since EO 12291 under Reagan in 1981. Every line is a completed action. Rescinded. Withdrawn. Terminated. Reopened. Slashed. The fact sheet is not the announcement of policy. It is the policy receipt.

What the document actually is

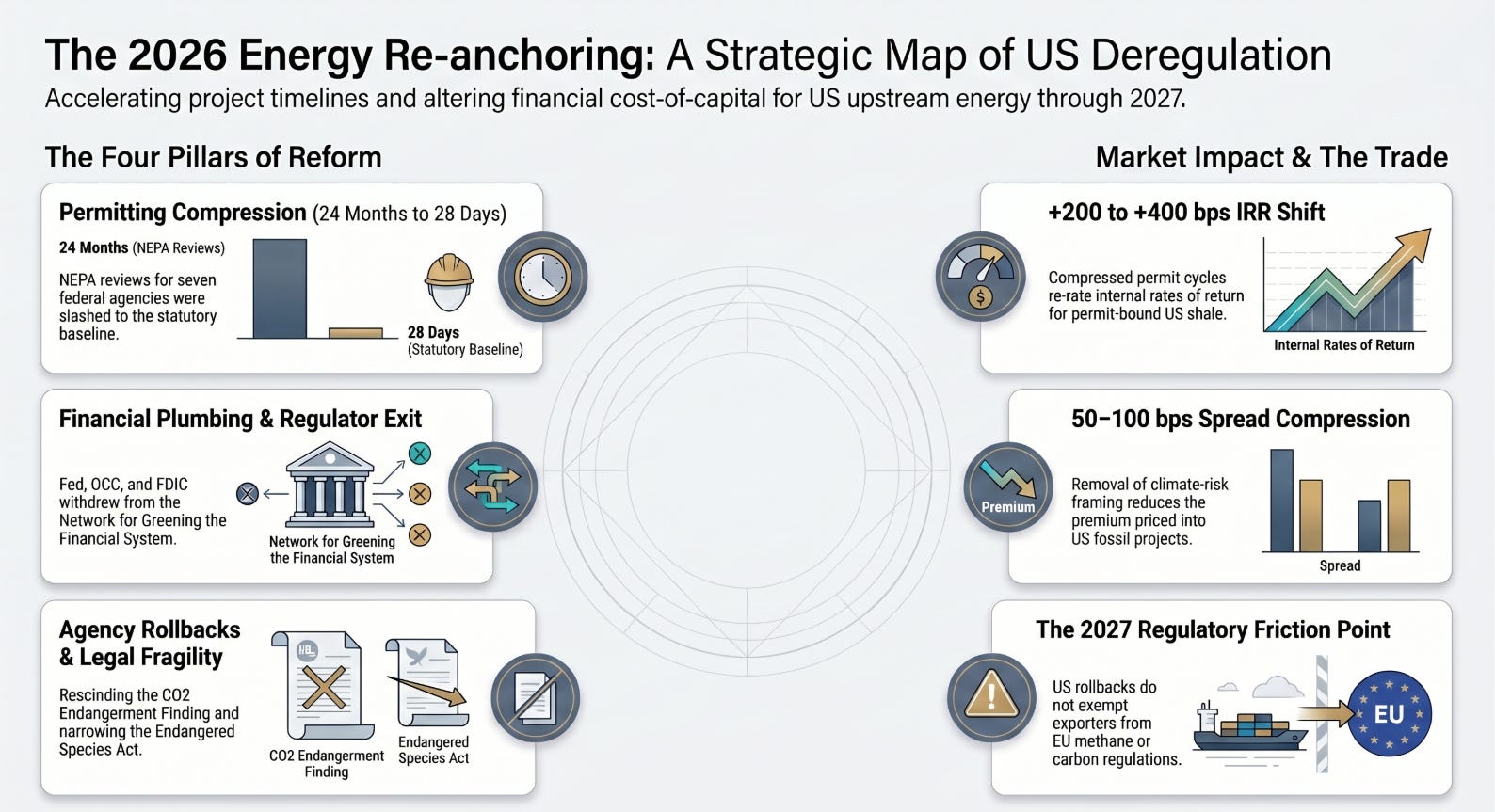

The Biden administration spent four years building an architecture. NEPA reforms with climate considerations baked in. The Endangerment Finding extended to power plants and to oil and gas operations. The Clean Power Plan 2.0. The OCS five-year leasing program reduced to three sales. The 2009 social cost of carbon embedded in every federal cost-benefit analysis. Bank regulators pulled into the Network for Greening the Financial System. SEC climate disclosure. CFTC climate risk unit. Cross-border transmission permitting layered with environmental review. Categorical exclusions reduced. Public lands restricted under the Public Lands Rule.

Most of that architecture is now gone. Not weakened. Gone.

The fact sheet inventories the demolition in plain language. The 2009 Endangerment Finding — the legal keystone that makes CO2 a regulated pollutant under the Clean Air Act — is being proposed for rescission. That is not a tweak. If it holds in court, it removes the administrative foundation under which the EPA regulates greenhouse gases at all. Massachusetts v. EPA gets reversed not by the Supreme Court but by the agency itself.

The UN Framework Convention on Climate Change and the IPCC are on the withdrawal list. Paris exit happened in Trump 1. Pulling out of the framework convention itself is the floor below that. The US is leaving the room where global climate negotiations happen, not just the room where commitments are signed.

Forty-seven DOE regulations slashed (per the fact sheet text). 101 new NEPA categorical exclusions at DOI. CEQ rescinded its NEPA regulations entirely. Seven federal agencies — USDA, DOI, DOE, FERC, Department of War, USACE, DOT, DOC — eliminated procedural NEPA requirements beyond minimum statutory baseline. The OCS five-year plan is being replaced. The federal coal leasing moratorium is over. NPR-A is reopened at 82 percent. ANWR’s Coastal Plain is back in play.

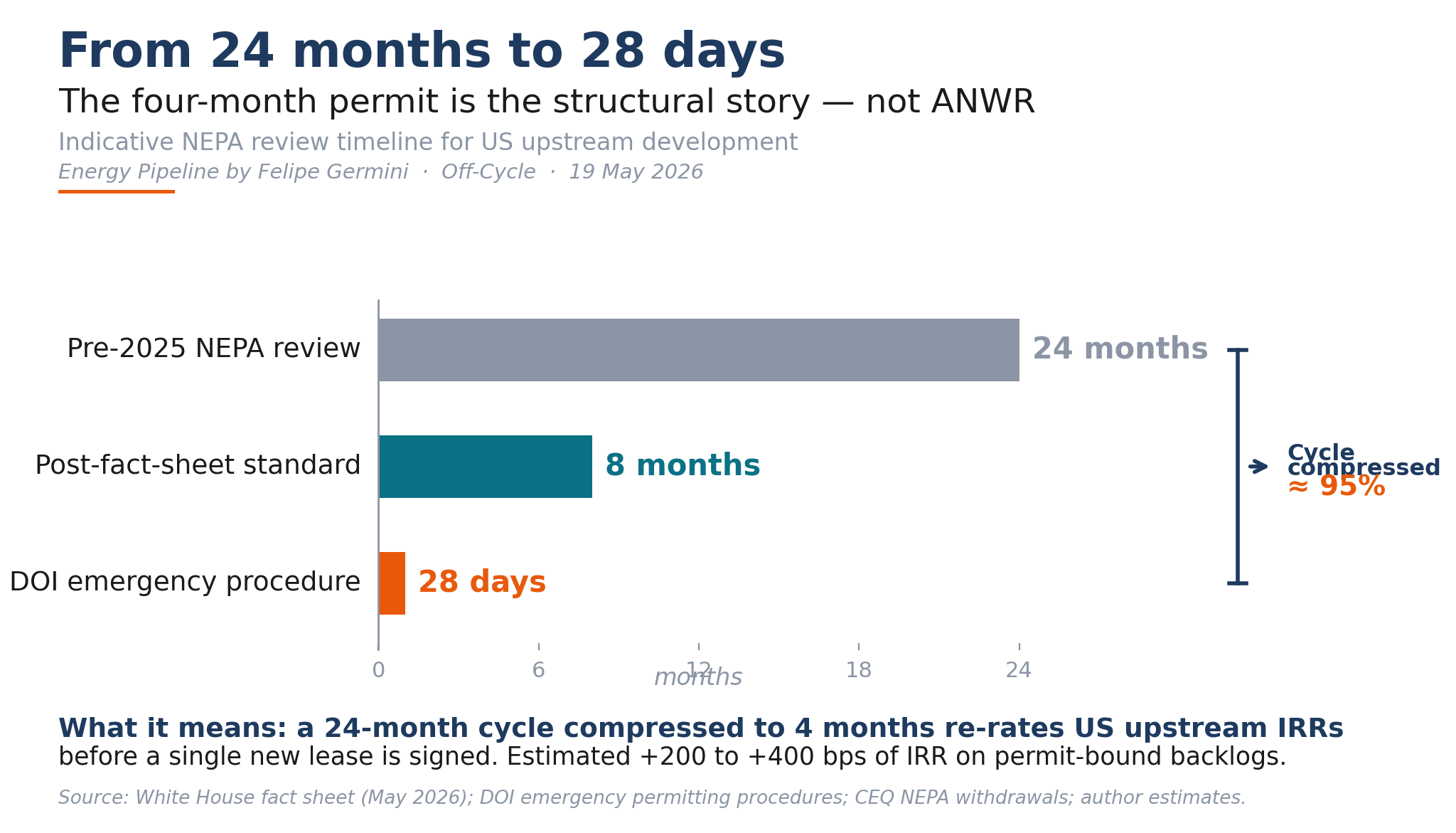

Chart 1 — Permitting Compression

Permitting compression is the operational story. Lease sales make headlines. Compressed permits change capital allocation.

What matters to operators and dealmakers

Strip out the political noise and the headlines about ANWR, and ask the question every operator asks: what changes the economics of a project I am actually working on?

The permitting compression is the real story. Multi-year NEPA review collapsed to 28 days under the DOI emergency permitting procedures. Cross-border transmission permits stripped of environmental and publication requirements, which the document says cuts review by six to twenty-four months. 101 new categorical exclusions under NEPA. The Council on Environmental Quality rescinded its NEPA regulations in February 2025 and let individual agencies write their own.

A two-year permit cycle compressed to four months is worth more, in pure project finance terms, than another twenty million acres of ANWR that nobody bids on. I have seen Permian independents with development backlogs gated by twelve-to-eighteen-month BLM permit waits. Compress that cycle by two thirds and the IRR on the same drilling program shifts by 200 to 400 basis points before a single rule on lease sales takes effect.

The Commingling Rule for multi-lease single-pad production is the kind of detail that gets ignored in summary coverage but actually changes how operators design field development plans. Multiple leases combined onto one well pad means fewer surface footprints, faster development, lower per-well costs. The kind of rule that makes a Delaware Basin operator save six months and twenty percent of capex per development project. Boring, technical, structural.

The Gulf of America carve-out from the Endangered Species Act is a quiet item that deserves more attention than it has received. Exempting an entire sedimentary basin from federal endangered species review for national security reasons sets a precedent. Whatever you think of the merits, that precedent will be used by future administrations in directions current proponents may not like.

Where this shows up in a book

For anyone who has to act on this, the trade has three legs. Long US independents with permit-bound development backlogs — Permian and Eagle Ford operators whose forward inventory is gated by NEPA timelines, not geology. Long the project-finance basis tightening — the spread between US fossil project bonds and comparable energy infrastructure paper in Europe should compress 50 to 100 basis points over the next twelve to eighteen months if the financial-regulator exits stick. Long Brazil downstream players who buy US Gulf Coast barrels — Houston ULSD 15 ppm into Suape on a thirty-day cycle gets cheaper to load and cheaper to fund, which widens the arb for the Brazilian buyer. The stop on all three is the DC Circuit. If the Endangerment Finding rescission gets enjoined within six months on Administrative Procedure Act grounds, the trade is on a tighter leash and the carbon-risk premium widens again before it compresses.

The underrated piece: the financial plumbing

Everyone is talking about NEPA and ANWR. Almost nobody is talking about what just happened in the financial regulators.

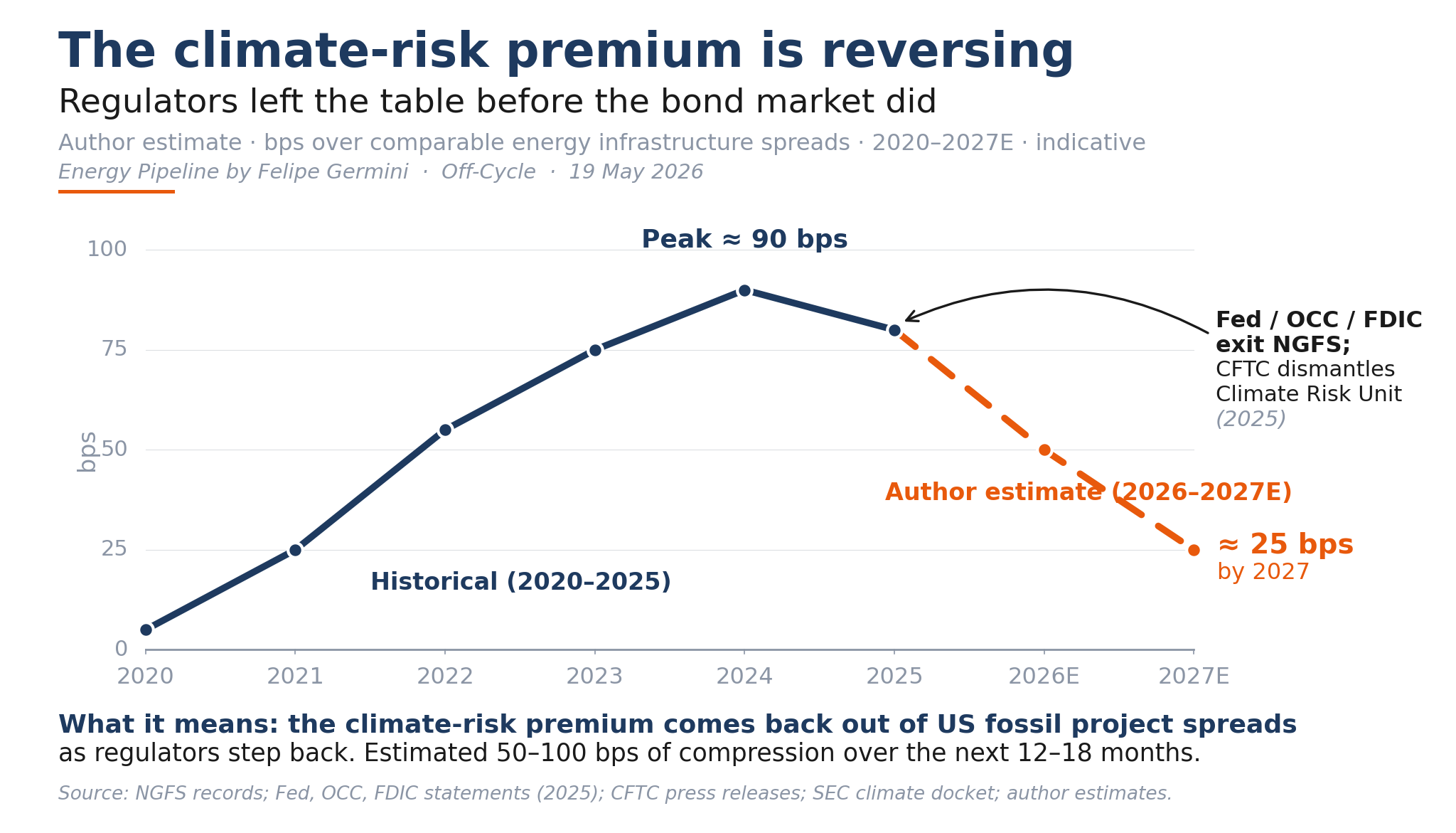

The Fed, OCC, and FDIC all withdrew from the Network for Greening the Financial System. The interagency climate-related financial risk principles for large banks were withdrawn. The CFTC dismantled its Climate Risk Unit, disavowed the 2020 Climate Risk Report, eliminated the MRAC climate-related market risk subcommittee, and withdrew its guidance on voluntary carbon credit derivative contracts. The SEC’s climate disclosure rule is paused indefinitely.

That is the floor below ESG retreat. The bank exits from the Net-Zero Banking Alliance in 2024 and 2025 — JP Morgan, Citi, BofA, Goldman, Morgan Stanley, Wells Fargo, the Canadians — were the private-sector retreat. The regulatory framework was the holdout pillar. That pillar is now gone.

This is what changes cost of capital for US upstream and midstream. Not the rhetoric. Not the lease sales. The structural removal of climate-risk framing from prudential supervision. When the Fed and the OCC no longer treat climate as a financial risk factor in their bank examinations, the banks downstream of those examinations no longer have to apply that framing to their loan books. Project finance for US fossil infrastructure gets meaningfully cheaper over the next twelve to eighteen months. Not because rates fall — because the climate-risk premium that started getting priced into spreads around 2022 to 2024 comes back out.

Chart 2 — Climate-Risk Premium Reversal

The regulators left the climate table before the bond market did. Now the bond market has cover to follow.

What is overrated

ANWR is overrated. The Coastal Plain has been opened, closed, and reopened so many times that the durability discount built into any acreage valuation there is enormous. Two recent lease sales were embarrassing duds — single bidders, low premiums, partial withdrawals. The majors will not touch Arctic acreage at sixty-dollar Brent without twenty-five-year regulatory certainty, and a future Democratic administration can close it again with the same executive pen that opened it. Reopening is symbolic; bidding is the test.

The replacement of the OCS five-year program is also more political than commercial. The Biden plan offered three sales. Replacing it with a more generous plan does not, by itself, conjure deepwater investment that operators were not already planning. Gulf of America activity is driven by tieback economics around existing infrastructure, not by the cadence of lease offerings.

The coal items get a lot of space in the document. Federal coal leasing moratorium ended. EIS requirements rescinded on three million acres. MATS rule reverted to 2012 standards. Coal combustion residual deadlines extended. None of this will save US coal as a baseload power source. The death of US thermal coal is being driven by gas-on-coal price competition, not by regulation. Henry Hub in the low threes beats coal economics in most markets regardless of what EPA does.

What is underrated — beyond the financial plumbing

The real friction is methane: the EU methane regulation passed in 2024 and the OGMP 2.0 reporting framework require importer-level intensity data starting in 2027, with phased thresholds. The US institutional channel that fed that data — the EPA’s Greenhouse Gas Reporting Program — is being weakened in the same fact sheet that withdraws the US from the convention.

The Endangered Species Act changes are also being underplayed. The Fish and Wildlife Service is proposing to narrow the act to its original intent — preventing endangered species from being killed — and to eliminate the regulation that made it a criminal offense to harm or harass them. That is a regulatory ceiling, not a floor. Combined with the Gulf of America carve-out and the Resolution Copper land transfer win in court, the ESA is being recalibrated as an obstacle that can be removed for economic projects, not a constraint that disciplines them.

The honest contrarian view

A lot of this is legally vulnerable. Rescinding the Endangerment Finding without a new scientific record will get challenged immediately and probably lose at the DC Circuit on Administrative Procedure Act grounds. The 28-day NEPA timeline will be torpedoed under arbitrary-and-capricious review. The categorical exclusions adopted without rulemaking are sitting ducks for litigation. The seven-agency NEPA procedural eliminations are partially supported by the May 2024 Fiscal Responsibility Act statutory changes and partially not — the not-statutory parts will be in court for two to three years.

And none of it restarts the demand curve. European industrial demand destruction is real and accelerating — chemicals, steel, ceramics — and the EU base load for refined products keeps shrinking. Chinese EV penetration is past the inflection point and now eating gasoline demand year by year. Every major energy outlook published in the last twelve months has trimmed its 2030-2035 oil call, including the ones written by people sympathetic to the upstream view. This rollback re-anchors US upstream economics for the next two to three years. It does not reverse the demand-side trajectory. Treating it as a structural reversal of the energy transition is the wrong read.

Smart counterparties are not treating this fact sheet as binding 2030 reality. They are treating it as a current-state regulatory environment that is optimistic and reversible. That is the right posture. The durability discount stays in every model. The pendulum has swung this far before and swung back.

Operationally, for those of us moving physical barrels and structuring deals, the change is incremental in the short term. The cargoes that loaded last week from Houston into Santos and Suape do not load any faster because EPA repealed the 2024 MATS amendments. What does change is sentiment, M&A appetite, and project finance availability. The Santos and Suape arbitrage from Houston ULSD 15 ppm widens because the rigs feeding those barrels load faster and the bond market funding the rig fleet pays less for the carbon-risk premium. Private equity that left upstream during the 2020-2024 ESG era now has cover to come back. Independents will be sold. The pre-IRA capital cycle in US upstream gets a second wind.

Three sentences for anyone who needs the summary. This is the most consolidated fossil-friendly regulatory action since the Reagan EO 12291 cycle, and broader in domain than that one was. Half of it is legally fragile and will be partially reversed in court or by the next administration, but the permitting compression and the financial-regulator exit from climate-risk frameworks are likely to stick because both are administrative in nature and consistent with broader deregulatory trends. The real beneficiaries are independents and private capital in US upstream; the real losers are international climate-coordination mechanisms and the legal infrastructure that has assumed federal climate regulation as a given for the last sixteen years.

Whatever your politics, this is a structural moment for the American energy industry. Not a turning point — those are rarer than the news cycle suggests — but a re-anchoring. The terms of the next decade just got rewritten.

If you trade physical barrels, structure deals, or sit on a board that allocates capital across US energy assets, the next ninety days are when the most important decisions get made. The capital that has been waiting for clarity now has it. The capital that was assuming a different regulatory environment now needs to recalibrate.

The fact sheet is dated May 2026. Most of it will be in court by the fourth quarter. The pieces that survive — the permitting compression and the financial-regulator exit — are the ones that mattered all along.

Founder & Managing Director, Germini Energy. Publisher of Energy Pipeline. 25+ years across upstream operations, downstream commodities, and M&A advisory. Former Country Managing Director for Brazil at Schlumberger.