The First Defection

What OPEC looks like when its third-largest barrel walks out of the room

On May 1, the United Arab Emirates stopped being a member of OPEC for the first time in 51 years. The mechanism was a press release. The consequence is something the oil market has not had to price since 1973, when Ecuador joined as the cartel was still defining what it was.

The headline writers reached for “historic.” The traders reached for the forward curve. Both reactions are correct and both are insufficient.

What actually happened is that the world’s seventh-largest crude producer decided that a quota system designed for a different decade was costing it between fifty and seventy billion dollars a year, and it had the capacity, the political latitude, and the buyer relationships to walk away from it. Abu Dhabi did not leave OPEC because OPEC was failing. It left because OPEC was succeeding at the wrong thing for the UAE’s barrel.

Read that again. The cartel is not collapsing. It is being asked to be smaller. And the difference matters.

The geometry of the exit

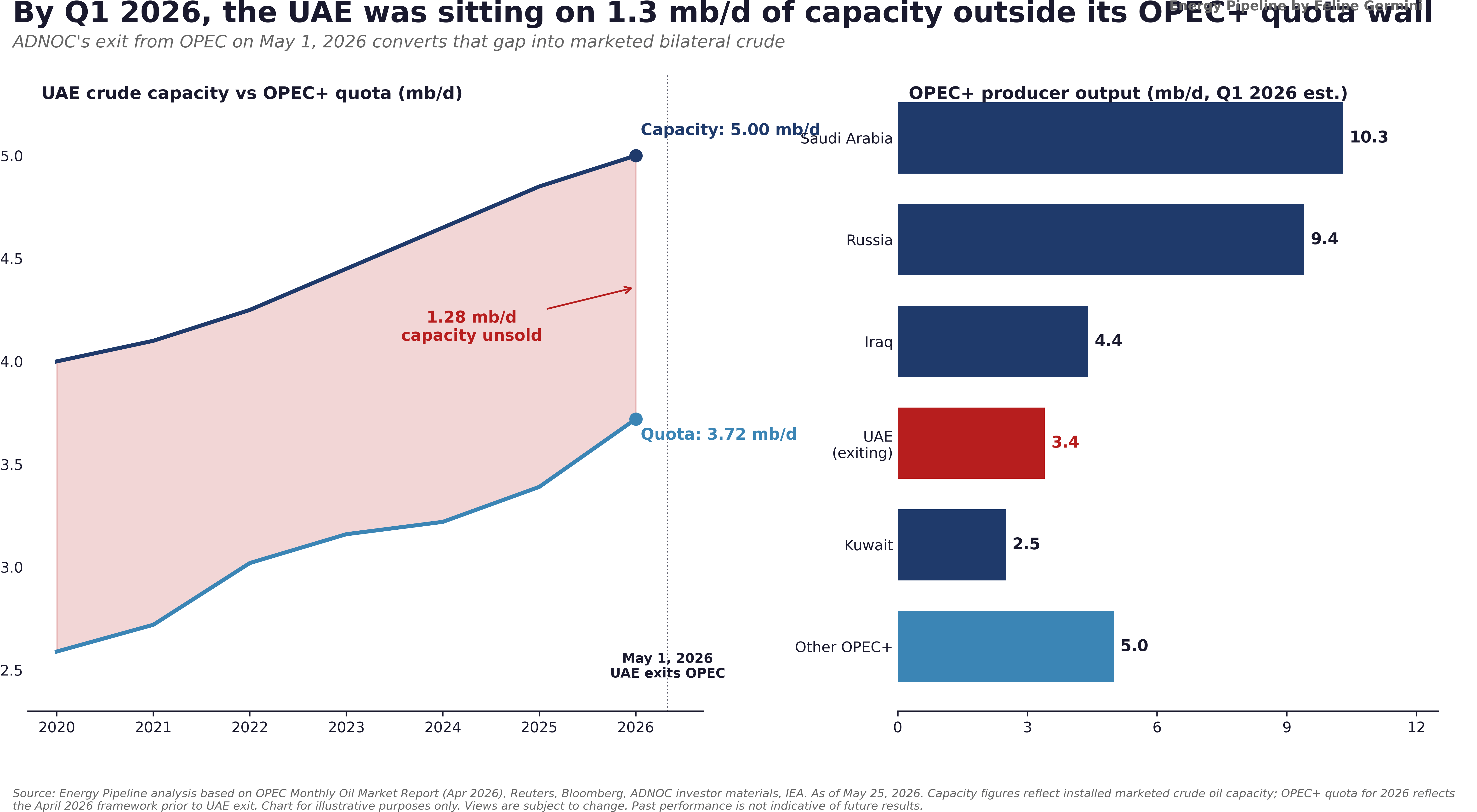

ADNOC has been telegraphing this move for ten years. Sustainable production capacity sits somewhere between 4.5 and 5.0 million barrels per day. The most recent OPEC+ ceiling for the UAE put actual output near 3.4 mb/d before the Iran war redrew the regional risk map. The arithmetic of the gap is straightforward. At a $75 Brent reference, every unsold barrel costs around $27,000 a day in foregone gross revenue. Multiply across roughly one to one-and-a-half million barrels of capacity sitting on the bench, then annualise. You arrive at exactly the $50-70 billion range the UAE energy minister has been quoting in international press without ever quite saying he is quoting himself.

A $150 billion ten-year capex program. Five million barrels per day of installed capacity pulled forward by three years from 2030 to 2027. Long-term offtake conversations with India, China, Korea, Japan that I am told from people on both sides of those tables had moved well past the exploratory stage by Q4 2025.

This was not a tantrum. This was a transition that had been priced into ADNOC’s own internal models since at least 2022.

The number nobody wants to say out loud

Chart 1. UAE installed capacity vs OPEC+ quota, 2020-2026; OPEC+ producer output snapshot.

The chart that should be on every trading desk this week is the one that plots UAE installed capacity against its OPEC+ quota over the last six years. The two lines diverge in 2022 and never reconverge. By Q1 2026, the gap is between 1.0 and 1.5 million barrels per day of capacity sitting outside the production wall. That is not a rounding error. That is, roughly, the entire incremental crude supply that the IEA had been counting on from non-OPEC sources to balance 2027.

For the cartel, the structural problem is that the UAE was the youngest, most invested, lowest-cost incremental barrel in the room. Saudi Arabia has spare capacity, but every barrel above 10 mb/d for Riyadh is a political decision before it is a commercial one. Iraq’s incremental barrel is contested by Kurdistan. Kuwait is producing close to its sustainable ceiling. Russia is producing as much as sanctions-tolerant buyers will absorb.

The UAE was the barrel of the next five years. And it just unhooked.

Three voices, three positions

In the seven days around the exit, three different people on three continents said three contradictory things about what this means.

The Saudi energy minister, speaking at a closed session in Riyadh that was reported afterwards by Reuters, called the UAE move “a sovereign decision we respect” and said nothing else of substance. The body language in the photographs that leaked from the session said something else. Translation from operator vocabulary: we will have a problem with quotas at the next four meetings.

The CEO of one of the major European integrated oils, talking on a Bloomberg panel two days later in Houston, said the exit was “less disruptive than people think because the UAE was already overproducing.” This is the buy-side talking its book. The European majors have been pivoting toward Middle East barrels for refinery security since the Russia restructuring, and a non-OPEC UAE with bilateral contracts is exactly the structure they prefer. Translation: we like this and we have been preparing for it.

The chief economist of a Mumbai-based refining and petrochemical group, quoted in the Times of India the following weekend, said the announcement would “fundamentally reshape Indian crude sourcing strategy for the next decade.” This is the most important of the three statements because it is the most honest. India imports approximately 85 percent of its crude. The UAE has been India’s second-largest supplier behind Russia in 2024 and 2025. A bilateral, no-quota ADNOC is, for India, the most important commercial development in oil since the Russia discount opened in 2022.

The mechanical chain

How does this actually play out in barrel terms? Walk through it slowly.

First, ADNOC adds between 600 thousand and 1.5 million barrels per day of effective marketed crude over the next 18-30 months, depending on how fast the bilateral contracts ramp and how much capacity actually gets monetised versus held in reserve as strategic optionality. Treat the middle of that range as the working assumption.

Second, OPEC+ has to absorb that addition without losing market share, which it cannot do at the current Brent reference. The cartel response will be either a tighter discipline on the remaining members (which has historically failed) or a quiet acceptance of a lower price floor (which is what the May 3 meeting’s “symbolic 188 thousand barrel” hike was actually signalling).

Third, the price war that didn’t happen in 2020 and didn’t happen in 2024 starts to look more plausible in late 2026 or early 2027. Not because anyone wants it. Because the math of the UAE’s exit creates the conditions for it. The cartel can absorb 200 kbpd of UAE drift. It cannot absorb a million.

Fourth, the buyer side starts negotiating bilateral term contracts with ADNOC at structures that look more like long-term LNG offtake than like traditional crude term deals. The Brazilian refiner that historically takes a Middle East cargo through a sour grade swap with a major trader will increasingly have the option of going direct to Abu Dhabi for a multi-year, indexed structure. That is a more important change for the Brazil sour barrel than anything Petrobras has done in the last five years, and almost nobody in Rio is talking about it yet.

The architecture frame

The five-year frame on this story is that OPEC is becoming what it always intended to be, a coordination mechanism for the legacy producers, and the post-quota producers are building the next-generation Gulf supply architecture in parallel. Aramco’s IPO in 2019 was the first signal that the Gulf was preparing for an oil world with different rules. The UAE’s exit is the second.

The thirty-year frame is that the post-war international oil order was built on three pillars: the integrated majors, the seven sisters’ successors, and the OPEC coordination mechanism. Two of those pillars have already reorganized. The third is reorganizing now.

The forty-year frame is the one nobody writes about because it sounds too speculative. In a world where global oil demand peaks somewhere in the early 2030s, the question for a low-cost Gulf producer is not how to defend prices. It is how to monetize reserves while the demand is there. The UAE’s exit reads as the first major producer to operate explicitly under that frame. Saudi Arabia will not be the second, but it will not be slow to follow.

Two ways this view dies

I have been wrong about Gulf coordination before, and I will be wrong again. The two ways the above analysis dies are worth naming.

One: ADNOC’s bilateral contract ramp is slower than the company has signalled. The Indian buyer side moves fast, but Japanese and Korean term structures take 18-24 months from MOU to first cargo. Chinese buyers move on government calendars. If the actual incremental barrel into the market lags by 12-18 months from the May 1 exit, the cartel has more time to absorb the change and the price war scenario fades.

Two: a renewed Iran shock takes the Strait of Hormuz offline for a structural period. Anything north of 60 days of meaningful tanker disruption rewrites every analysis written this month. The Strait is open today. Insurance markets are pricing it as if reopening is fragile. If the fragility becomes reality, the UAE exit becomes a footnote to a much bigger story.

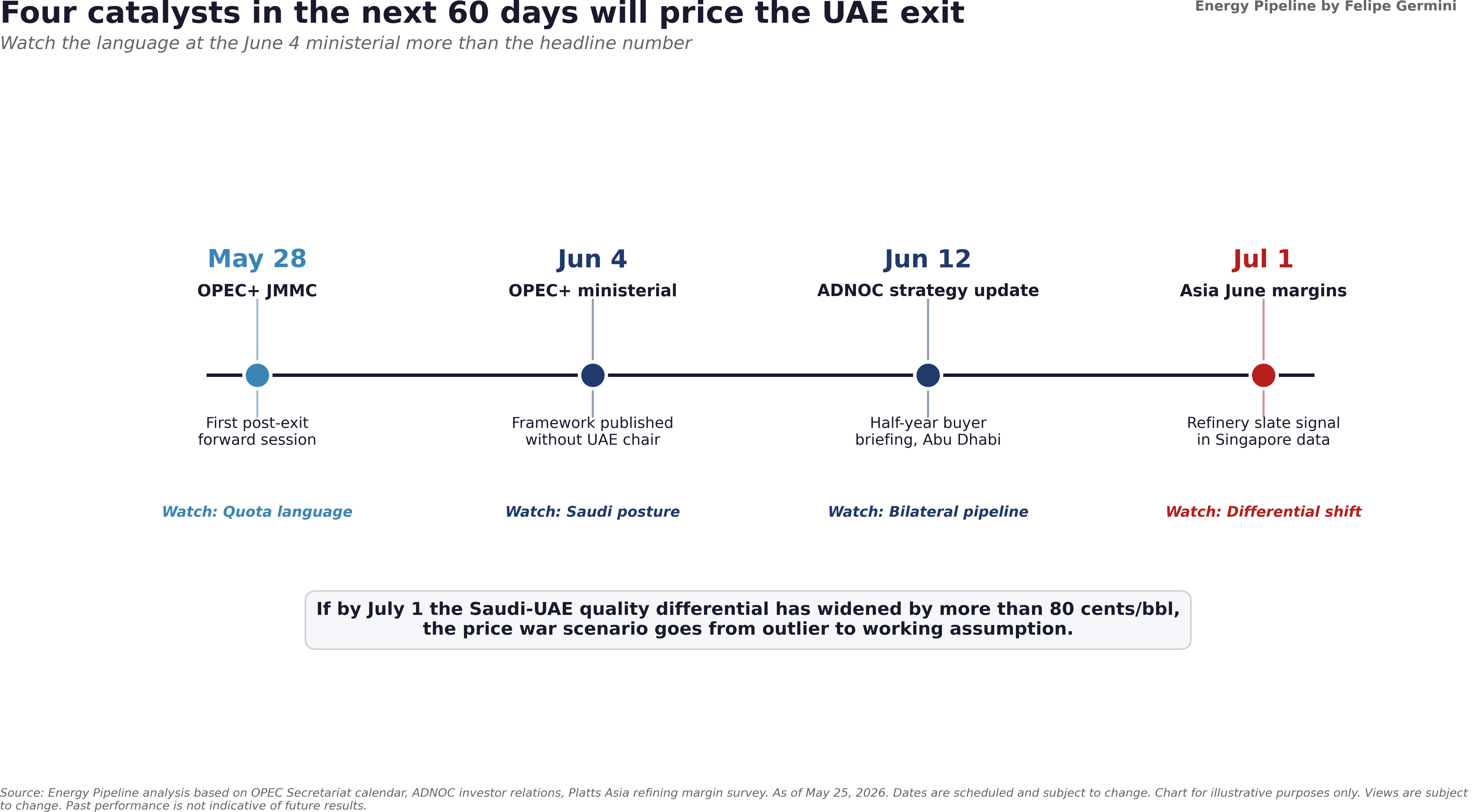

The dated calendar to watch

Chart 2. Four-catalyst calendar through July 1, 2026.

Four catalysts inside the next 60 days will tell you whether the analysis above is converging or diverging from market reality.

May 28. OPEC+ Joint Ministerial Monitoring Committee meeting. First post-UAE-exit forward-looking session. Watch the language on quotas, not the headline number.

June 4. Full OPEC+ ministerial. The first time the cartel formally publishes a production framework without the UAE in the room. The framework will tell you whether Saudi Arabia is leading discipline or accommodating drift.

June 12. ADNOC half-year strategy update, traditionally given in Abu Dhabi to invited buyers. The bilateral contract pipeline will be partially visible here.

July 1. Singapore and Asian refining margins data for the June month. If Asian refiners are shifting their sour grade slate toward UAE light/medium and away from Saudi Arab Light, you will see it in the differentials before you see it in trade press.

What this means on the desk

If you are a refiner: open the conversation with ADNOC’s term marketing team now, not in six months. The structures available in the first wave of bilateral contracts will be more favourable than what shows up after the obvious buyers have locked their volumes.

If you are a Brazilian importer: the medium-sour ADNOC barrel into Santos has not historically been competitive against the Saudi and West African slates. The economics of a non-quota ADNOC change that calculation by between $1.20 and $2.80 per barrel on the FOB structure, depending on freight. Worth modelling.

If you are a trader: the Saudi-UAE quality differential, which has been remarkably stable since 2019, becomes the most interesting structural trade in the Middle East crude complex over the next 18 months. The widening case is the consensus. The narrowing case is the contrarian one, and it depends entirely on whether Riyadh decides to defend market share.

If you are policy: the assumption that OPEC’s coordination function is monolithic and durable was always slightly more religious than analytical. The May 1 announcement is the data point that breaks the religion. Plan accordingly.

The week ahead

Wednesday’s Flow piece will go deeper on this, specifically on the Regions pillar: how the Gulf supply architecture reorganises itself across the next 18 months and what the Brazilian buyer side should be doing with that information. The Friday Horizon will frame the next-week catalysts.

This is a structural story, not a price story. The Brent screen will move on Iran headlines and inventory data this week. The screen is not where the action is. The action is in the term contract conversations happening in Abu Dhabi, Mumbai, Houston, and Singapore that almost nobody outside those rooms is reading correctly yet.

I have sat in those rooms across three decades. The room in Abu Dhabi this month does not look like the room in Vienna ever did. That is the signal.

• • •

Paid Flow subscribers receive the full presentation pack for this edition: 10 slides covering the UAE capacity vs. quota math, the Saudi-UAE differential trade map, and the four-catalyst calendar through July 1, formatted for desk and boardroom use. Wednesday’s Flow piece (Regions pillar) goes deeper on the Gulf supply restructuring thesis.

• • •

Felipe Germini is a Brazilian energy executive with 25+ years operating across the full oil and gas value chain. He built his career at Schlumberger, rising to Country Managing Director for Brazil with full P&L responsibility over deepwater and onshore operations, and later moved into downstream commodities, M&A advisory, and executive consulting across Brazil, Latin America, Russia, Africa, the Middle East, and the United States. As certified board member, he founded Germini Energy, a boutique brokerage.