The Flow Flagship Edition : The Four-Year Queue

The market is funding the chips. The bottleneck is the gas turbine, and there is a four-year line for one.

Every AI capex number you read this quarter rests on one silent assumption: that the power shows up on schedule. Go ask anyone who tried to order a heavy-duty gas turbine in 2026 how that is going. The honest answer is 2030.

The consensus has decided that artificial intelligence is a semiconductor story. Chips, fabs, GPUs, the names everyone can recite. That framing is not wrong so much as it is one layer too high. The thing that actually gates an AI buildout is not the processor. It is the electron, and underneath the electron, the machine that makes it on demand. A data center is a power plant with a roof. The market is pricing the roof.

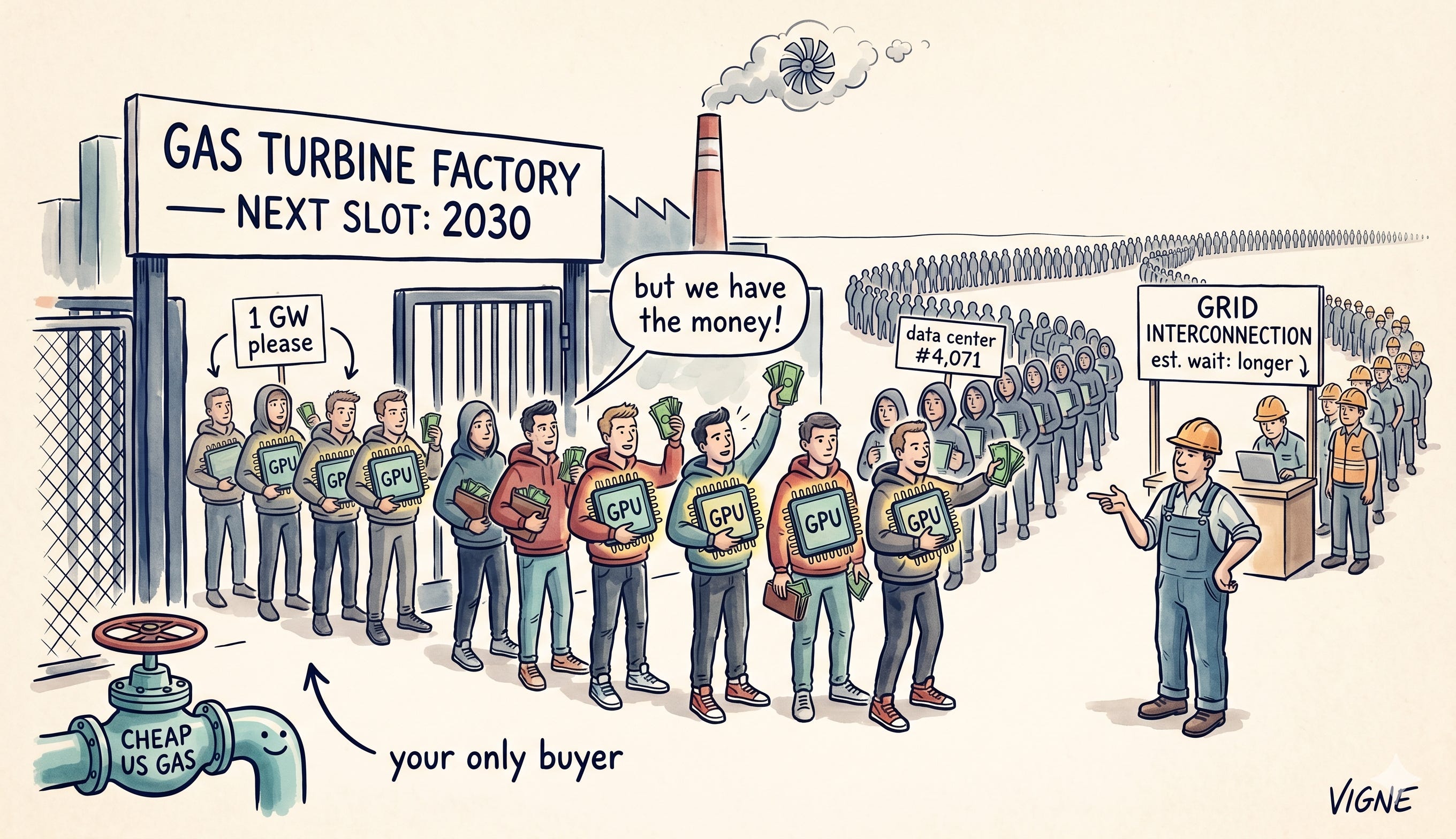

This is where the desks have it backwards, and the mispricing is large enough to trade. A graphics chip has a lead time measured in months and a supply chain that responds to price. A 1,500-megawatt block of firm, dispatchable power has a lead time measured in years and a supply chain that does not care how much money you wave at it. You cannot pay a turbine into existence faster than the forging schedule allows.

Chart 1 · You can buy chips in a quarter. You wait years for the power and the wires. Author analysis from OEM and grid-operator lead-time guidance.

The chain, one link at a time

Strip the story to mechanics. There is no hand-waving in any of these steps, which is why the conclusion is hard to dodge.

Compute demand becomes electricity demand. A frontier training and inference campus does not sip power. It pulls hundreds of megawatts, and the hyperscaler roadmaps now talk in gigawatts. The chip roadmap is a power roadmap wearing a different badge.

That load has to be firm. A model mid-training does not tolerate a grid that comes and goes with the weather. It needs 24-hour dispatchable supply. Solar and wind contribute, but the baseload has to be there at 3 a.m. when the wind drops. That means gas, nuclear, hydro, and storage to smooth the edges.

Firm new-build means gas turbines. Nuclear is years too slow for this cycle. Hydro is geographically fixed. The only firm generation you can order at scale and bring on this decade is the gas turbine. Everyone reached that conclusion at the same time.

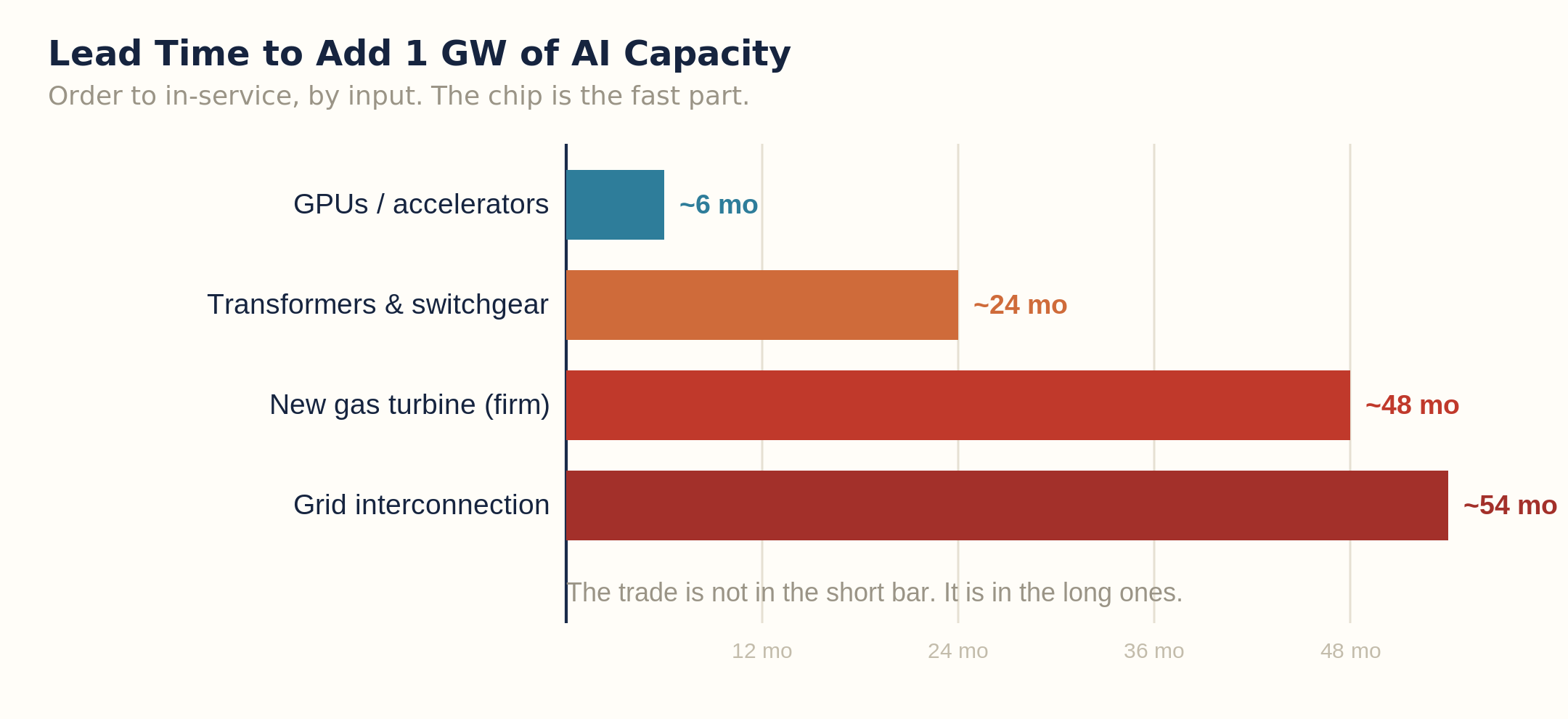

The turbine line is full. A handful of manufacturers make heavy-duty turbines. Their order books are sold out into the back half of the decade. Lead times have stretched from roughly a year before the cycle to about four years now. Slots, not money, are the scarce asset.

The grid is the second queue. Even with a turbine, the interconnection wait is its own multi-year line. Transformers and high-voltage switchgear have their own backlogs. The campus is not built when the chips arrive. It is built when the last electron path is energized.

Put those five links together and the picture inverts. The constraint on the AI cycle is not silicon. It is the forging capacity of a few turbine halls and the throughput of grid interconnection queues. That is a far more inelastic, far more concentrated bottleneck than chips, and the market is barely pricing it.

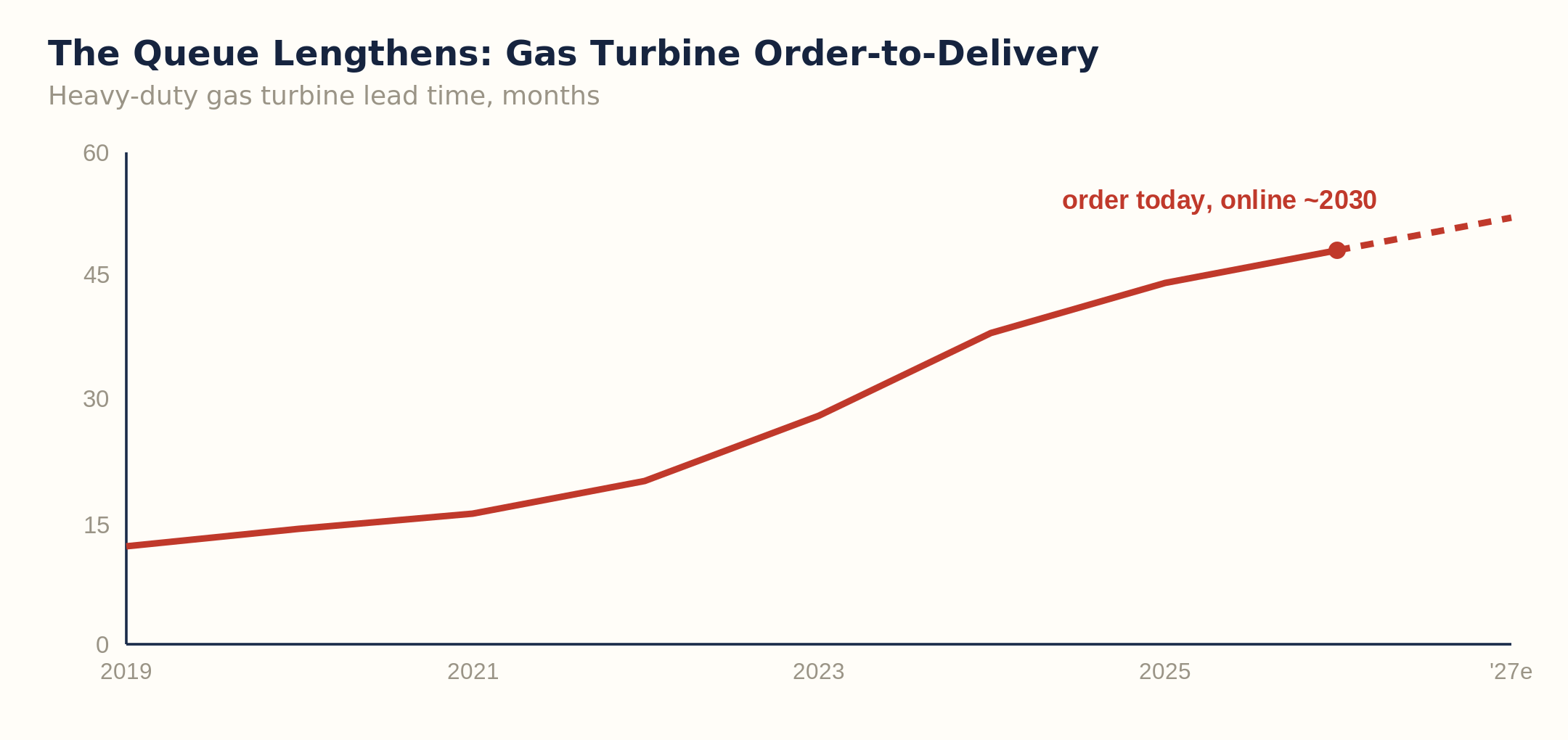

Chart 2 · The line went from about a year to about four. Money does not move the forging schedule. Author analysis from turbine OEM disclosures and industry order-book commentary.

Why this is not the dotcom fiber story

Someone in the room always says it: this rhymes with the late-1990s overbuild, when the fiber everyone laid sat dark for a decade. The objection is fair and it is wrong on one specific point. Fiber was a manufactured good with elastic supply. Firm power is a permitted, forged, grid-connected asset with a four-year minimum gestation and a wall of regulation around it. You can flood the world with fiber in eighteen months if the capital says so. You cannot flood it with interconnected gigawatts on any timeline the capital controls. The constraint is physical, not financial, and physical constraints clear slowly.

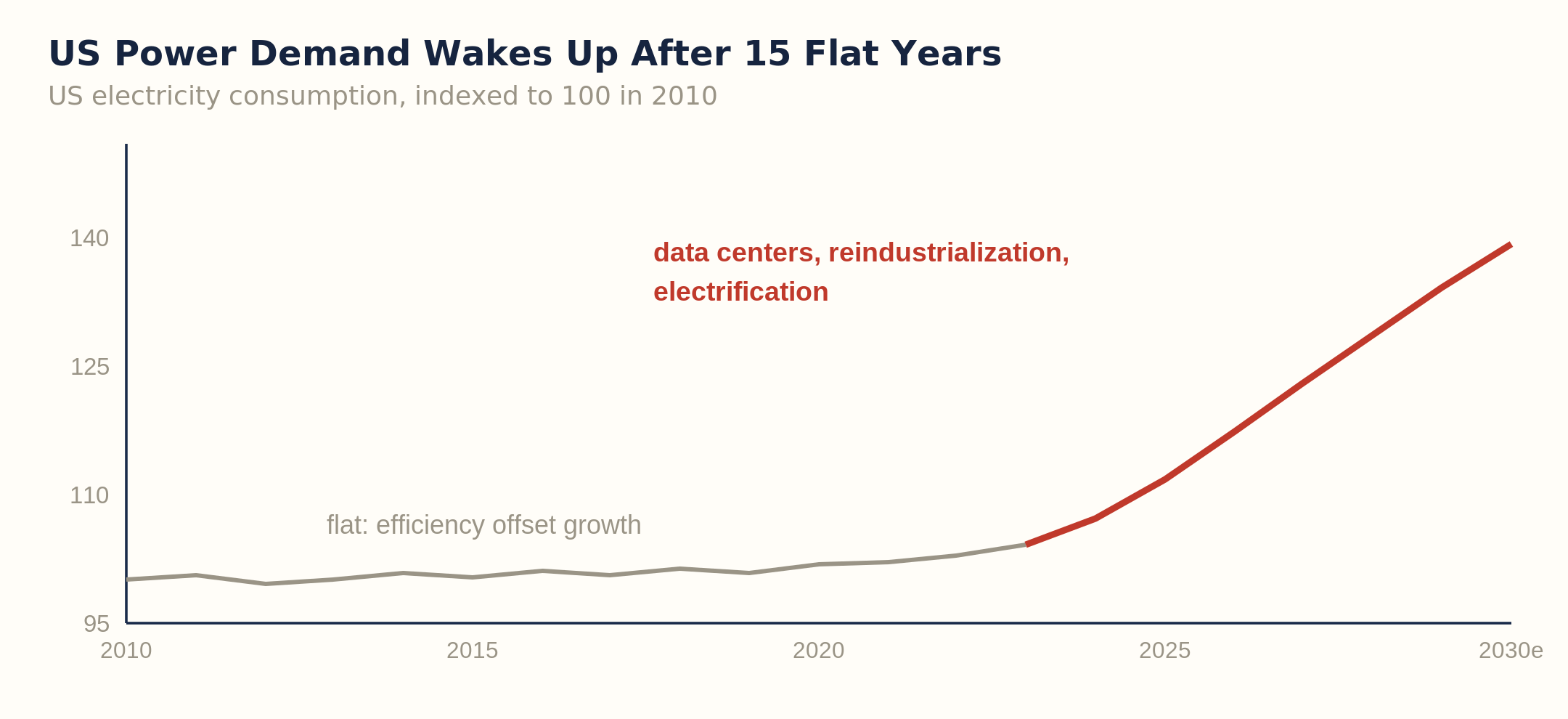

Chart 3 · A decade and a half of flat demand trained utilities and markets to expect nothing. The inflection is colliding with a supply chain that was sized for stagnation. Author analysis from EIA and industry load forecasts.

There is a second-order point that links straight back to Monday. The American gas glut that has Henry Hub down 30 percent has been searching for a structural buyer. Firm power for data centers is that buyer. Baseload gas demand from compute, plus the LNG that finally clears the export wall later this decade, is the mechanism that drains the surplus. The barrel that nobody wanted becomes the fuel that the most capital-rich industry on earth cannot do without. That is the through-line of the whole week.