The FLOW Weekly: War Premium Refuses to Die

The trade is the crack, not the flat price.

THE FLOW | WEEKLY ENERGY PIPELINE RECAP | MAY 18-22, 2026 | ISSUE W21/26

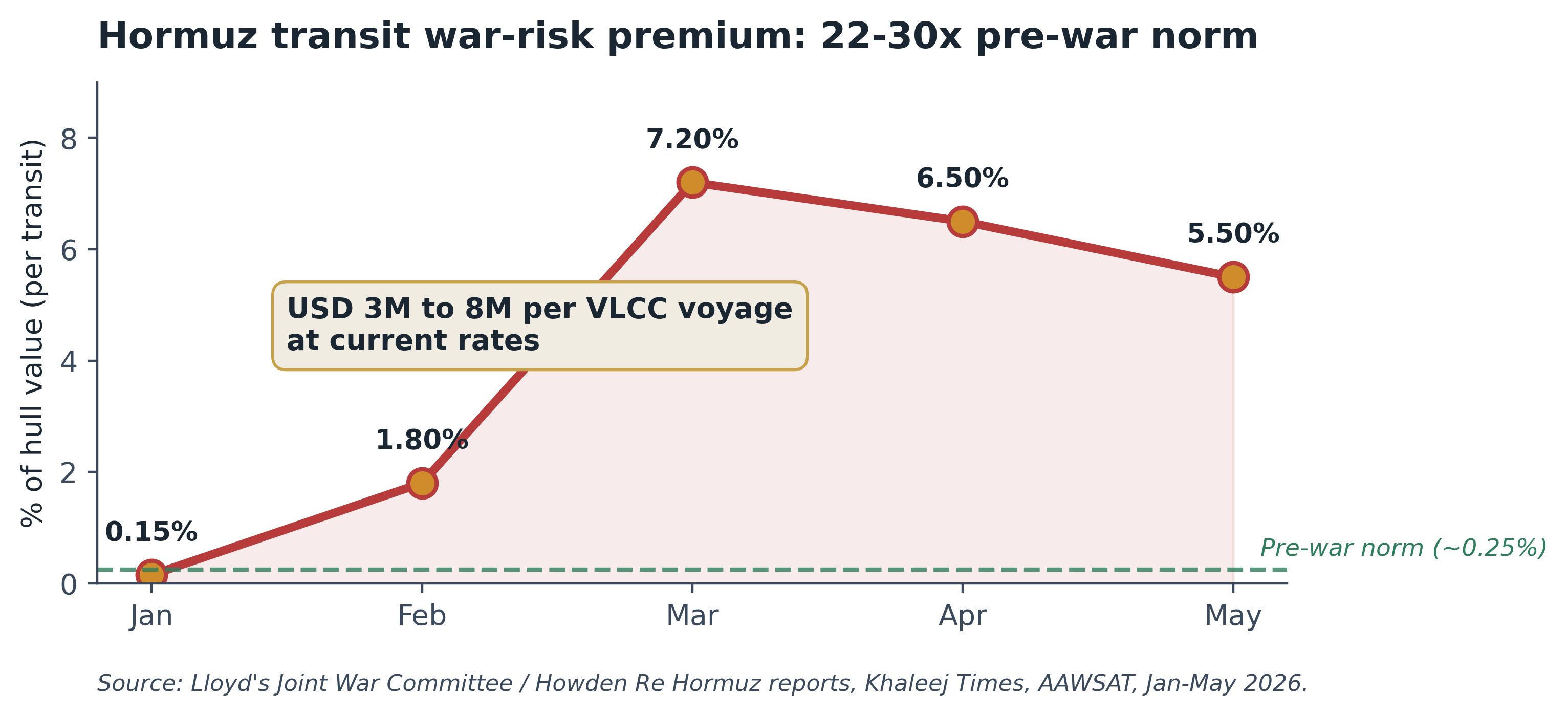

Most macro coverage this quarter is anchored on OPEC+ quotas and Chinese demand. The actual price discovery is happening inside Lloyd’s of London. Since late February, war-risk premiums on Strait of Hormuz transits have moved from 0.15% of hull value to 5.5%, translating into USD 3M to 8M of insurance cost per VLCC voyage. That is roughly $3 per barrel of pure premium before freight, before lightering, before P&I.

Brent printed $105.10 on Friday and still closed the week down 4.3%. The market is pricing the reopening of Hormuz before the diplomatic paperwork is signed. The crack complex has not unwound in tandem. That gap, between flat price selling off on hope and crack spreads holding the wartime premium, is the trade.

Summary

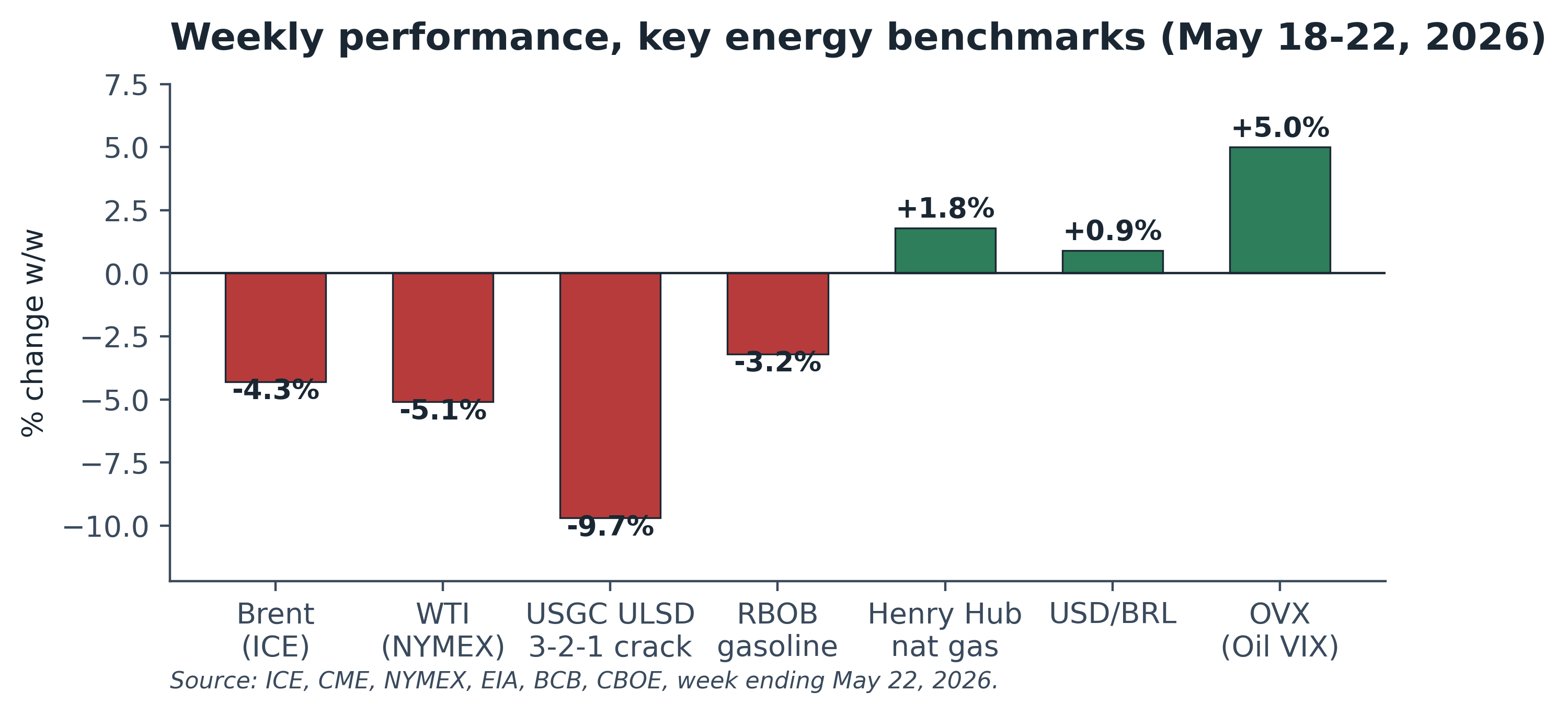

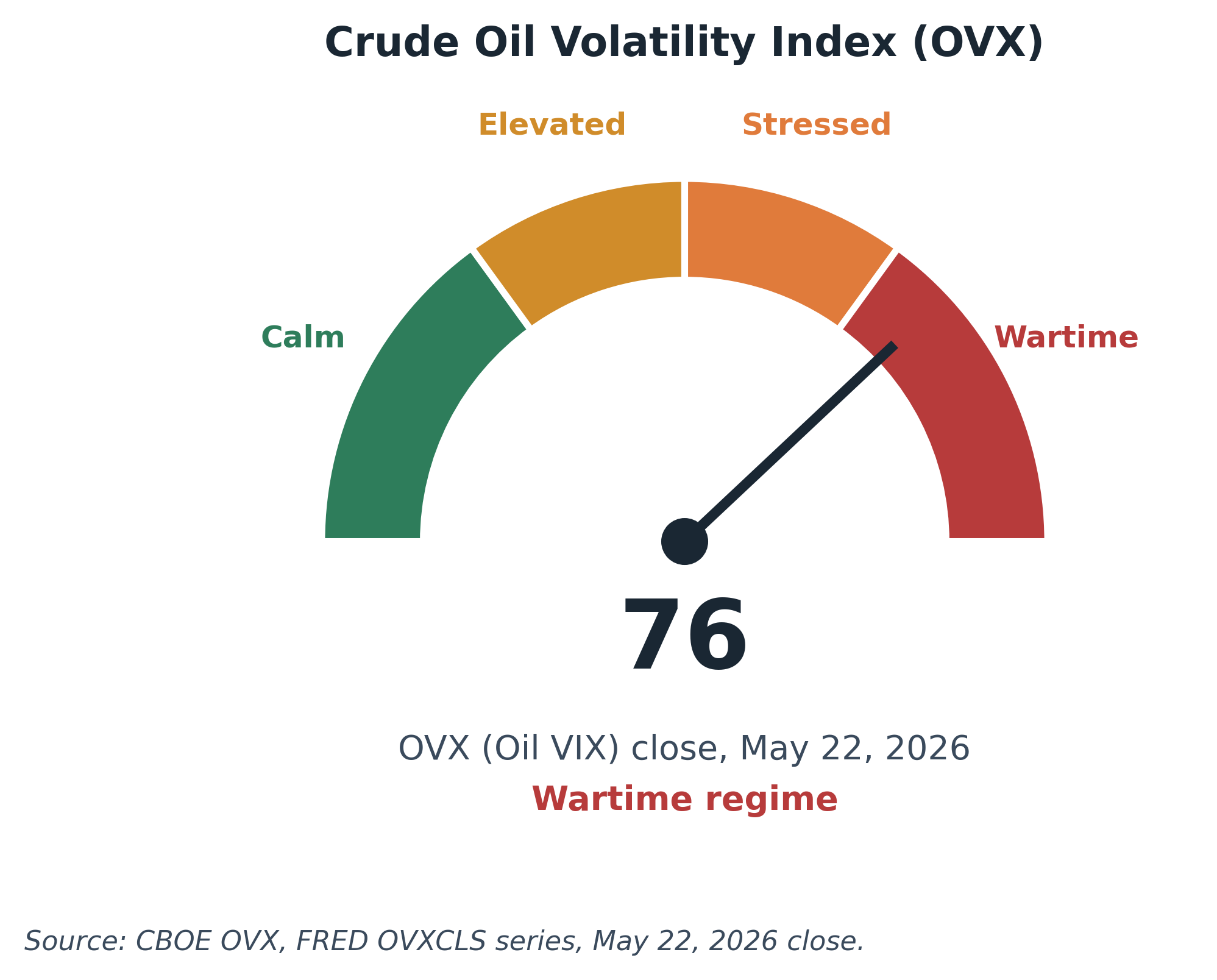

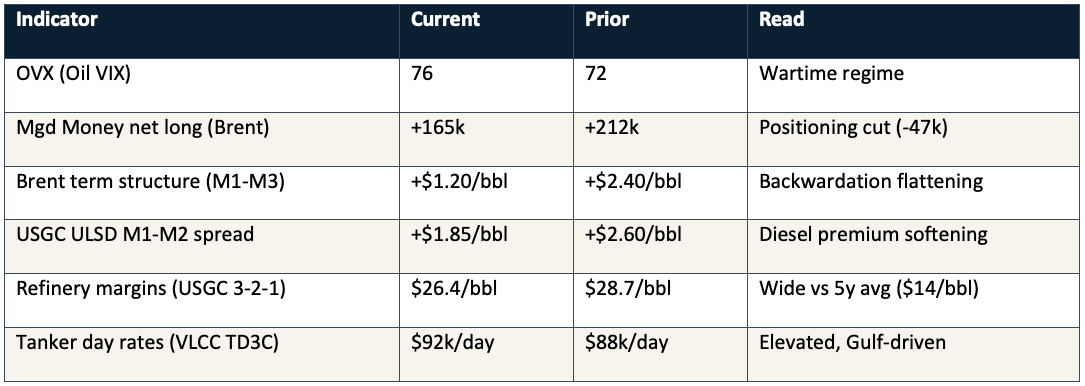

1. Performance: Brent (Aug-26) -4.3%, WTI -5.1%, USGC ULSD vs WTI 3-2-1 crack -9.7% to $26.4/bbl, OVX +5 points to 76 (wartime regime).

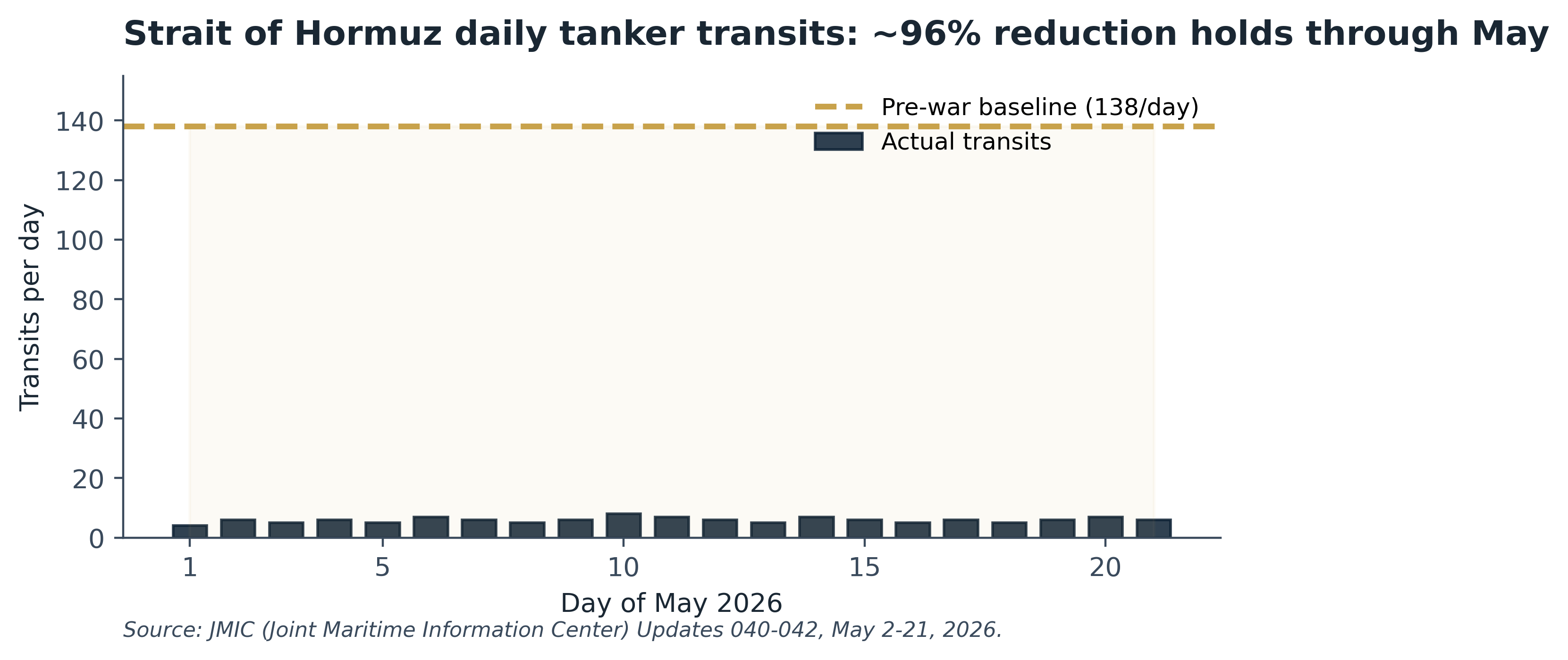

2. Hormuz pulse: daily transits 5-7/day vs 138/day baseline. JMIC threat level CRITICAL through May 21. War-risk premium 5.5% of hull value, USD 3M to 8M per VLCC voyage.

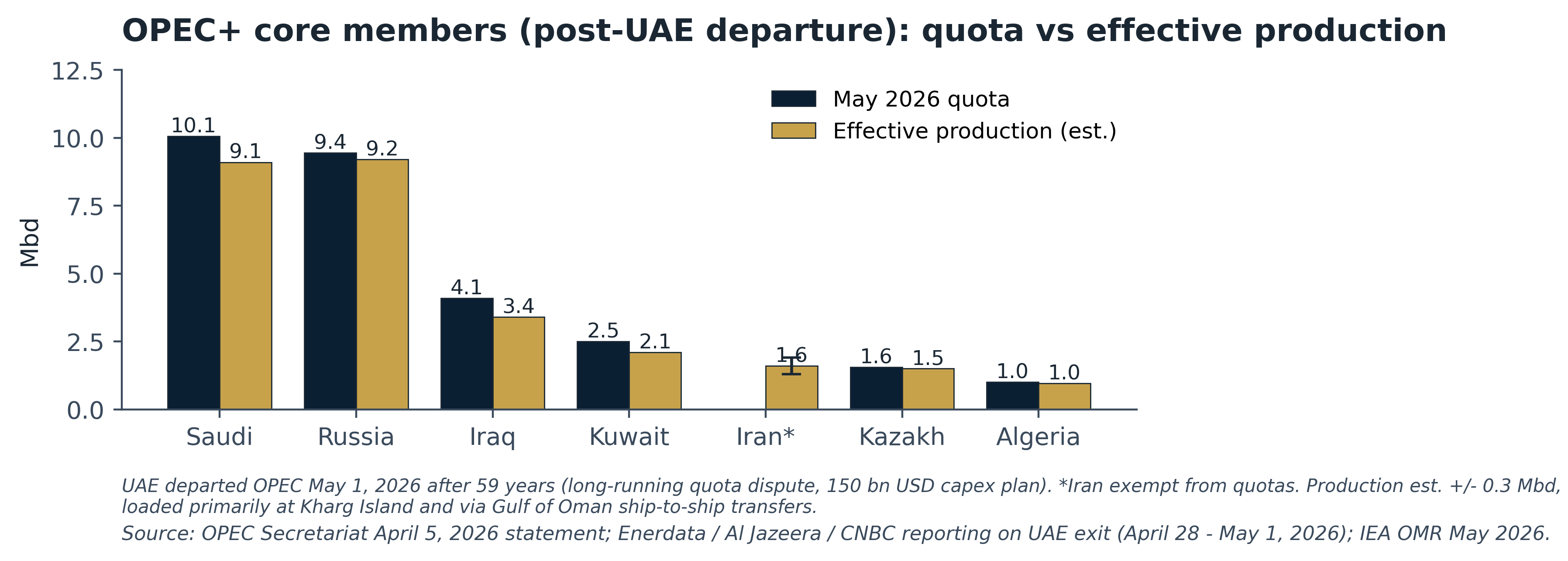

3. OPEC+ update: UAE departed OPEC May 1, 2026 (the largest exit in the cartel’s history). May quota lifted 206 kbd, largely symbolic. Saudi, Kuwait, Iraq running 0.5 to 1.0 Mbd below quota. Iran producing ~1.6 Mbd (+/- 0.3) via Kharg Island and ship-to-ship transfers.

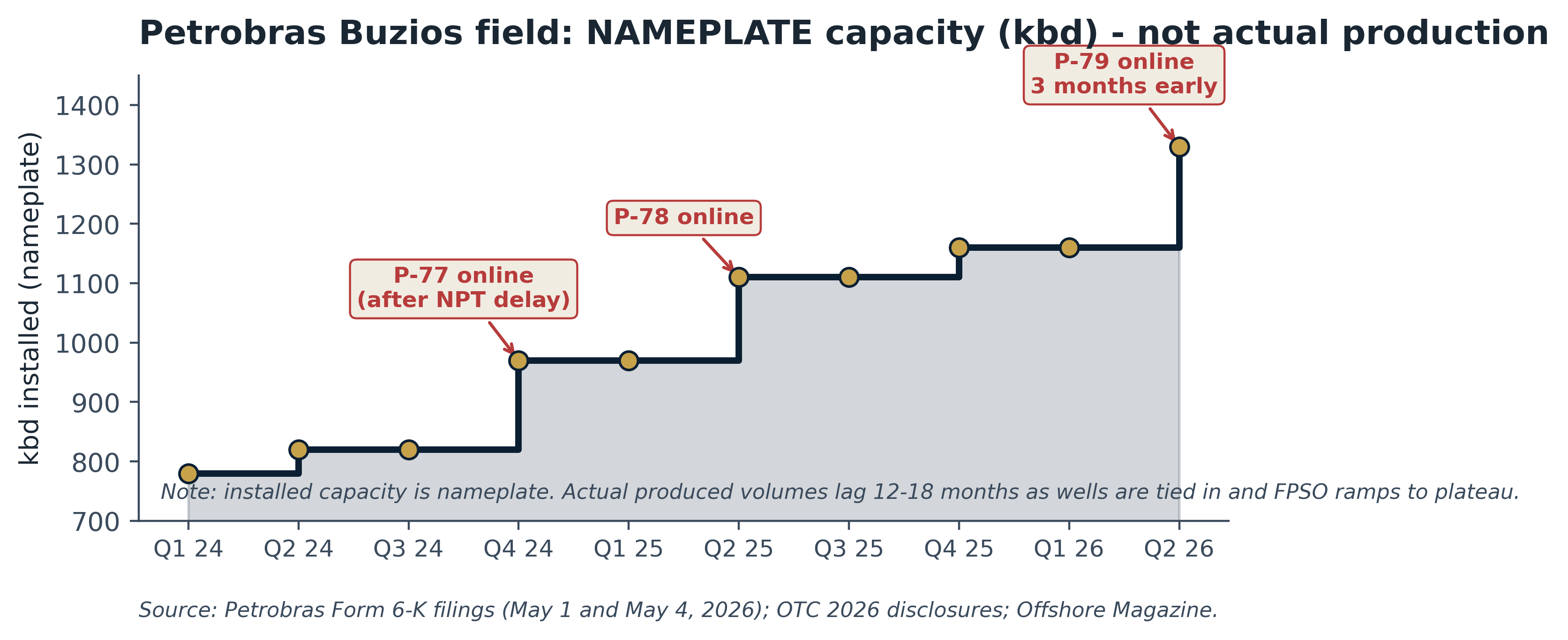

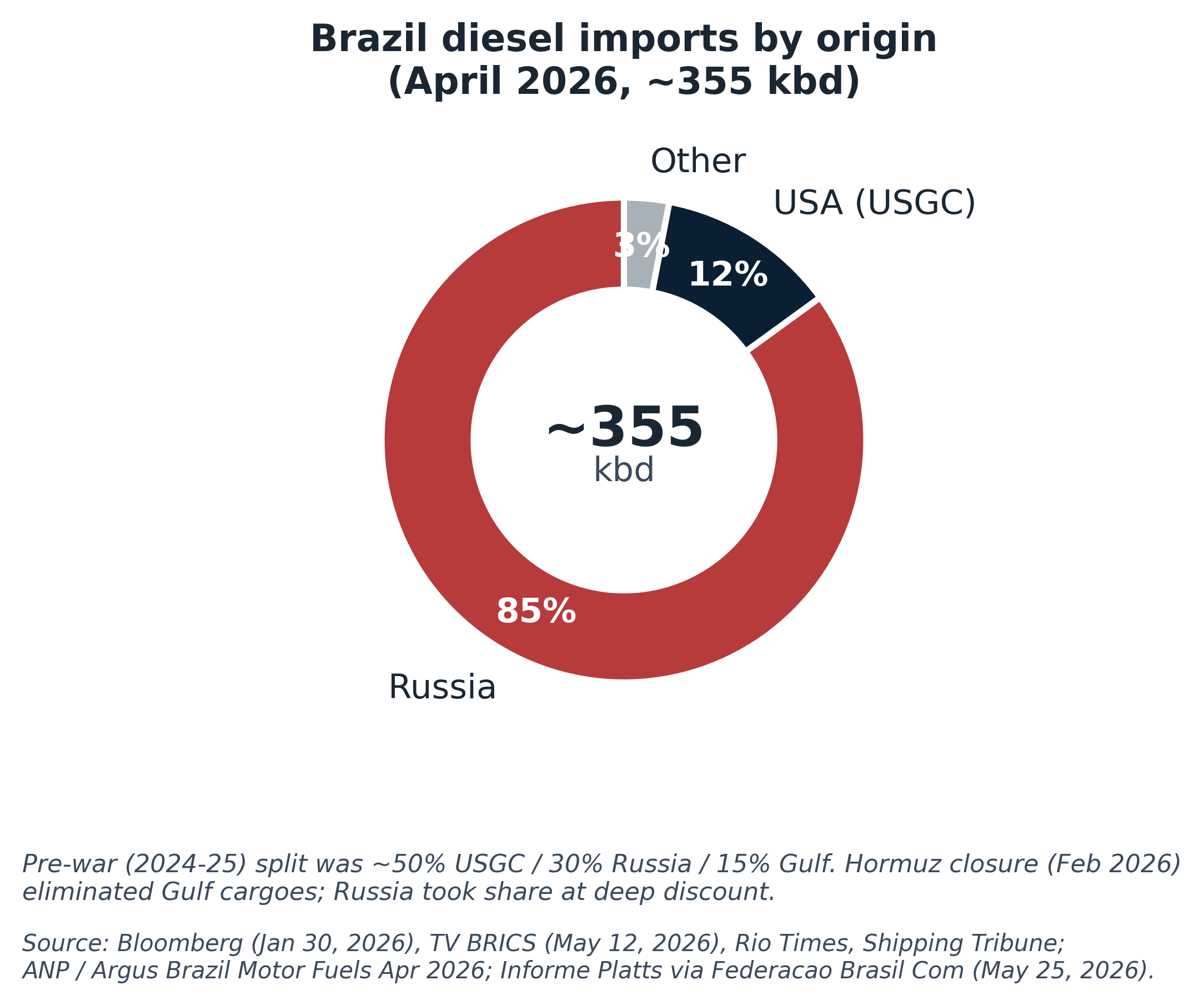

4. Brazil desk: Petrobras P-79 first oil three months early (Buzios nameplate now 1.33 Mbd, actual production lags 12-18 months). ANP approved Berbigao AIP, consortium board ratification pending. IBAMA renewed two Equatorial Margin exploratory well licenses. Brazil’s diesel import mix has flipped to Russia ~85% / USGC ~12% since Hormuz closed Gulf cargoes in late February.

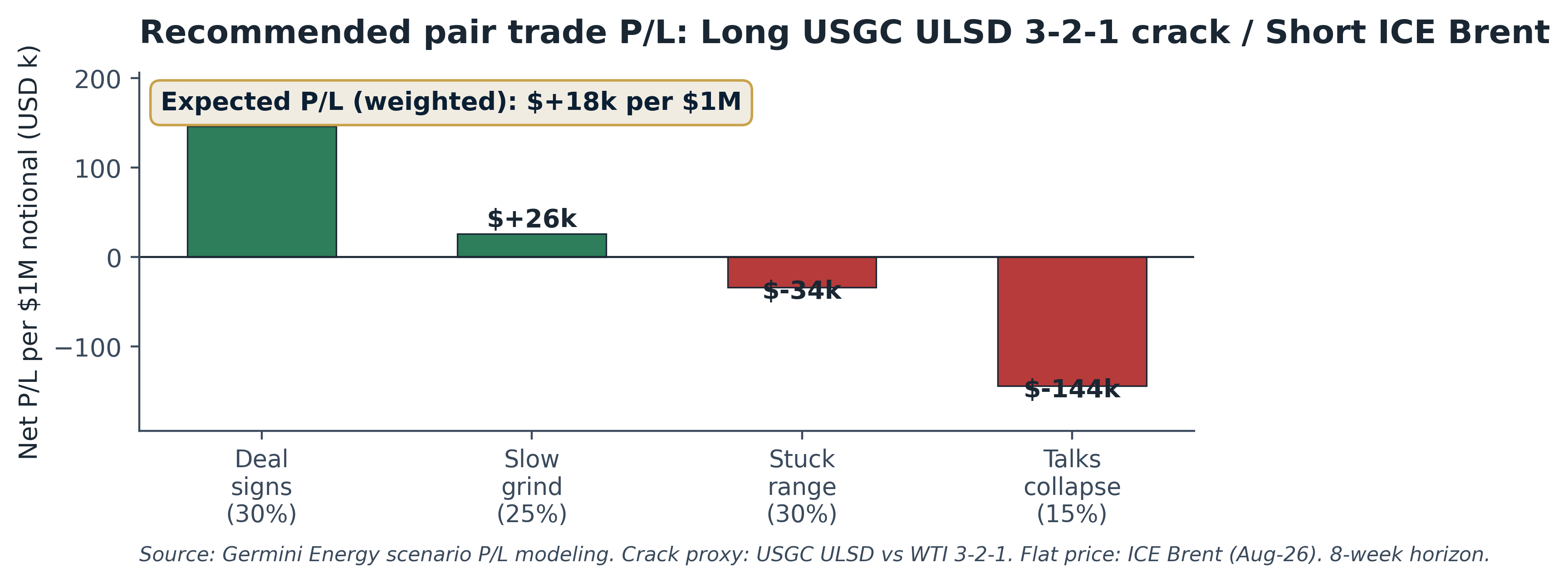

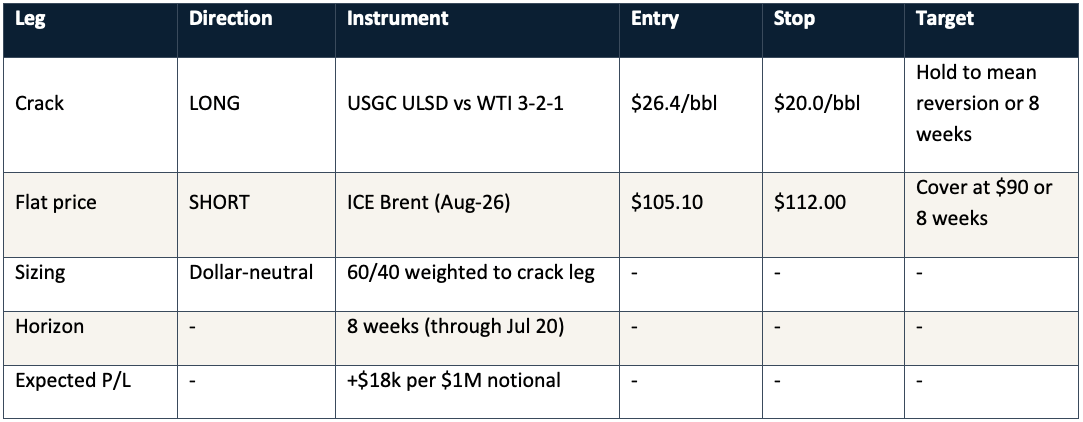

5. Recommended trade: long USGC ULSD vs WTI 3-2-1 crack / short ICE Brent (Aug-26), dollar-neutral, 8-week horizon. Expected P/L +$18k per $1M notional at scenario weights. Stop on crack break below $20/bbl.

MY TAKE

Diplomacy is being priced as more likely than the insurance market believes. The flat price has come down on US-Iran framework leaks. The cracks have not, because actual tonnage is still not moving safely through Hormuz. Insurance markets do not move on headlines; they move on transits. When they reconcile, they will reconcile through the crack complex, not flat price. That is the trade.

Performance Recap

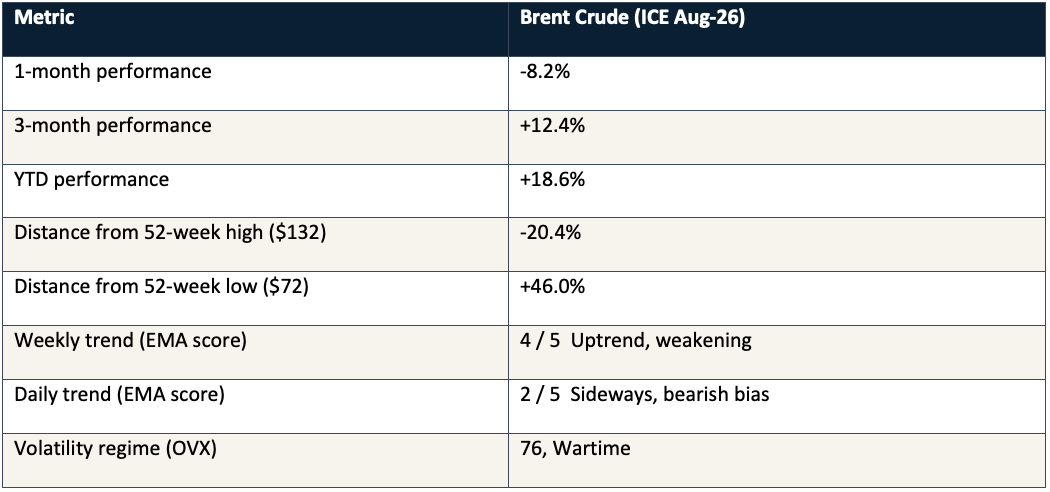

1. Brent Crude (ICE Aug-26) intraweek path

Brent gapped down Monday on the leaked US-Iran ceasefire framework, ground lower through Thursday to an intraweek low near $96.30 as the diplomatic narrative built, then rebounded Friday to $105.10 after Iran’s Supreme Leader ordered enriched uranium stockpiles to stay inside Iran (which the market read as a step backward on the deal). Weekly close: -4.3% w/w on ICE Brent (Aug-26).

2. Weekly performance, key energy benchmarks

USGC ULSD vs WTI 3-2-1 cracks bled 9.7% (settling $26.4/bbl) as the diesel war premium softened on Hormuz reopening hope. OVX moved up five points to 76, a wartime-regime reading that says options markets are pricing further dislocation, not normalization. Henry Hub was the only positive print, driven by US heat-related demand and weak Permian associated gas response.

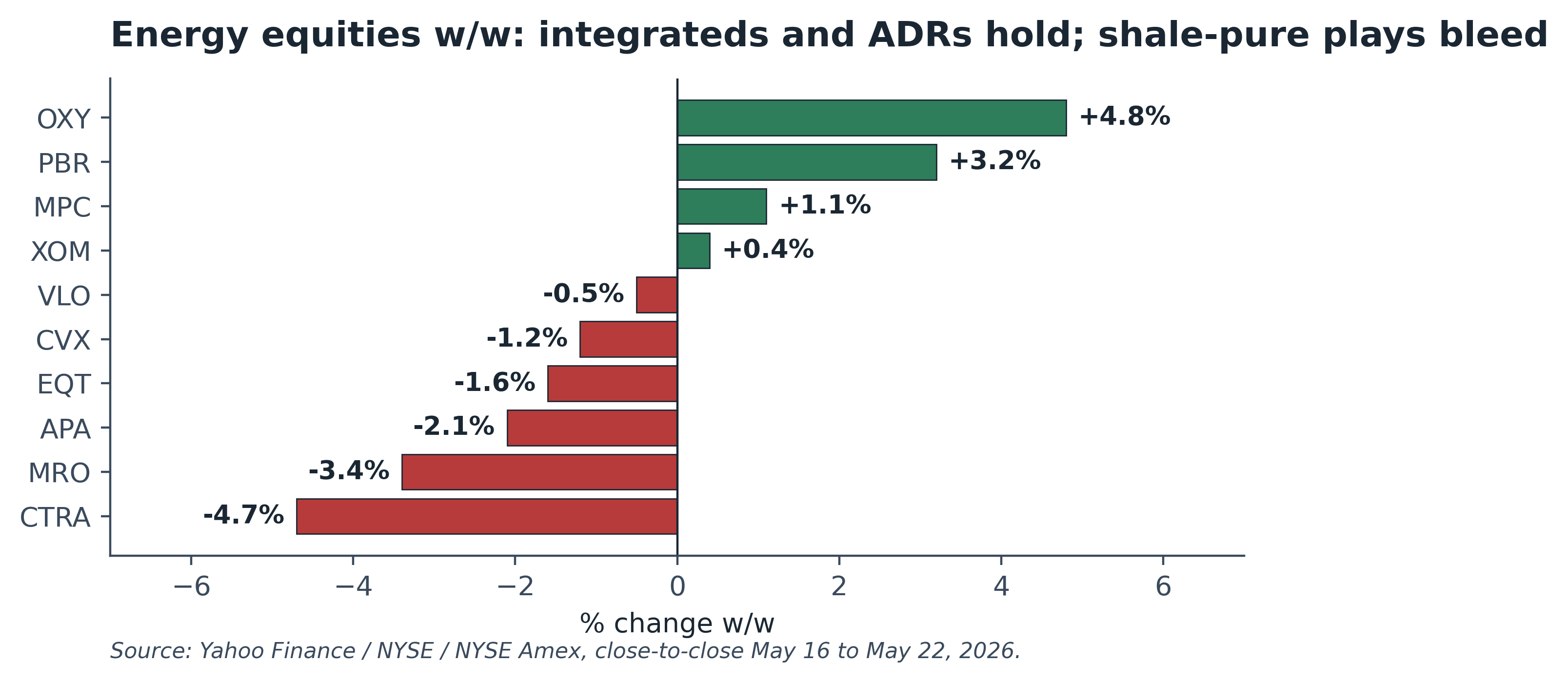

3. Energy equities, top vs worst

Brazilian and high-leverage US independents outperformed (OXY +4.8%, PBR +3.2%) on Buzios first oil and the resilient Atlantic Basin barrel. US shale-pure plays underperformed (CTRA -4.7% on its $50/bbl breakeven framework being tested, MRO -3.4%) as the broader WTI selloff threatened back-half capex math.

MY TAKE

The split between Brazilian/integrated names and US shale-pure plays is the first thing worth flagging. When the market sells flat price on diplomatic hope, the names with integrated downstream, low-cost barrels, or non-Gulf-dependent logistics outperform. The strongest version of the bear case on PBR is that the equity is correctly priced because political-asset risk is real (Lula election cycle, dividend policy variance, CNPE setting B15 by resolution, pricing-policy reversal risk post-October). I disagree, but I have not yet sized the call. See trade section.

Momentum Pulse Check

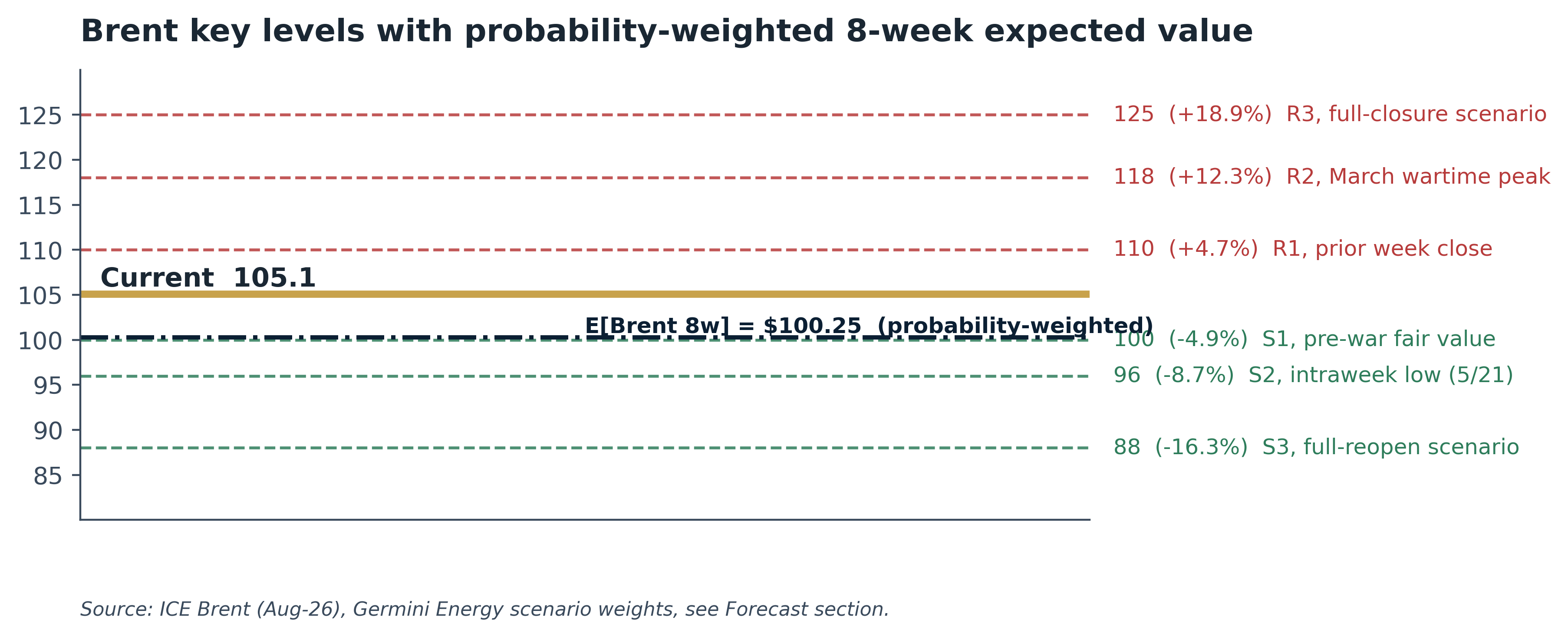

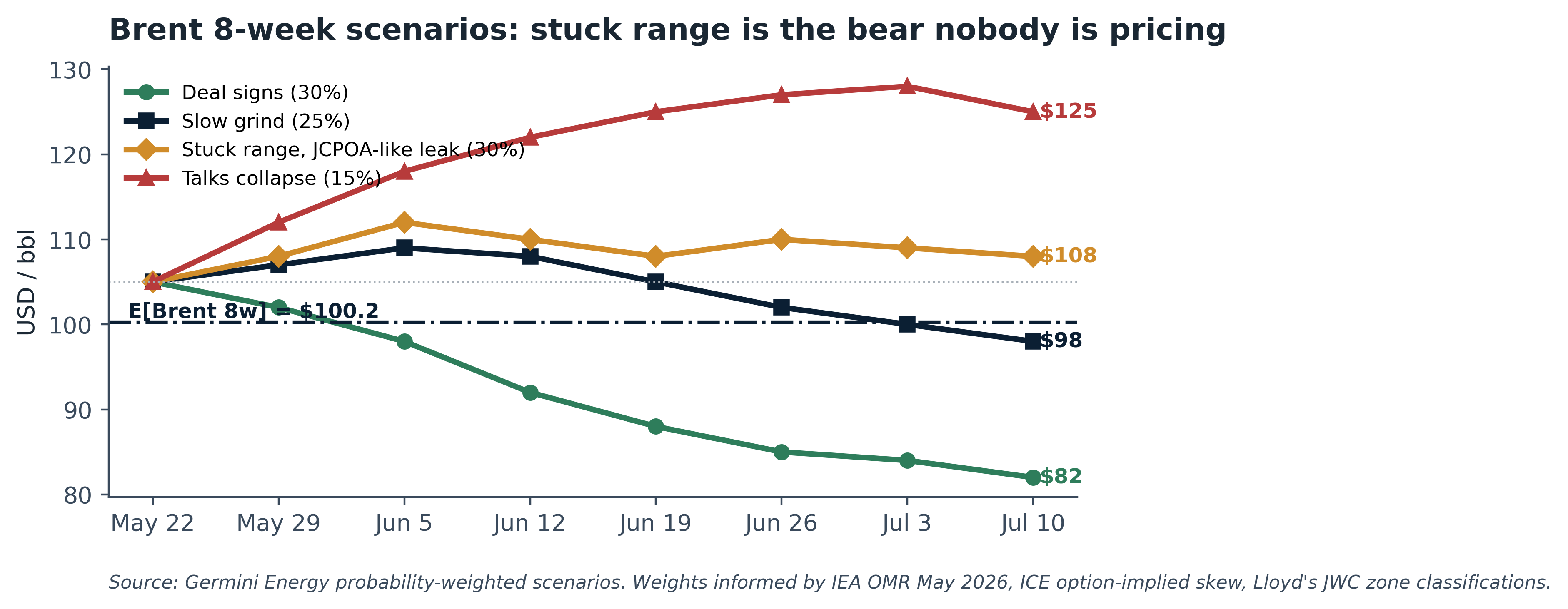

4. Key price levels with probability-weighted expected value

If the US-Iran framework is signed, expect Brent to test $100 / $96 supports quickly. If Friday slips without a deal, expect a retest of $110 and a potential print to $118. The probability-weighted expected value 8 weeks out is $100.25, essentially flat to spot. That is the math that justifies the pair trade detailed in the Forecast section, rather than a directional flat-price bet either way.

Deep Dive: The Pricing Mechanism Most Macro Coverage Is Missing

The Hormuz war-risk premium as a pricing input

The price discovery this quarter is happening inside Lloyd’s, not OPEC headquarters. That is the single most useful frame for the next eight weeks. The war-risk premium on a Hormuz transit moved from 0.15-0.25% of hull value in January to a peak of 7.2% in March and has stabilized at 5.5% in May. Translate it into per-barrel cost: a VLCC carrying 2 million barrels with a hull valuation of $120M paying a 5.5% premium is absorbing $6.6M of insurance cost on a single laden voyage, or roughly $3.30/bbl of pure premium.

The math gets sharper when you remember that most of the Asian refining complex relies on Gulf grades that come through Hormuz. Korean and Japanese refiners are absorbing either the premium or the alternative-grade arbitrage cost (Atlantic Basin barrels shipped long-haul). Either way, refined product cracks should reflect this. They have, partially. USGC ULSD vs WTI 3-2-1 cracks have held a $25-30/bbl premium against a normalized $12-15/bbl range. Singapore Gasoil 10ppm vs Brent cracks have held similar wartime levels.

When the market starts to price Hormuz reopening (as it did this week), the first leg sold is flat price, because flat price is the most liquid expression. The second leg, which lags by days or weeks, is the crack complex. Diesel cracks are sticky to the downside because the physical premium does not unwind until tonnage actually transits the strait safely. That gap, between flat-price unwinding and crack-spread unwinding, is the trade.

OPEC+ Quota vs Effective Production (post-UAE exit)

Important structural change this month: the UAE formally departed OPEC on May 1, 2026 after 59 years of membership, ending a long-running dispute over its 3.5 Mbd quota ceiling against its expanded ~5 Mbd capacity. This is the largest exit in the cartel’s history and reshapes the GCC bloc inside OPEC+. The remaining core (Saudi, Russia, Iraq, Kuwait, Iran-exempt, Kazakhstan, Algeria, Oman) raised the May quota by 206 kbd, but the gap between quota and effective production is now structural. Saudi, Kuwait, and Iraq are all running 0.5 to 1.0 Mbd below their notional ceilings because Hormuz tonnage is constrained. Iran is producing outside the quota framework entirely, with estimated output of 1.6 Mbd (+/- 0.3) loaded primarily at Kharg Island and via Gulf of Oman ship-to-ship transfers outside formal port records. The cohesion question is no longer whether quotas get raised again, it is whether the bloc keeps any pricing power once both the Hormuz premium collapses and the UAE operates as a free agent.

Brazil & LatAm Desk

Petrobras: P-79 onstream, but nameplate is not production

Petrobras delivered P-79 first oil three months ahead of the 2026-2030 plan, lifting Buzios installed nameplate capacity to roughly 1.33 Mbd. Important caveat: installed capacity is nameplate. Actual produced volumes typically lag 12-18 months as wells are tied in and the FPSO ramps to plateau. The headline is execution discipline, not incremental 2026 barrels.

ANP approved the production individualization agreements for Berbigao (Sururu and BVE-ITD/RJS-697), but this is one of three approval gates. Consortium board ratification is still pending. IBAMA (not ANP) renewed two additional exploratory well licenses for the Equatorial Margin; operational drilling requires both ANP (reservoir) and IBAMA (environmental) sign-off, and the two regulators do not move in sync. The B15 diesel mandate is in force per CNPE resolution; biodiesel margins are squeezed.

Brazilian diesel imports: the Hormuz flip

The picture here is dramatically different from the pre-war 2024-25 baseline. Through April 2026, Brazil imported roughly 355 kbd of diesel, with Russia supplying around 85% (Bloomberg / TV BRICS reporting puts the April share at 89.84% by value), USGC barrels at 12%, and Other (residual UK / Atlantic Basin spot) at 3%. The Hormuz closure in late February eliminated UAE and Saudi cargoes that together had been roughly 30% of the import slate. Russia took share aggressively at deep discount as its refining complex recovered from the 2025 Ukrainian drone campaign. Counterparties should note: Russian flows remain outside G7 oil price cap enforcement scope but each cargo’s title chain warrants independent verification. The MR USGC-Brazil arbitrage is structurally narrower than the prior baseline implies because Russian product is now the marginal barrel into Suape and Santos.

Brazilian spot prices and the policy response

From the May 25 Informe Platts via Federacao Brasil Com: S10 diesel FCA prices fell on the day in line with futures. Araucaria saw a 200 m3 immediate-delivery trade at PB +R$1,250/m3 with offers as high as PB +R$1,440/m3; Paranagua offers held at PB +R$1,400/m3. On the DAP side, USGC HO July -8 cpg was heard for arrival into Itaqui in the June 20-25 window, reflecting the freight relief Felipe’s desk has been watching. Gasoline followed crude lower; Itaqui offers PB +R$1,650/m3, Suape PB +R$1,750/m3, with liquidity thin on Petrobras-quota uncertainty in the North and Northeast.

Regulatory layer: under Decreto No. 12.923 (April 7, 2026), the federal government zeroed PIS/Cofins on fuels as a direct mitigation measure against the Middle East war impact. This is the pump-stability lever Lula’s team is pulling first, ahead of any direct Petrobras pricing intervention. Biodiesel DAP Paulinia (1-7 day delivery, all-in) was assessed at R$6,160/m3 on May 25, up R$40/m3 day-on-day. The B15 mandate (CNPE resolution) keeps biodiesel margins compressed at the blending point.

Forward-looking, on the downstream M&A tape: Acelen secured USD 1.5 billion in financing to build a biorefinery in Bahia, targeting 1 billion liters/year of SAF and renewable diesel via HEFA technology, start-up 2029. This positions Brazil as a credible LatAm hub for sustainable aviation fuel and heavy-transport renewable diesel and is the first material capital commitment in Brazilian downstream renewables this year. Worth watching as a leading indicator for similar mid-Atlantic financings.

OPERATOR OF THE WEEK: PETROBRAS

Sized view, not a generic WATCH: long PBR ADR vs equal-weight short basket of XLE components, 60/40 dollar-weighted, 12-month horizon. Entry on current levels. Stop on PBR underperforming the basket by more than 8% (signals political-asset thesis winning). Target +15-20% relative return on operational ramp and dividend recovery. Recognize the steelmanned bear: Lula’s election-year fuel-policy intervention could compress margins; this is the live risk and what the stop is for.

Market Sentiment

MY TAKE ON POSITIONING

Managed-money net long was cut by 47k contracts this week, the largest single-week reduction since November 2025. That is the speculative tape pricing the Hormuz reopening. Note the divergence: while flat-price positioning is unwinding, refinery margins remain wide and tanker day rates are sticky. Three different markets are telling three different stories. When they reconcile, they will reconcile through the crack complex, not flat price.

Forecast & Recommended Trade

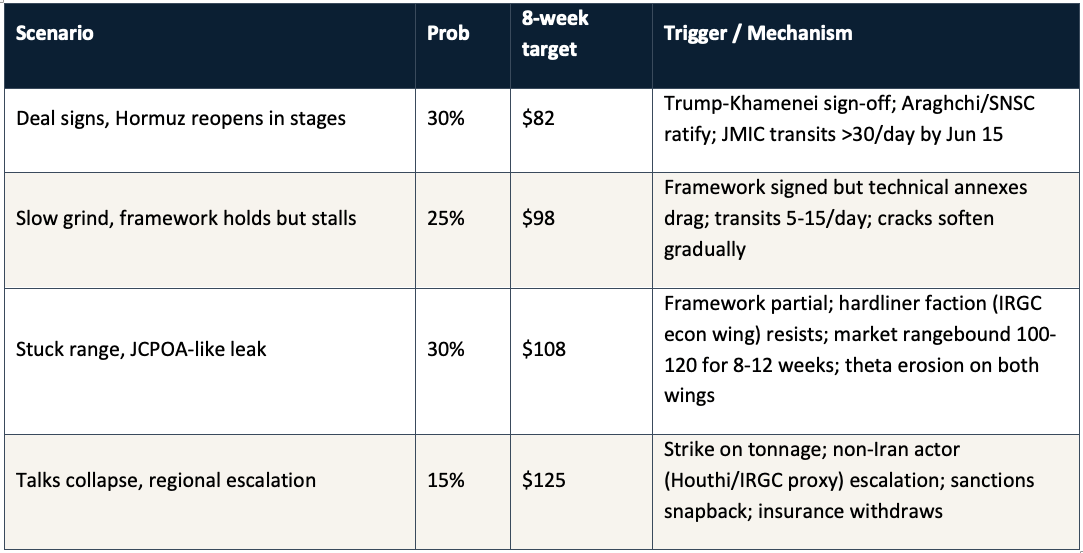

8-Week Brent scenarios (probability-weighted)

The expected value at these weights is $100.25/bbl, essentially flat to spot $105.10. That is what kills the directional flat-price trade and points to a relative-value structure instead. The stuck-range scenario at 30% is the bear case nobody is pricing: a JCPOA-like framework signed but functionally leaky, market rangebound $100-120 for 8-12 weeks, both wings of any straddle/strangle structure bleeding theta. The recommended pair trade addresses this directly.

Recommended trade: pair, dollar-neutral

Logic: in three of four scenarios (deal signs, slow grind, talks collapse), the pair is profitable or near-neutral. The stuck-range scenario is the only loss, and it is small (-$34k per $1M notional). This is the trade for an operator who believes the crack premium is anchored to physical reality and the flat price is reacting to news flow. Alternative trade for short-vol views: sell front-month Brent strangle (puts $95 / calls $115), collect rich vol at OVX 76; sized at 5-10% portfolio risk; stop on either wing break.

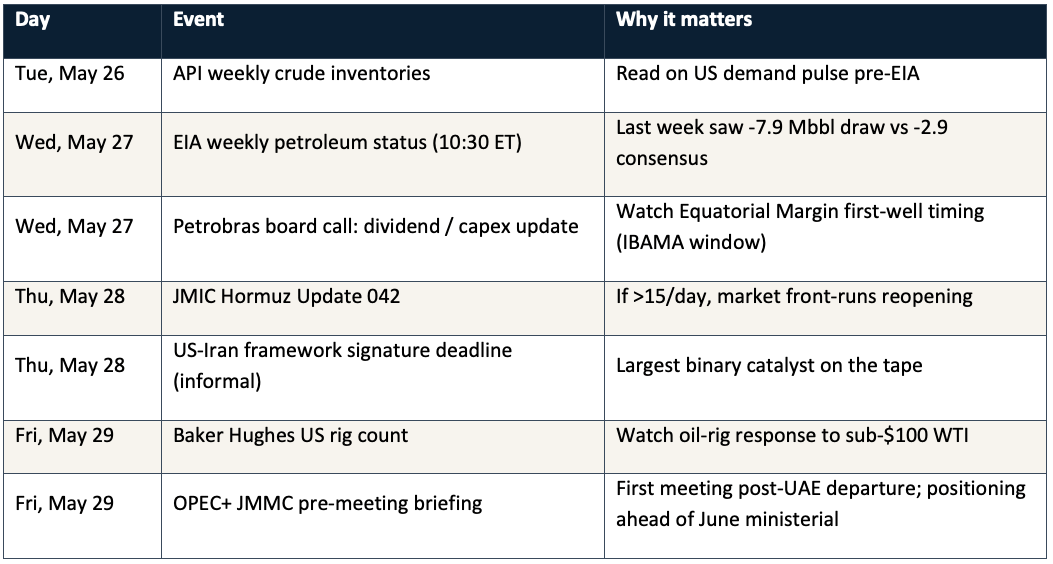

Calendar to watch

EDITORIAL SIGNAL

This week’s Substack develops the war-risk-premium-as-pricing-mechanism argument. The strongest counter, which I take seriously: flat price still leads cracks on macro headlines (China demand, Fed policy), and the war premium is a smaller overlay than the deep dive suggests. My disagreement: the magnitude this cycle is different - 5.5% of hull value is roughly 25x pre-war norms, large enough that the crack signal leads, not lags, in physical markets. Worth a Wednesday Flow deep cut.

------------------------------------------------------------

Germini Energy | Crude Oil & Refined Products Brokerage | Brazil & LatAm

intelligence@germinienergy.com | fgermini.substack.com

Proprietary intelligence prepared for authorized recipients. Not investment advice. Trade recommendations are illustrative; size and stop per your own risk framework.

Extended high prices for fossil fuels is a catalyst for alternatives investing. There would be so much more of it if AI weren’t sucking up most of the available investment capital.