The Horizon: Three Reopenings

Hormuz, Iran, and Venezuela are unwinding at the same time. The market is pricing each pipe individually. The expensive mistake will be on the second-order effects.

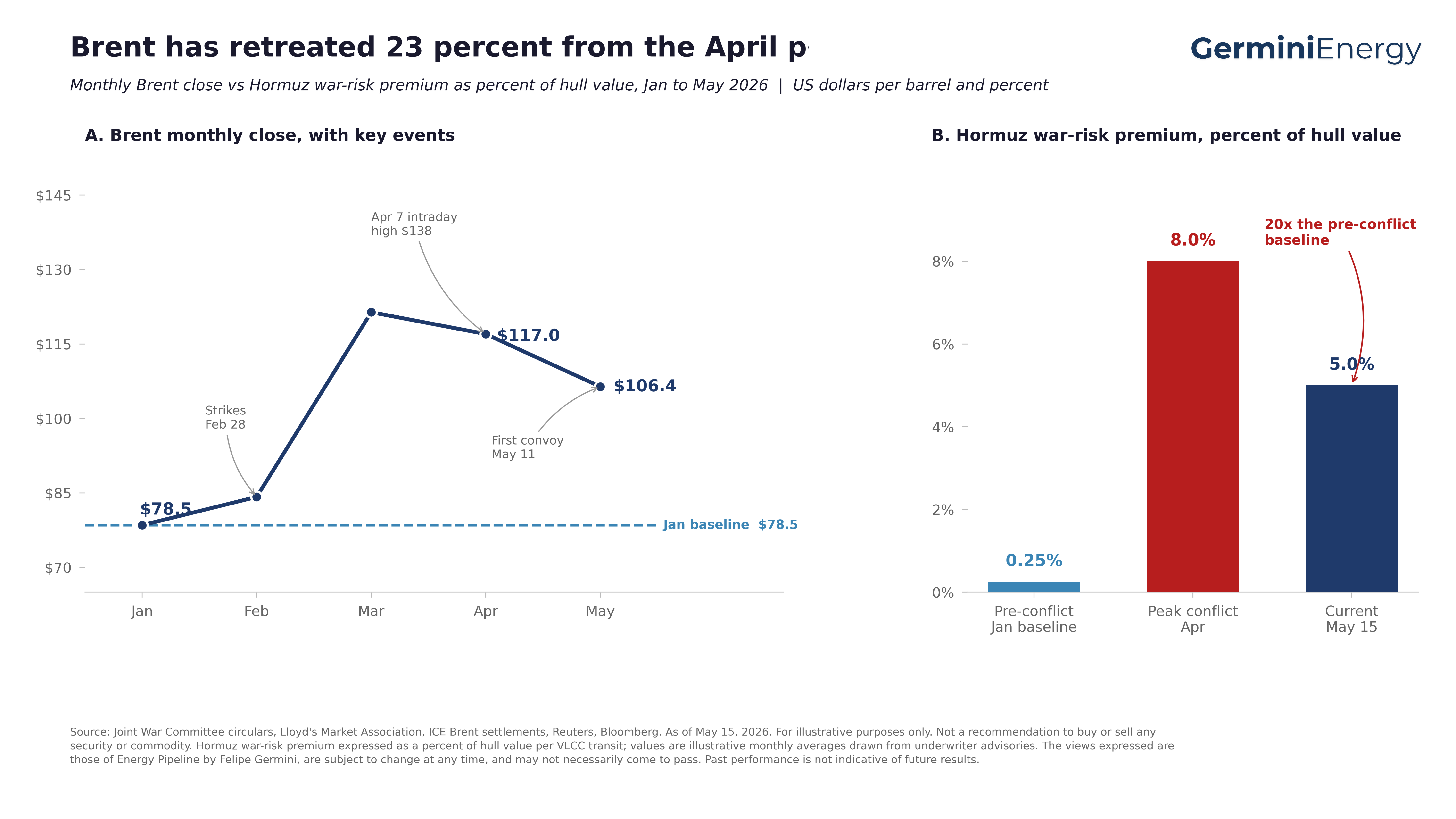

The math on a VLCC moving through Hormuz today runs five to seven million dollars in war-risk premium per voyage. Six weeks ago that same line item was a quarter of one percent of hull value. Roughly two hundred thousand dollars. The premium has not moved much in the last seven days, even with three British escort ships now in the Gulf and the first cleared lanes back in commercial use. That tells you something important about how this market resets, and how it does not.

Three supply pipes are being unwound simultaneously over the next six to twelve weeks. The Strait of Hormuz. Iranian crude. Venezuelan crude. Each carries a separate political clock, a separate counterparty stack, a separate set of buyers and sellers. The trade press is covering each as its own story. The forward curves are pricing each as its own story. The expensive mistake here will be on the second-order effects, not on the first-order barrels.

Brent settled at $106.40 yesterday, off from the April 7 print at $138, and roughly twelve dollars above where consensus had it six months ago. The market is reading the move as a relief rally on Hormuz reopening, framed against the UAE leaving OPEC May 1 and the seven remaining OPEC+ members agreeing on May 3 to add 188,000 barrels per day starting June. Saudi production sits at its lowest level since 1990. The cartel-discipline story has been replaced by a cartel-decomposition story. None of those framings are wrong. They are just incomplete.

The asymmetric clock

Here is the structural feature of the next two quarters the front-month Brent curve has not learned to price. Crude supply normalizes first. Freight does not normalize on the same clock. War-risk insurance normalizes last.

The strait clears, cargoes load, the trade press writes the relief rally. Suezmaxes and Aframaxes that spent the last six weeks redirecting Brazilian, West African, and US Gulf crude around the Cape into Asia priced six months of dislocation into their charter cards. They will not give that back on day one. Insurers want six to nine months of sustained quiet before they revert to pre-conflict war-risk underwriting. Premiums sit between three and eight percent of hull value, against a 0.125 to 0.4 percent pre-conflict baseline.

That asymmetry, supply quick, freight slow, insurance slowest, shows up in landed crude costs to Asian and Mediterranean refiners and in product spreads. It does not show up on the screen.

Hormuz: the toll booth that is not coming down

The strait was formally closed by the IRGC on March 2. The first VLCC convoy under UK escort cleared the eastern channel on May 11. That single convoy is the basis for the reopening headlines. Pre-conflict war-risk premium per VLCC transit was roughly two hundred thousand dollars. Today it runs three million to eight million. Insurers want sustained quiet before they normalize cover. The pipe reopening and the toll booth coming down are two different events on two different clocks.

Iran: half-open and politically unstable

Ali Khamenei has been dead since February 28. The Trump-Tehran one-page memo remains on the table, currently described in Washington as on life support after Trump rejected Tehran’s last proposal. The administration’s condition is a defined-period nuclear-program halt, ten years, plus surrender of the existing 440 kilogram enriched-uranium stockpile. Tehran is delaying. Sanctions were eased on certain Iranian stockpiles March 20, then OFAC added twelve more entities to the SDN list this Monday. The contradiction is the policy: Trump is running sanctions enforcement as a negotiating clock, not as an embargo. Iranian crude is moving from Persian Gulf loading points under shadow-fleet cover. China is functionally the only buyer. India has stopped. Turkey is hedging.[^1]

[^1]: This editorial discusses sanctions architecture as observable market structure, not as commercial advice. Counterparty decisions involving sanctioned entities require direct legal counsel.

Venezuela: the cleanest reopening, the most underpriced

Maduro was captured by US forces on January 5. The interim government under Delcy Rodriguez moved fast. By late January the National Assembly had approved the oil-law reform giving foreign producers full autonomy on production, export, and cash repatriation. Chevron, Repsol, ENI, and Reliance Industries have all filed for individual licenses to expand operations beyond Chevron’s existing 140,000 bpd joint-venture stake. The EIA put potential output upside at up to twenty percent over the coming months. That upside is contingent: on US license issuance pace, on the Venezuelan National Assembly continuing on the reform path, and on the next Venezuelan election producing a government aligned with current US policy. None of those are settled.

The two-billion-dollar US-Venezuela supply deal Rodriguez signed in March established the floor. Heavy Merey crude is moving into US Gulf refineries again at posted prices. PDVSA’s structural counterparty role is being unwound. The Faja del Orinoco can scale. Twelve to eighteen months out, this is the biggest non-OPEC supply increment available on the planet, and it is being priced as a footnote in a market obsessed with Hormuz.

That mispricing will not last.

____________________________________________________________

This is for the trader and capital allocator who has read the Hormuz reopening headlines and is asking what to do about it before consensus catches up.

Below the cut: the three-scenario Q3 Brent matrix with implied trade structure; the hard bear case nobody is engaging; the Iran counter-consolidation argument with the single political signal that resolves it; the discount-grade compression with port-, spec-, and month-level detail; the Brazilian grade and Brasília-channel picture for the readers running heavy export volumes; the single ratio that tells you which scenario is unfolding; and five sized strategic calls with position, stop, and time horizon.

Paid subscribers also receive this edition’s presentation pack, twelve slides covering the scenario matrix, the Hormuz war-risk to Atlantic Basin freight ratio dashboard, the counterparty exposure map, and the sized strategic calls, formatted for boardroom use.

Upgrade to read the full edition.

____________________________________________________________