The Insurance Geometry That Replaced the Strait

Iran did not close the chokepoint. The insurance market did. Here is what that costs, who pays, what does not snap back when the strait reopens, and how to position around it.

On Tuesday evening, US Central Command struck two IRGC naval vessels in the Strait of Hormuz that were reportedly laying mines, and a surface-to-air missile site at Bandar Abbas. Iran’s Foreign Ministry called the strikes a violation of the April 8 ceasefire and threatened retaliation. Within hours, the State Department reaffirmed that the framework memorandum of understanding now under negotiation in Muscat still gives both sides sixty days to reach a full peace deal. By Wednesday morning, Brent had given back two-thirds of the previous session’s optimism rally. The Lloyd’s market did not move at all.

Bloomberg’s tanker desk has been carrying the same headline number since March 17: war-risk cover for a Hormuz transit costs five percent of vessel value. A hundred-million-dollar VLCC pays five million dollars to clear the strait. The number is not the story. The geometry behind the number is. And the reason the insurance market did not move on Tuesday night is the reason most of what is about to be written in the trade press over the next ten days will produce the wrong trade.

Almost three months into the Hormuz crisis, the conversation is still dominated by missiles, mines, and the rhythm of the IRGC’s next move. That framing makes for good copy. It also misreads what has happened. The strait has not been closed by Iranian ordnance. It has been closed by the underwriters. The military theater forced the insurance market to reprice; the insurance market then forced the tanker market to reroute, slow down, or refuse to move. The chokepoint is now an accounting chokepoint as much as a geographic one. That is the piece of architecture that does not reverse when the diplomats finish in Muscat.

This piece sits inside the Chokepoints pillar of The Flow. The argument: when the binding constraint of an energy trade moves from physical infrastructure to insurance pricing, the trade does not normalize when the physical constraint is removed. It normalizes when the paper unwinds, which is a slower and more political process.

Three positions, three continents, this week

Three positions taken in the past seven days, on three continents, frame the disagreement perfectly.

In Tehran, on May 18, Iranian state media announced the formal launch of “Hormuz Safe,” a digital insurance platform settling in Bitcoin that offers cover to vessels willing to transact directly with Iran. Al Jazeera reported a ten-billion-dollar annual revenue target. The platform appears to be operated by the IRGC’s Khatam al-Anbiya commercial arm rather than the Ministry of Petroleum, and that matters more than the launch itself: an IRGC-run product will not be dismantled in a ceasefire that leaves the IRGC intact. The Ministry of Petroleum wants oil revenues normalized. The IRGC wants a permanent toll on the strait. Those two institutions will not lose interest in this platform on the same day. Iran is not asking the West for the keys to the strait. Iran is selling its own keys, and the seller is not the Ministry that signs the peace deal.

Nothing in this piece constitutes guidance on counterparty selection or sanctions compliance. Payments to Hormuz Safe by US persons or entities subject to US jurisdiction would expose them to secondary sanctions, and no operator in our network is using the platform.

In London, on May 22, the International Group of P&I Clubs reissued its standing position that any payment to a sanctioned entity for safe-passage cover voids the underlying P&I policy. The IG covers roughly ninety percent of world ocean-going tonnage by gross tonnage. The statement is not a recommendation. It is a price signal that closes the door on dual coverage.

In Abu Dhabi, ADNOC’s marketing arm continued through last week to load voyages with explicit war-risk surcharges built into the FOB price. They are not arguing about who should pay. They are pricing as if the surcharge is now permanent.

Three positions. Three different bets on how long the insurance architecture stays in place once Hormuz reopens. Tehran (IRGC) is betting on a parallel market that survives any deal Khamenei’s successor signs. London is betting on the sanctions regime holding. Abu Dhabi is betting that the price has been reset for years, not months. All three of those bets cannot be right.

The strait did not close. The insurance closed.

That is the line I would put on the office whiteboard. It is short, accurate, and it inverts the trade-press framing. Once a tanker desk understands that the binding constraint is paper, not water, the entire trade plan changes.

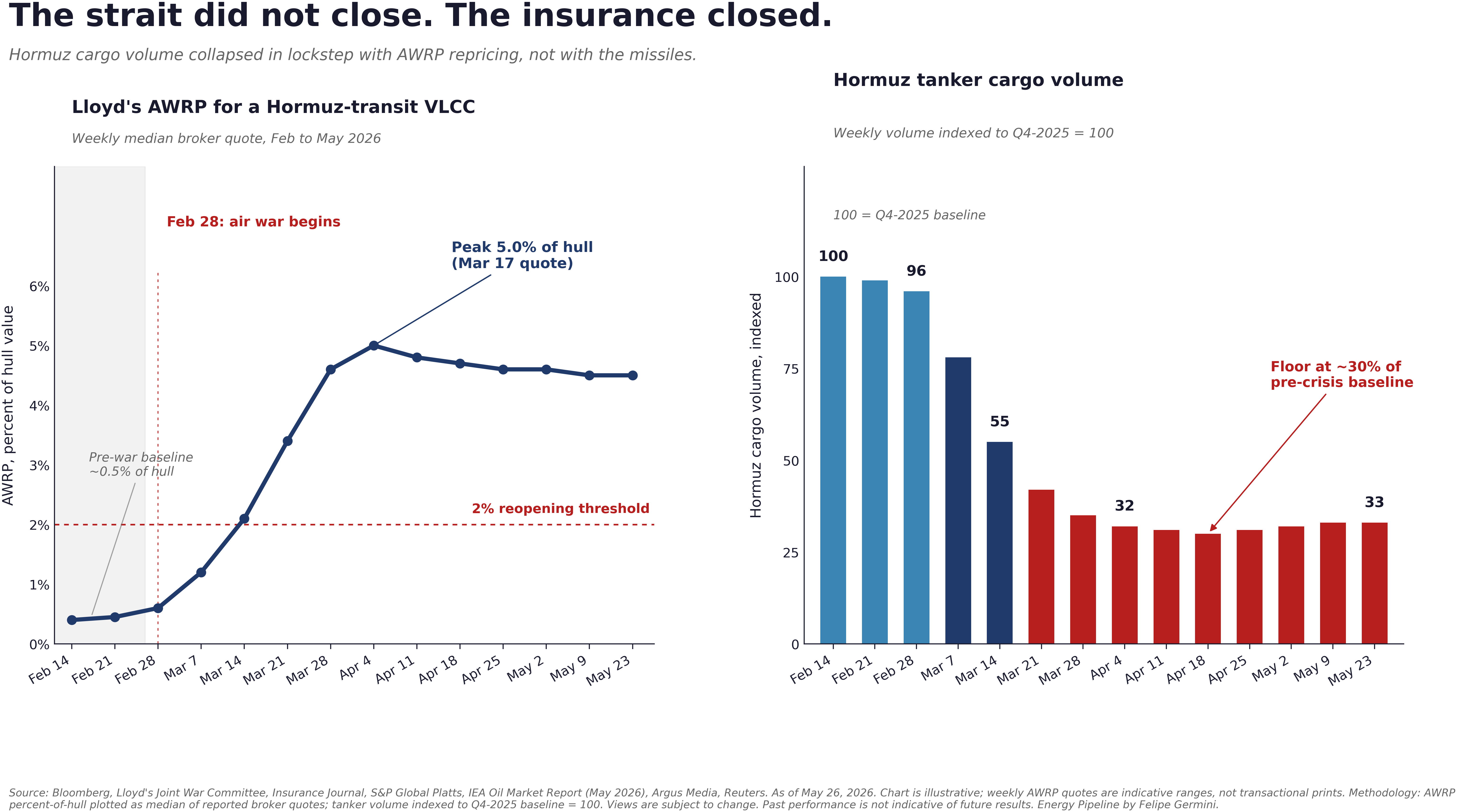

Chart 1. Lloyd’s AWRP and Hormuz cargo volume, Feb to May 2026

Here is how the insurance closure actually happened. The sequence matters.

First, on February 28, the US-Israeli air war on Iran triggered Lloyd’s Joint War Committee to extend the listed war-risk area to cover the entirety of the Persian Gulf and the Strait of Hormuz. That is a binary administrative act. Once a route is listed, every hull underwriter and every P&I club requires a separate Additional War Risk Premium per voyage, on top of standard cover.

Second, between March 3 and March 17, the AWRP quote jumped from roughly half a percent of hull value to five percent. That is not price discovery in the normal sense. It is a refusal to write the cover at any rational price, signaled through a number nobody actually wants to pay. The underwriters were telling charterers: do not ask us to insure this.

Third, charterers responded the only way they could. Hormuz cargo flows slowed to roughly thirty percent of pre-crisis volumes within three weeks, with two distinct adaptations on either side of the curve. The biggest national producers (Saudi Aramco, ADNOC, QatarEnergy) self-insured or moved cargoes on owned tonnage with sovereign-backed cover. The middle layer, the long tail of independent traders and smaller refiners, simply stopped lifting.

Fourth, the political response from Washington and Brussels arrived late. The US announced a twenty-billion-dollar reinsurance backstop in mid-April, intended to revive commercial traffic. The number sounds large. It is roughly equivalent to two weeks of insured Hormuz transit value at pre-crisis volumes. It is a stopgap, not a structural fix. And it does nothing to address what happens when the strait reopens.

Architecture: this has happened before

Insurance has been the silent chokepoint of energy trade for as long as there has been energy trade. The 1973 Yom Kippur war produced a tanker insurance spike that took roughly eighteen months to fully reverse, well after the political crisis had ended. The 1980s Tanker War in the Persian Gulf, between Iran and Iraq, produced AWRP quotes that peaked at seven percent of hull value and never fully normalized for the duration of the conflict; vessels routed wide of Kharg Island for almost a decade. The pattern is consistent. Insurance prices set quickly, and they normalize slowly. The trade desks that understood this in 1973 and 1987 made money on the way up and on the way down. The ones that did not went under.

The 2026 Hormuz crisis fits this lineage, but with two new features. The first is the Bitcoin-settled parallel insurance market. There has never been a sanctioned chokepoint state offering its own insurance product before. The second is the size of the US reinsurance backstop, which signals that Western governments now understand they need to act as insurers of last resort to keep their own commercial fleets moving. Both of these are structural innovations, and both of them stay in place after Hormuz reopens.

What this looks like on the ground, in operator language: charterers are being asked to sign Letters of Indemnity that the carriers’ P&I clubs do not actually back. Owners are demanding voyage-specific cover on top of standard hull. Demurrage clocks are being negotiated under additional war-risk language nobody had to draft six months ago. Charter parties that priced AG-USG voyages at a single freight rate now contain a war-risk pass-through tied to the Lloyd’s quote of the week. The paperwork itself has changed shape.

This is for the trader and the broker who have been watching the Hormuz premium build for ten weeks and are now trying to decide whether to lift a cargo on the reopening trade. Tuesday night’s strikes raised the stakes on getting that timing right. The wrong week to lift, on the wrong assumption about how fast insurance unwinds, costs more than the spread.

Below the cut: the “Two ways this view dies” section naming the specific events that would invalidate the thesis, and what changes after Tuesday night’s strikes. A dated calendar of six catalysts between May 27 and June 18, visualized as a timeline. The Flow trade map, four longs, three shorts, and the one cleanest macro expression of the insurance-as-chokepoint thesis, each with entry zones and stops. A regional impact note on what the rerouted Brazilian diesel barrel does next, and the three Brasília actors who decide when the corridor flips back.

Paid Flow subscribers also receive this edition’s presentation pack, ten slides covering the AWRP pricing timeline, the catalysts calendar, the trade map, and the Atlantic Basin impact matrix, formatted for boardroom use.

Upgrade to read the full Flow piece: $8/month standard.