The Kremlin's Hormuz Windfall

How America's War Is Financing Russia's Oil Renaissance

Five weeks into the Hormuz closure, the crude market has settled into a strange equilibrium. Brent oscillates between $102 and $106. Traders have priced in the shock. The initial panic has matured into something resembling routine. But underneath that surface calm, something far more consequential is taking shape.

Russia is having its best month in the oil market since before the invasion of Ukraine.

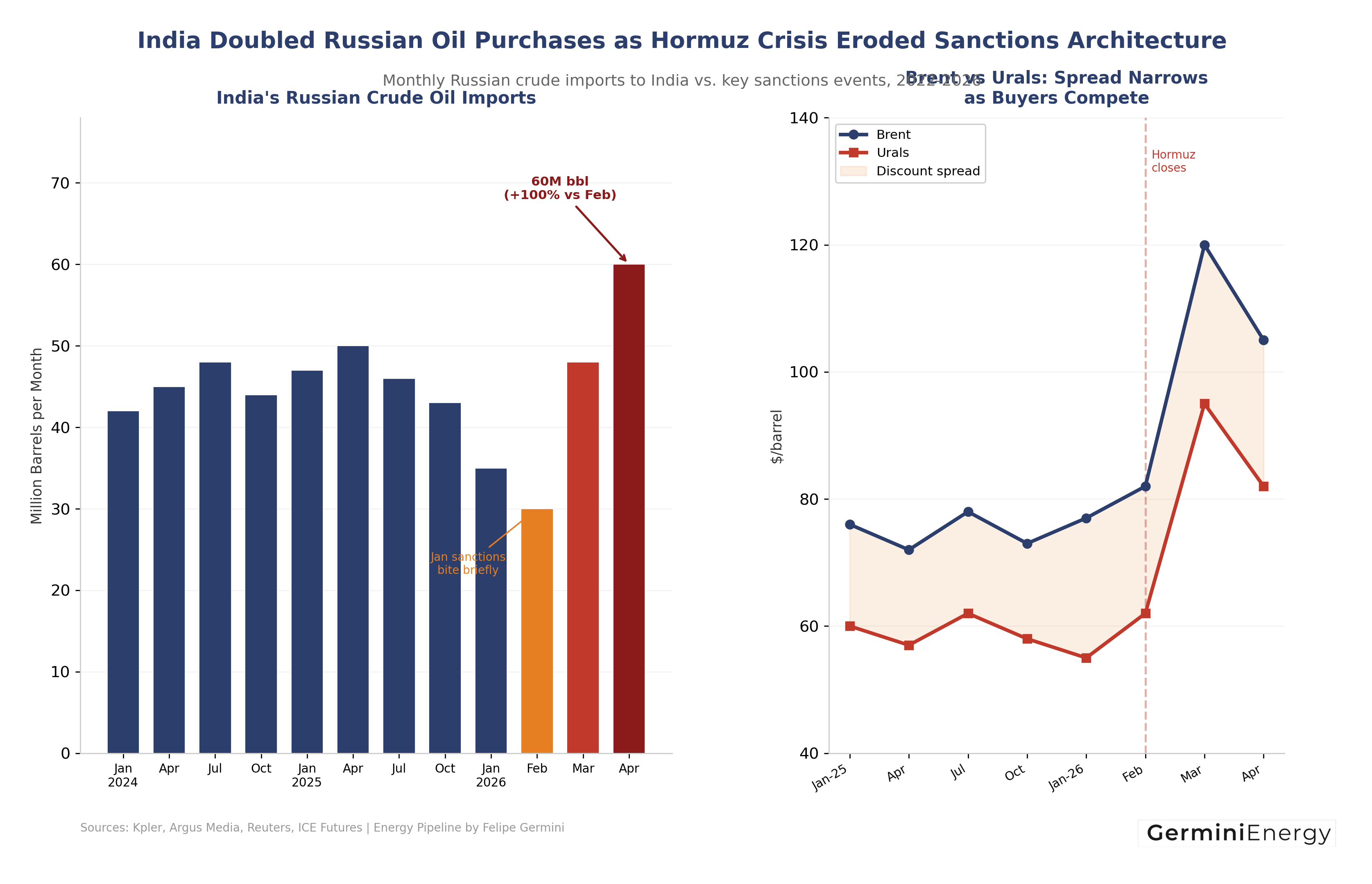

India is heading to import 60 million barrels of Russian crude in April, as per latest line-up. That is double the February figure. Double. Not a marginal increase driven by seasonal demand or refinery maintenance schedules. A structural doubling, driven by the simple arithmetic of a world that suddenly needs every available barrel that does not transit the Strait of Hormuz.

The sanctions architecture that Washington spent three years assembling — the price cap, the tanker designations, the shadow fleet enforcement, the secondary sanctions threats — is not holding. It was already fraying before Hormuz. Now it is being actively dismantled by the same government that built it.

I have spent enough years watching commodity cycles to know when a policy framework is bending under its own weight. The signs are always the same: quiet exemptions, vague language in enforcement notices, and a growing gap between official statements and observable trade flows. All three signs are present now. And they are accelerating.

The General License That Said the Quiet Part Out Loud

On March 12, the U.S. Treasury Department issued a general license permitting the purchase and delivery of otherwise sanctioned Russian oil already loaded on vessels. The license runs through April 11. Read that again. The United States government, while prosecuting a war against Iran that has closed the world’s most critical oil chokepoint, simultaneously authorized the delivery of Russian oil that its own sanctions regime had previously blocked.

The logic is transparent: Washington needs every barrel it can get, and ideology has collided with thermodynamics. You cannot simultaneously remove 20 percent of global oil supply from the market via Hormuz and maintain a sanctions regime that constrains another major supplier. The physics do not allow it. The Treasury Department understands this. The State Department may not. The Pentagon certainly does.

I worked in Russia long enough to understand how Moscow reads signals from Washington. A general license is not just a legal instrument. It is a message. And the message Moscow received on March 12 was clear: your barrels are needed, and we will look the other way while they flow.

The Atlantic Council published a sharp analysis last week noting that these waivers risk “sustaining Russia’s war effort amid the Iran war.” That framing is correct but incomplete. The waivers are not an isolated policy accommodation. They represent the structural failure of a sanctions strategy that was designed for a world with 2-3 million barrels per day of spare capacity and comfortable shipping lanes. That world no longer exists.

India: The Biggest Buyer in the Room

India’s 60 million barrels in April is not just a headline number. It represents a strategic shift in how New Delhi sources its crude. Before Hormuz, India was already the largest buyer of Russian seaborne crude. After Hormuz, it has become Russia’s most important customer by a wide margin.

The Urals-Brent spread has narrowed from $16-18 per barrel in early 2025 to roughly $20-23 in April, but at a Brent level of $105, that still means Urals is trading around $82-85. For context, Russia’s federal budget for 2026 was built on an assumption of $63 Brent. Even after accounting for the discount, Moscow is collecting revenue far above its fiscal breakeven. Every month the Hormuz crisis persists, Russia’s budget surplus grows.

The mechanism is worth understanding. Indian refiners — Reliance’s Jamnagar complex, Indian Oil Corporation, Nayara Energy (itself 49 percent owned by Rosneft) — are running at maximum throughput. They are processing discounted Russian crude, refining it into diesel and jet fuel, and exporting finished products to Europe and Africa at international prices. The margin arbitrage is enormous. The refiners win. Russia wins. The only losers are the architects of the sanctions regime, who are watching their policy evaporate in real time.

The EU’s Split Personality on Russian Energy

Brussels, to its credit, is trying to maintain pressure. The European Union announced that it will prohibit the purchase, import, or transfer of Russian LNG effective April 25. This is a meaningful step. Russian LNG accounted for roughly 16 percent of European LNG imports in 2025, and cutting that supply during a period of extreme global gas tightness requires real political will.

But the contradiction is glaring: Europe is tightening the noose on Russian gas while the oil noose loosens by the day. The April 25 LNG ban will redirect Russian cargoes to China and India — the same countries that are already absorbing Russia’s displaced crude oil. The net effect on Moscow’s total energy revenue is minimal. Russia loses European gas revenue but gains additional Asian oil revenue, at higher prices, with shorter payment cycles and less regulatory scrutiny.

This is not a criticism of Europe’s intentions. It is an observation about the structural limitations of unilateral sanctions in a disrupted market. When the supply stack is this tight, every barrel finds a home. When the IEA calls Hormuz the “greatest global energy security challenge in history” — and that is a direct quote from the head of the agency — sanctions enforcement becomes a luxury that markets cannot afford.

OPEC+ Meets Saturday: Russia Holds the Cards

The OPEC+ ministerial meeting on April 5 — three days from now — will be one of the most consequential in the group’s recent history. The eight countries that agreed to the 206,000 barrel-per-day increase for April face a paradox: they have committed to restoring supply, but the Hormuz closure means that several of them — Iraq, Kuwait, the UAE — cannot physically export their quotas.

Iraq and Kuwait have already begun shutting in production. Their export terminals on the Persian Gulf are either inaccessible or operating at a fraction of capacity. The UAE has some flexibility through its Fujairah terminal and pipeline bypasses, but volumes are constrained. The countries that can actually deliver incremental barrels to the global market are, in order: Saudi Arabia (via Red Sea terminals), Russia (entirely outside the Hormuz chokepoint), and to a lesser extent, the West African and Latin American producers.

Russia, in other words, is one of the only OPEC+ members whose production can actually reach the market. This gives Moscow extraordinary bargaining power heading into Saturday’s meeting. Any decision to increase quotas benefits Russia disproportionately, because Russia can ship while others cannot. Any decision to hold production steady keeps prices elevated, which also benefits Russia. It is a rare geopolitical position where both outcomes favor the same actor.

Think about what that means for internal OPEC+ dynamics. Saudi Arabia has traditionally held the swing producer role. But a swing producer is only useful if it can swing barrels to market. Right now, the Saudis can ship via Red Sea terminals — Yanbu and Ras Tanura’s pipeline-connected alternatives — but their Persian Gulf terminals at Ras Tanura itself are constrained. Russia faces none of these limitations. Primorsk, Novorossiysk, Kozmino — all operational, all outside any conflict zone, all loading tankers around the clock.

The $200 Question

Wall Street analysts and U.S. government officials are now openly discussing the possibility of $200 oil. Bloomberg reported last week that this scenario is under active consideration in Washington. The arithmetic is simple: if Hormuz remains closed through summer, and OPEC+ cannot compensate for the lost volumes, and strategic petroleum reserve releases prove insufficient, then the market faces a structural deficit of 8-12 million barrels per day.

I have been in this business long enough to know that $200 forecasts are usually wrong. They were wrong in 2008, when Goldman’s $200 call preceded a crash to $33. They were wrong in 2022, when the initial shock of the Ukraine invasion sent prices to $139 before settling back to $80. Extreme price calls tend to be right about the direction and wrong about the magnitude.

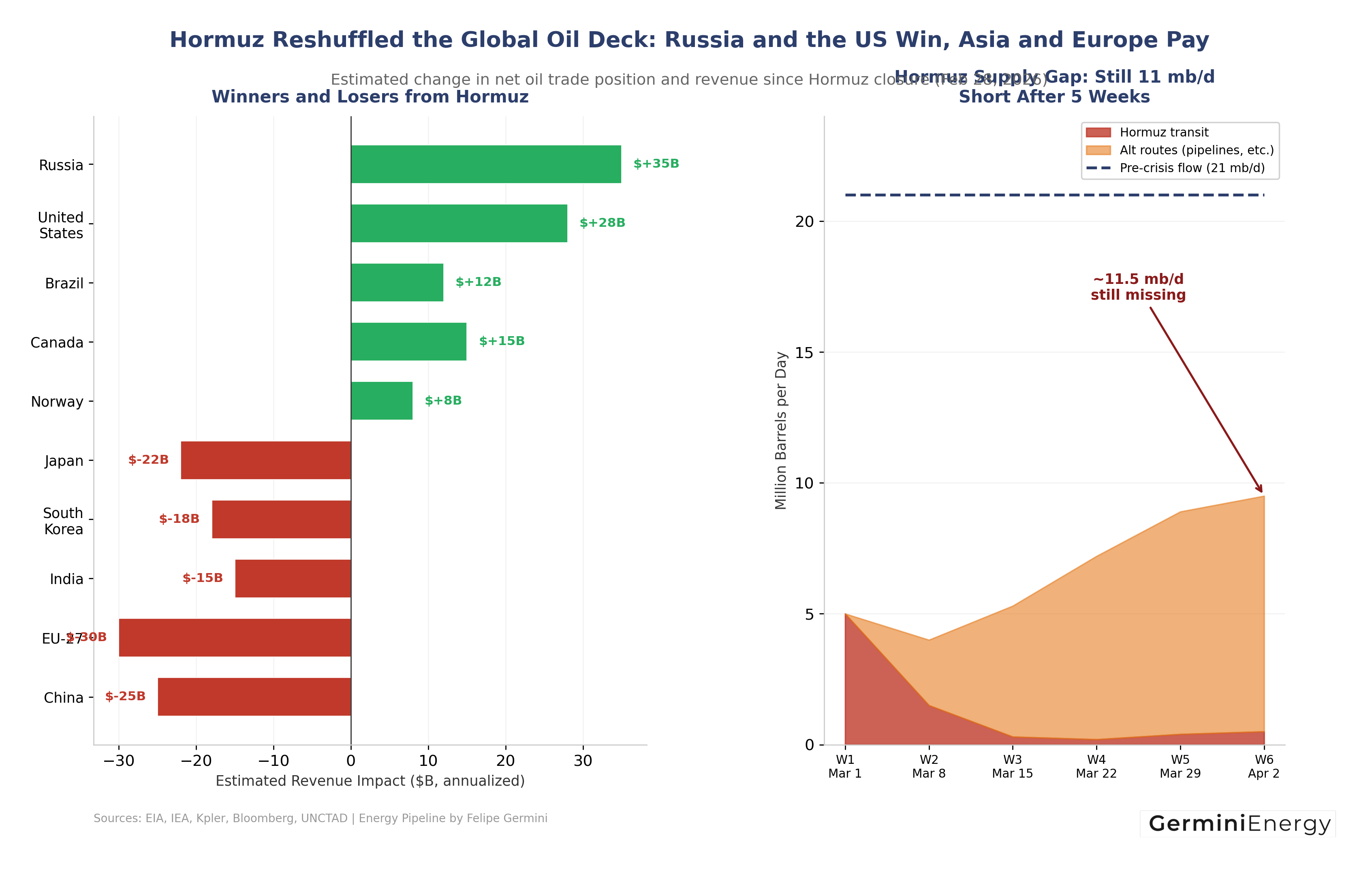

But this time the physical dislocation is larger than anything the modern oil market has experienced. The 1973 Arab oil embargo removed approximately 4.4 million barrels per day from the market. Hormuz, at its pre-crisis flow rate, carried 21 million barrels per day. Even with partial rerouting through pipelines and alternative ports, the net loss is still around 11-12 million barrels per day after five weeks. That is roughly three times the 1973 embargo.

The question is not whether $200 is possible. It is whether the demand destruction necessary to rebalance the market will arrive before the price gets there. High prices are already triggering behavioral changes: airlines are cutting routes, heavy industry is curtailing output, and governments across Asia and Latin America are intervening with subsidies and price controls. Brazil’s own Provisional Measure 1,340, which slapped a 12 percent export tax on crude and a 50 percent levy on diesel exports, is a direct consequence of this price environment.

What the Comfortable Consensus Gets Wrong

The prevailing market narrative goes something like this: Hormuz is terrible, but sanctions on Russia are holding, OPEC+ is managing supply responsibly, and the conflict will resolve within months. This narrative is wrong on at least two of those four counts.

Sanctions on Russia are not holding. They are being actively waived by the country that imposed them. The general license for loaded vessels, the tolerance of Indian and Chinese purchasing at volumes far above pre-war levels, the absence of secondary sanctions enforcement against Nayara Energy (again: 49 percent Rosneft-owned) — these are not minor accommodations. They represent a policy regime in retreat.

And the assumption that the conflict resolves quickly is contradicted by the latest signals from Washington. President Trump’s prime-time address this week vowed further escalation in the coming weeks, not de-escalation. That address sent Brent above $106 before subsequent walk-back comments pulled it back to $103. The market is treating every Trump statement as a tradeable event, which tells you how thin the informational edge is right now.

The comfortable consensus wants the Hormuz crisis to be temporary and the sanctions regime to be permanent. The reality is closer to the opposite: Hormuz may redefine global energy flows for years, while the sanctions regime is being hollowed out in real time.

The View from Here

I have operated across Russia, the Middle East, Latin America, and West Africa over two and a half decades. I have watched sanctions regimes come and go. The common pattern is always the same: sanctions work best when the sanctioned country produces something the world can live without. When it produces something the world needs desperately — and crude oil at $105 qualifies — the sanctions bend, and then they break.

Russia is not just surviving the Hormuz crisis. It is thriving. Moscow’s fiscal position has improved every month since February. Its customer base in Asia has expanded. Its bargaining position within OPEC+ has grown. And the Western coalition that spent three years trying to constrain Russian energy revenue is now quietly facilitating its flow.

Saturday’s OPEC+ meeting will reveal whether the group can even pretend to manage supply in an environment where half its members cannot physically export. My expectation is that the meeting produces a cautious statement, a modest headline increase, and an implicit understanding that the actual allocation of global supply is being decided not in Vienna but by shipping lanes, insurance markets, and sanctions waivers.

The real allocation of power in this market is not where the headlines suggest. It sits in the tankers moving Russian crude to Jamnagar. In the Treasury Department offices where sanctions licenses are quietly extended. In the pipeline corridors that bypass the Strait entirely. The visible market is a sideshow. The invisible one is where the money is moving.

There is a term I learned early in my career, working oilfield operations in places where policy and reality rarely agreed: operational truth. It means the reality on the ground as opposed to the story being told in corporate offices or government briefings. The operational truth of the current oil market is that Russian crude is flowing at volumes not seen since before February 2022, at prices that exceed Moscow’s fiscal requirements, into refineries that are converting it into products that end up in the very countries trying to sanction it.

That is not a policy failure in the conventional sense. It is the market asserting itself over politics, the way it always does when the imbalance between supply and demand is severe enough. The only question now is whether anyone in Washington, Brussels, or Tokyo is willing to acknowledge what the tanker tracking data already makes obvious.

And right now, a disproportionate share of that money is moving toward Moscow.

About the author: Felipe Germini is an energy executive and strategic advisor with 25+ years across upstream operations, downstream commodities, and M&A. Former Country Managing Director for Brazil at a major oilfield services company. Founder of Germini Energy, a crude and refined products brokerage. Publisher of Energy Pipeline on Substack.

Energy Pipeline by Felipe Germini — weekly editorial on energy markets, geopolitics, and industry dynamics. Subscribe on Substack.