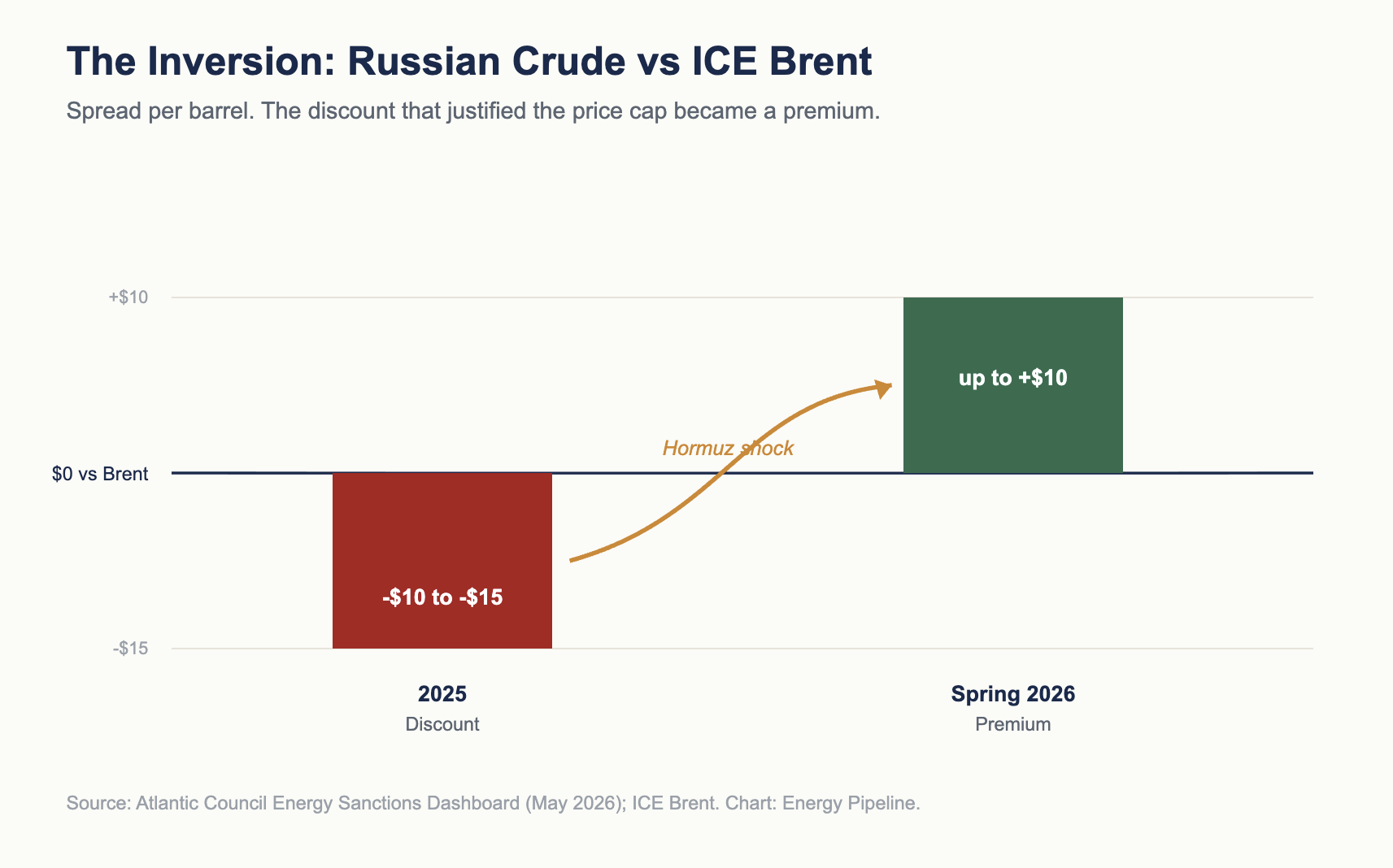

Russian crude is trading at a premium to Brent. Read that line twice, because it ends an argument Washington and Brussels have been having with themselves since 2022.

The entire Western sanctions architecture rested on one number. The discount. The G7 price cap, the European push toward a 44 dollar ceiling, the shadow fleet math, the insurance bans, every piece of it assumed Russia would sell cheap because it had nowhere else to go. The discount was the proof the policy worked. It was the scoreboard.

As of this week, that scoreboard reads in Moscow’s favor. The Atlantic Council’s Energy Sanctions Dashboard, the one half my inbox forwarded last week, puts Russian grades at premiums of up to ten dollars over ICE Brent. It mentions this almost in passing, three screens down, wrapped in cautious think-tank prose. I will not be that polite. The price cap is dead. The only open question is whether anyone in Treasury will say so out loud before June 17.

Chart 1. The spread that justified the entire price cap has flipped sign.

What actually happened, stripped of drama

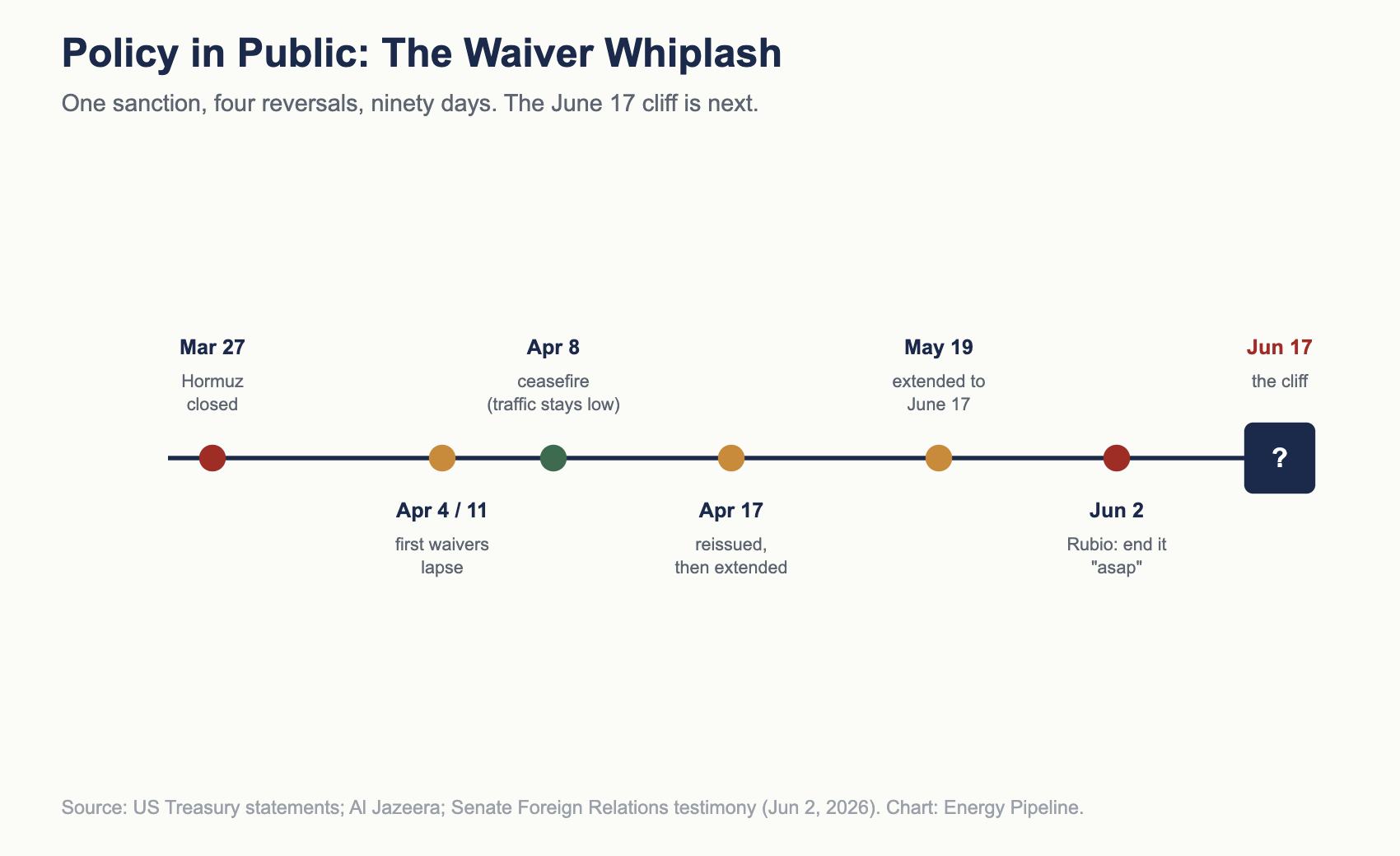

Here is the sequence. In late March, the Strait of Hormuz effectively closed. Roughly a fifth of the world’s seaborne oil moves through that gap of water, and for the first time the IEA reached for a phrase it had never used before: the largest supply disruption in the history of the oil market. A ceasefire was announced on April 8. Traffic never returned to where it was. Tankers still treat the Gulf as a war zone because, functionally, it remains one.

That is the supply shock. Now the policy response.

Washington, staring at a Gulf it could no longer count on, did the one thing it swore it never would. It opened the door to Russian barrels. Bessent issued narrow waivers, let them lapse, reissued on April 17, then extended again. The latest extension runs to June 17. On June 2, Rubio sat in front of the Senate Foreign Relations Committee and said the administration wants to kill the waivers as soon as we possibly can. Two senior officials, pointing in opposite directions, on the same policy, in the same month. That is not strategy. That is a government improvising in public.

Brent sits near 92 dollars as I write, down roughly 20 percent from the spring panic peak, holding in a 90 to 100 band while the market waits to see whether the ceasefire holds. The calm is borrowed. The structure underneath it has changed in ways that will outlast the headlines.

Chart 2. One sanction, four reversals, ninety days, and a cliff on June 17.

The scale nobody wants on the table

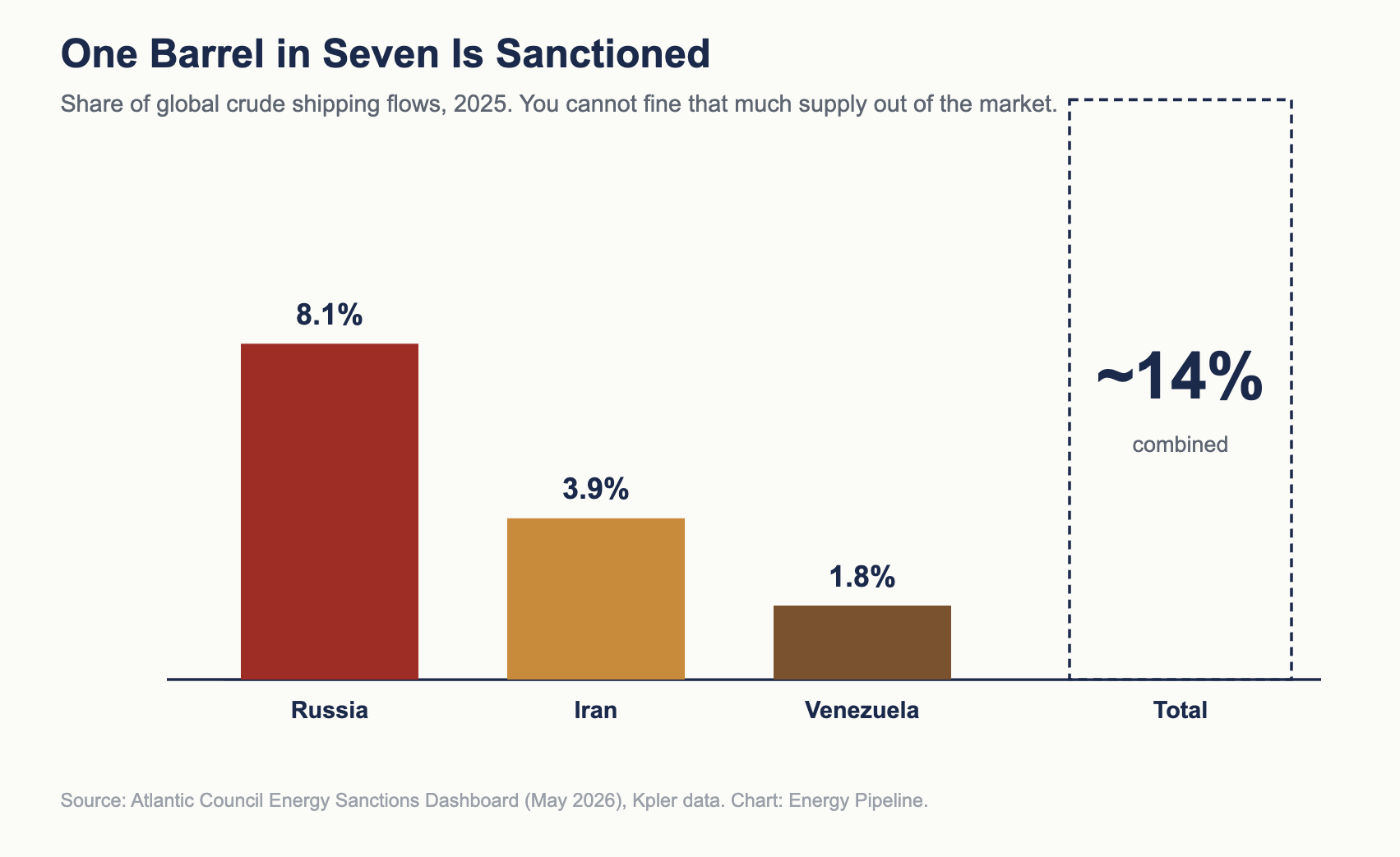

Three sanctioned regimes, Russia, Iran, and Venezuela, accounted for almost 14 percent of global crude shipping in 2025. Russia alone moved 8.1 percent. Iran added 3.9. Venezuela, even with Maduro’s capture in January and the US blockade, still managed 1.8. You cannot fine one barrel in seven out of the market and expect the price not to notice.

For three years the answer to that math was the shadow fleet, the discount, and a buyer in Beijing willing to pocket the spread. At peak discount in 2025, China was saving up to 28.8 million dollars a day buying sanctioned crude. That is not evasion at the margin. That is a parallel market with its own price, its own fleet, and its own logic.

The Hormuz shock broke the discount. When Gulf barrels vanished, the world stopped treating Russian crude as contraband to buy cheap and started treating it as supply to secure at any price. The discount became a premium. The shadow fleet stopped being a discount mechanism and became a delivery mechanism. Same ships. Opposite economics.

Chart 3. Sanctioned crude was roughly 14 percent of 2025 shipping flows.

The chain of causality, one link at a time

Walk it with me. This is where the consequences compound.

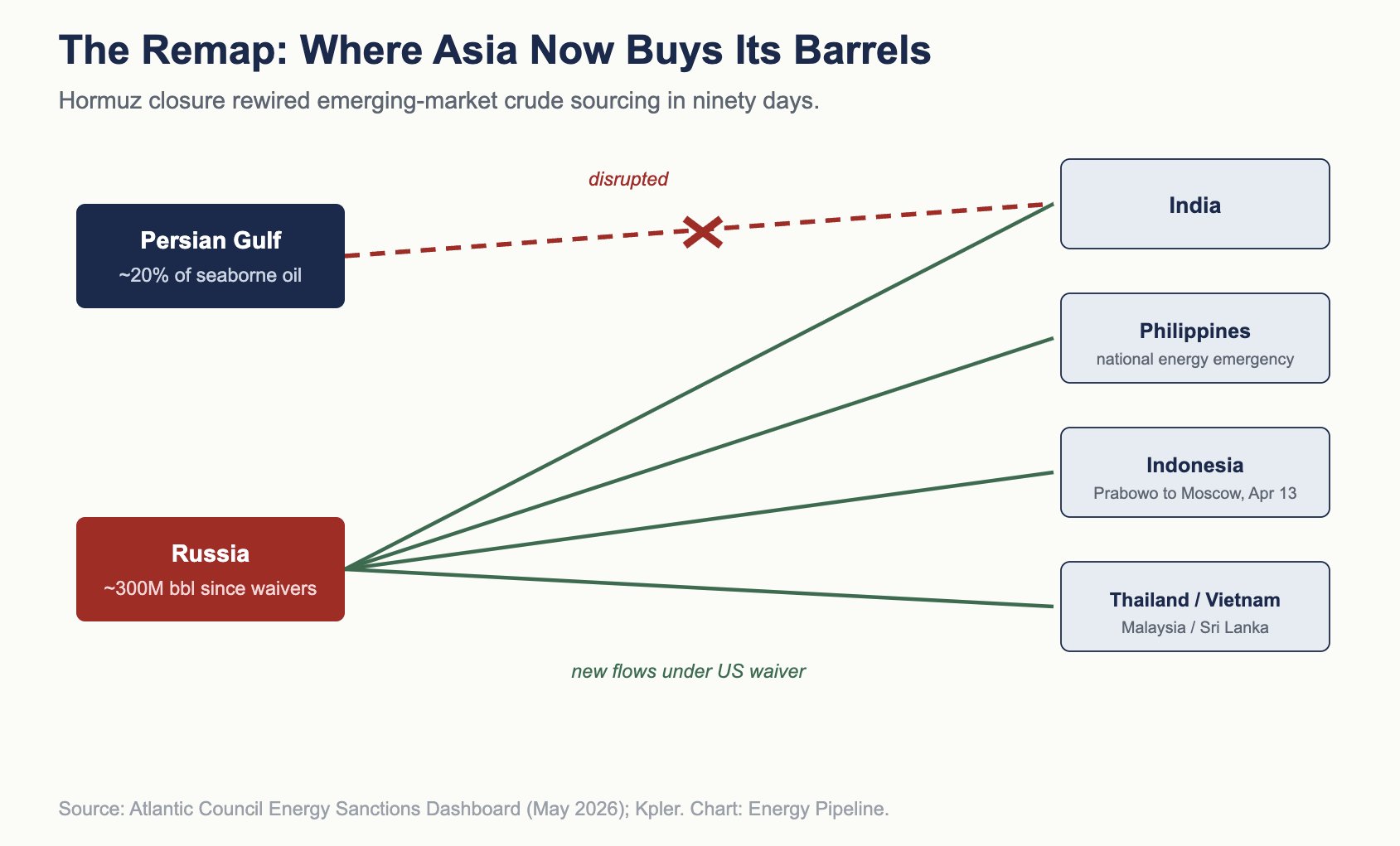

1. Hormuz closes. Roughly 20 percent of seaborne oil is suddenly unreliable. Asian refiners who built their diet around Gulf grades face a hole they cannot fill from inventory.

2. The United States waives its own sanctions on Russian crude. The instrument built to starve Moscow becomes the instrument that feeds Asia.

3. Russian export volumes surge. March imports of Russian crude rose about 41 percent over February, to levels not seen even before the 2022 invasion. Since the waivers, Russia has put roughly 300 million barrels back into the international market.

4. The buyer base widens. India returns to pre-sanction volumes and is openly lobbying to extend the waiver. Southeast Asia, a region that imported up to 96 percent of its crude from the Middle East, shows up as a brand new customer. The Philippines declared a national energy emergency. Indonesia went to Moscow and came home a buyer. Thailand, Vietnam, Malaysia, Sri Lanka are all in the queue.

5. New dependencies set like concrete. This is the link nobody in Washington wants to look at. A refinery that reconfigures for Russian crude does not switch back the morning a waiver expires. A government that signed an emergency supply deal with Moscow does not tear it up on a US press release. The waiver was sold as temporary relief. It is building permanent plumbing.

6. The discount inverts. With demand chasing a shrinking pool of available barrels, sanctioned exporters stop competing on price and start collecting a premium. Russia, the most sanctioned major exporter on earth, becomes the best-positioned seller in the market.

7. The enforcement tool loses its teeth. You cannot run maximum pressure on Iran with one hand while waving Russian cargoes through with the other and expect anyone to believe the threat. China noticed. For the first time, Beijing deployed its prohibition order, instructing its own companies to ignore US secondary sanctions outright. The mask of quiet compliance is off.

Seven links. Each followed logically from the last. None of them were the plan.

The enforcement problem, in one paragraph

None of this works without the ships. Transshipment, the cargo-to-cargo transfer at sea that launders a sanctioned barrel into a clean one, and the shadow fleet that carries it, vessels with opaque ownership that switch off their transponders or spoof their position, remain the load-bearing wall of the whole evasion structure. The West keeps sanctioning individual tankers and individual Chinese teapot refiners. FinCEN issued a fresh advisory to banks on the red flags of Iranian oil smuggling. Treasury rebranded the Iran campaign as Operation Economic Fury and pointed secondary sanctions at intermediaries in China, the Emirates, Hong Kong, Iraq, and Oman. All of it is real, and none of it has shrunk the fleet. You cannot out-designate a problem that grows a new shell company every week. Enforcement that is not coordinated across the G7 and is not aimed at the financial plumbing is theater with a press release attached.

FOR PAID SUBSCRIBERS

This is the part that matters for anyone with a barrel, a refinery, or a budget exposed to diesel.

Below the wall: three scenarios for the June 17 waiver cliff and how each prices through to Brent, Urals, and Brazilian diesel. The Global Economic Ripple, traced through Asia, Europe, and the one region the Atlantic Council dashboard ignores entirely, Latin America, where the realignment is quietly minting winners. And the single move I would make this week sitting on physical length or short diesel.

Who this serves: the operator deciding whether to hedge June and July diesel, the trader weighing Urals length, and the executive who has to explain to a board why a temporary waiver is a permanent risk.

Companion deck: 12 slides, including the discount-to-premium inversion mapped against the Hormuz timeline, and the Latin American barrel map most desks have not drawn yet.

Subscribe to read the full analysis. Free readers get The Signal each Monday. Paid and Founding readers get The Flow and The Horizon, the scenarios, and the deck.

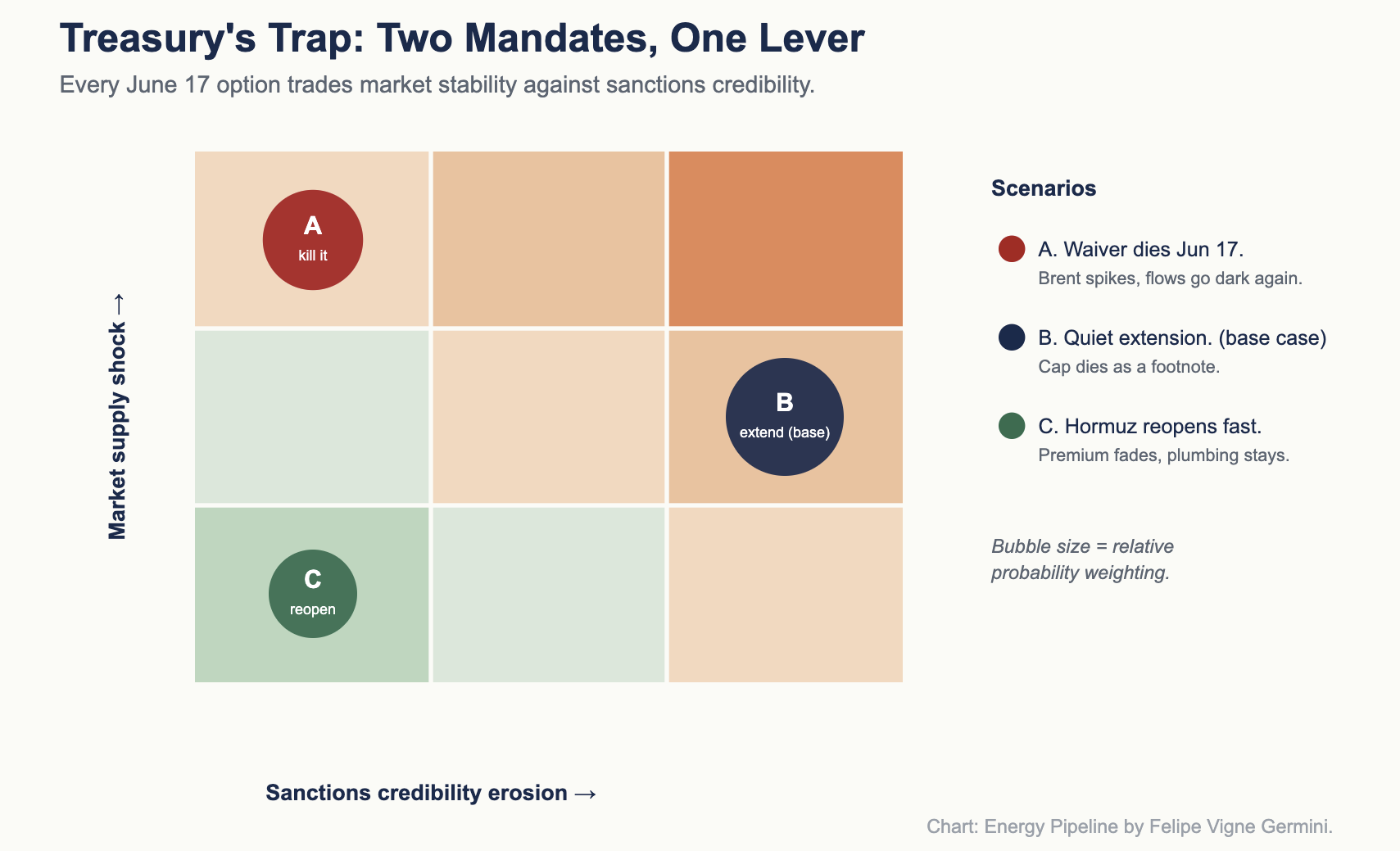

Alternative scenarios for June 17

Scenario A. The waiver dies on June 17. Rubio gets his wish. Treasury lets it lapse and returns to undiluted maximum pressure. On paper, credibility is restored. In practice, you have pulled 300 million barrels of relief out of a market still short Gulf crude. Brent spikes back toward the spring highs. India and Southeast Asia, told they cannot legally buy Russian, buy it anyway, because a fuel shortage is a domestic crisis and a US fine is a line item. Indian officials have already said as much. Expiry does not stop the flows. It moves them back into the dark, rebuilds the discount for China, and hands Beijing the spread again. Sanctions look tough and accomplish less.

Scenario B. The waiver is extended quietly, again. The most likely outcome, and the most corrosive. Washington keeps issuing thirty and sixty day extensions because the alternative is an allied recession. Each extension normalizes Russian crude a little more. Urals holds its premium. The price cap becomes a footnote nobody bothers to repeal. Moscow funds its budget at market prices while the West congratulates itself on a cap that no longer caps anything.

Scenario C. Hormuz reopens faster than expected. The ceasefire holds, Gulf volumes recover over the summer, and the supply panic drains out of the price. This is the bullish case for sanctions and the bearish case for Brent. Russian premiums collapse back to discounts as Gulf barrels return. But even here, the Southeast Asian relationships do not vanish. Indonesia and the Philippines learned a lesson about single-source dependence that no reopening unteaches. The flows shrink. The plumbing stays.

My weighting: B is the base case, A is the political tail risk markets are underpricing for June, C is the hope every importing finance minister is praying for and none can bank on.

Chart 4. Every option trades market stability against sanctions credibility.

Global economic ripple

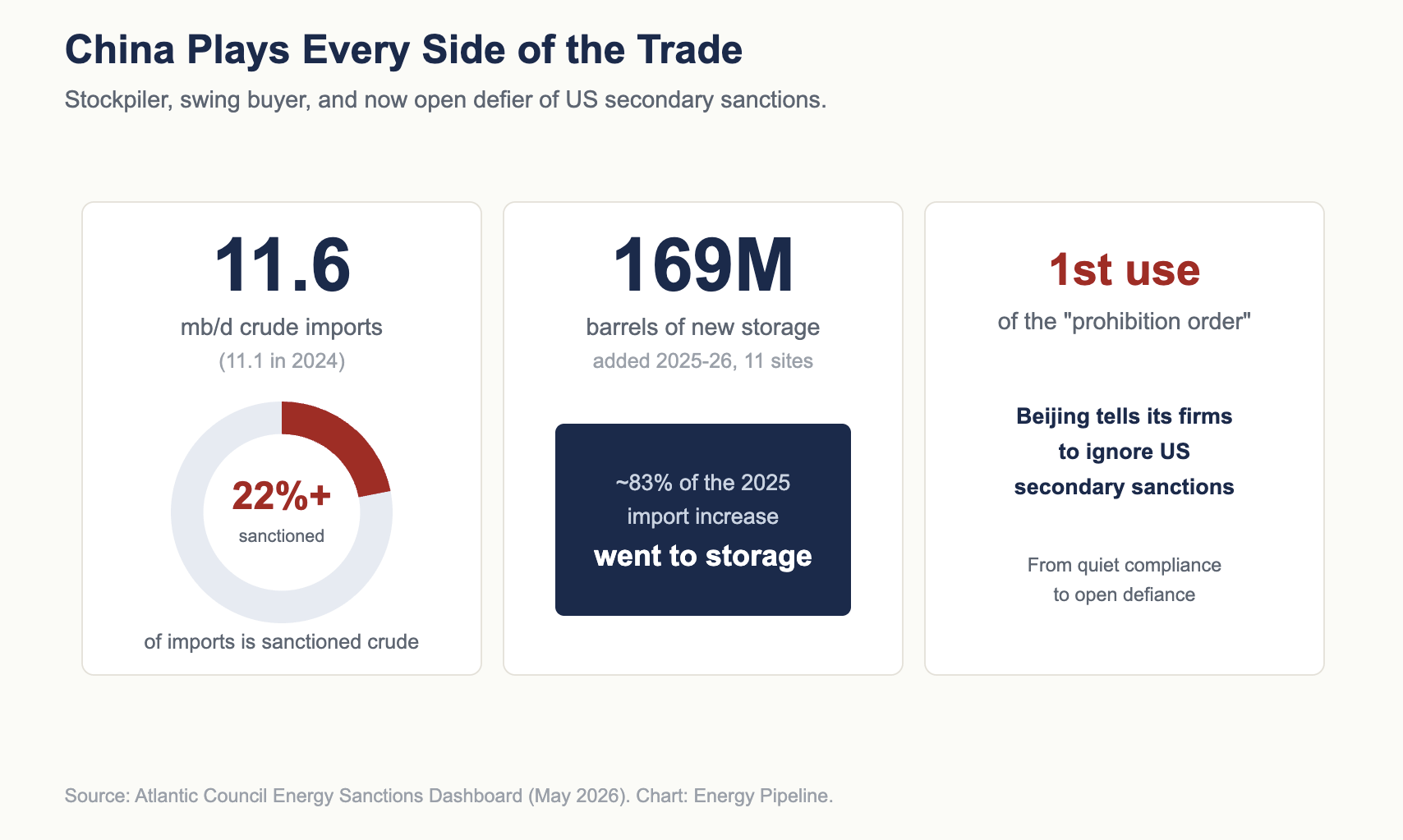

Asia. The epicenter. The region went from comfortable Gulf dependence to a frantic supply hunt in ninety days. Diesel and gasoline prices in the Philippines doubled in the first month of the crisis. Thailand, Vietnam, and Malaysia are exposed at 70 percent import reliance or worse. The structural shift is that Asian energy security now runs partly through Moscow, and that is a strategic gift to Russia no battlefield delivered. China, meanwhile, sat on 169 million barrels of fresh storage it built in 2025 and 2026 and is playing every side: stockpiler, swing buyer, and now open defier of US secondary sanctions. Watch the Chinese teapot refineries. They are the pressure point Treasury keeps designating and never quite closes.

Chart 5. China holds the storage, the volume, and now the willingness to defy.

Europe. The continent that built the price cap is watching it die and saying very little. The EU pushed toward a 44 dollar ceiling precisely when the market moved to a Russian premium, which means the cap is now a number with no buyers and no relevance. Brussels has two bad options: enforce a cap the market ignores and look impotent, or quietly let it lapse and admit the pressure is gone. Either way, the lesson is the one Europe should have learned in 2022. A sanction is a tool of pressure only when the sanctioned party has somewhere worse to go than you. Russia now has Asia.

Latin America. Here is the region the dashboard does not mention, and the one I watch most closely from Sao Paulo. The realignment is quietly minting winners across the Atlantic Basin. Every barrel of Gulf crude that does not reach Asia is a barrel someone else has to supply, and non-sanctioned medium and sweet grades gain. Brazilian pre-salt crude, already pointed at China, becomes more valuable simply by being clean, liftable, and politically boring. Guyana’s output looks better by the day. Argentina’s Vaca Muerta exports catch a tailwind.

I have brokered enough of these flows to know the arbitrage does not care about ideology, only about delivered cost. For a decade the diesel that clears the Brazilian market has been a contest between US Gulf Coast cargoes and, more recently, Russian barrels arriving through long, deniable supply chains. Close Hormuz, scramble the Russian diesel pool, and distort the Gulf Coast arb at the same time, and you remove the two reference points that Brazilian importers price against. The result is not a clean shortage. It is a wider, more volatile import parity that Petrobras either passes through to the pump or absorbs onto its own balance sheet for political cover. Either choice has a constituency that screams.

The other side of the ledger is diesel. Brazil is a structural diesel importer, and the global diesel complex is the most exposed product in this whole mess. With Russian diesel flows scrambled and the US Gulf arbitrage distorted, Petrobras faces the old, ugly choice between import parity pricing and political pressure to eat the spread. Watch the Brazilian pump. It is where a strait in the Persian Gulf turns into a line item in a Belo Horizonte trucking budget. And Venezuela, with Maduro gone since January and general licenses redirecting crude north, is being slowly reabsorbed into a US-facing supply orbit. The heavy barrel map of the hemisphere is being redrawn while everyone stares at Hormuz.

Chart 6. The plumbing being built now does not reverse on a press release.

The strategic read

If you want the one sentence I would put in front of a board: the waiver is not the story, the dependency is. Markets are trading June 17 as a binary, expiry or extension, spike or relief. That is the wrong frame. Whatever Treasury decides on the 17th, the structural fact is already set. A meaningful slice of Asian and emerging-market demand has been rewired to run through Russian crude, and that wiring does not reverse on schedule. The premium is the proof.

For the operator, that means treating Russian length as a market position, not a sanctions risk, and hedging diesel exposure into the third quarter rather than betting on a clean reopening. For the policymaker, it means admitting that a sanction you cannot afford to enforce is not a sanction. It is a bluff with a deadline. And for anyone in Brazil or the wider Atlantic Basin, the next eighteen months hand non-sanctioned producers a structural premium they did nothing to earn, and hand diesel importers a bill they cannot avoid.

The Atlantic Council ends its dashboard asking how Washington can stabilize markets without weakening pressure on Russia and Iran. After this spring, that question answers itself. It cannot. It already chose. The barrels chose for it.

Best Regards,

Felipe Vigne Germini is an energy executive, operator, and dealmaker with 25 years across the oil and gas value chain, from deepwater operations to physical crude and product trading in Brazil and Latin America. He writes Energy Pipeline, an independent newsletter on energy markets, geopolitics, and the business of moving barrels.