The Reopening Trap

Five variables that outlive the Hormuz headline

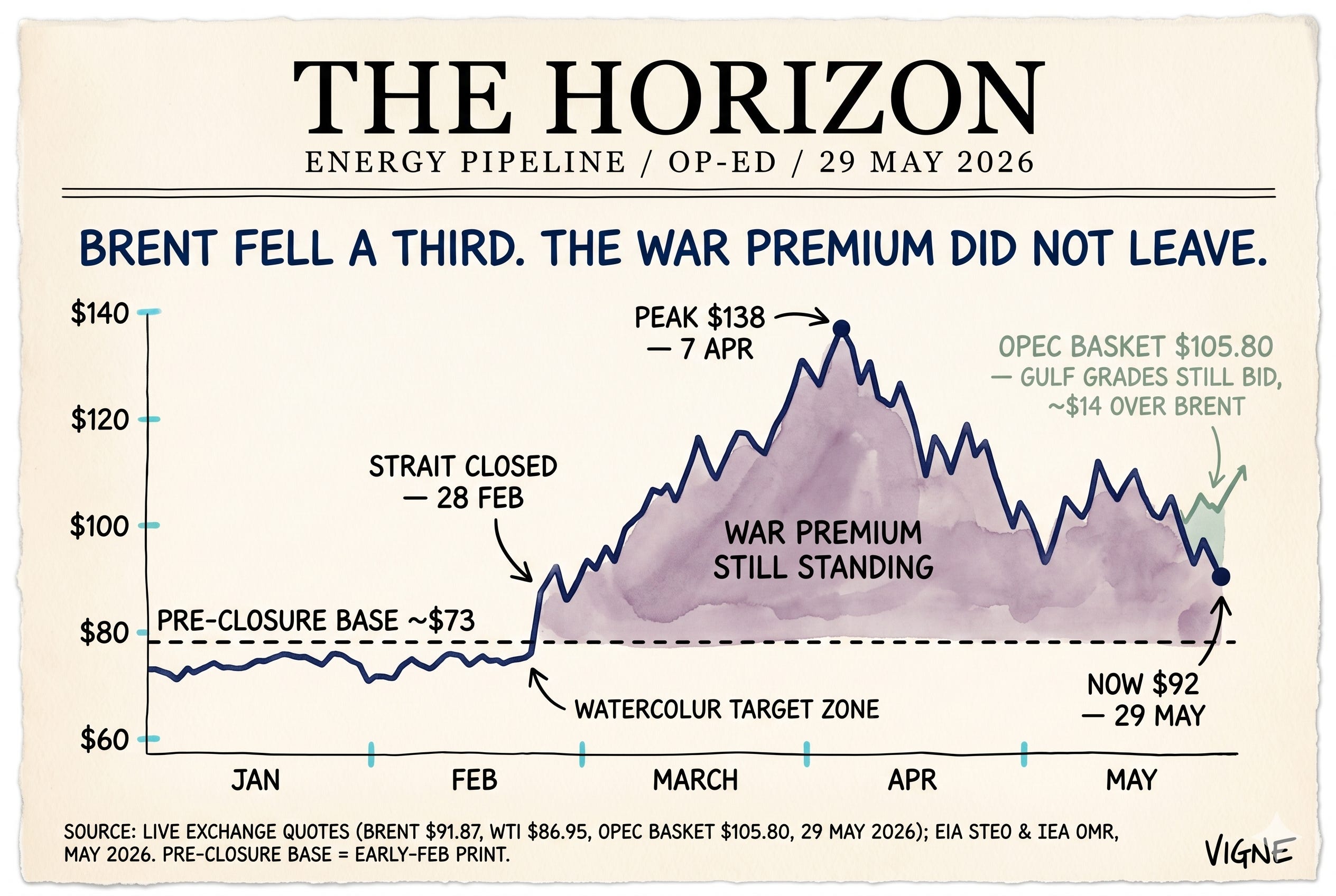

The desks have already buried the war. You can see it in the tape. Brent printed $138 a barrel on the 7th of April. Today it sits near $92. WTI is under $87. That is a third off the top in seven weeks, and the financial press is writing the obituary of this crisis with the enthusiasm of people who were short the whole way down and want company.

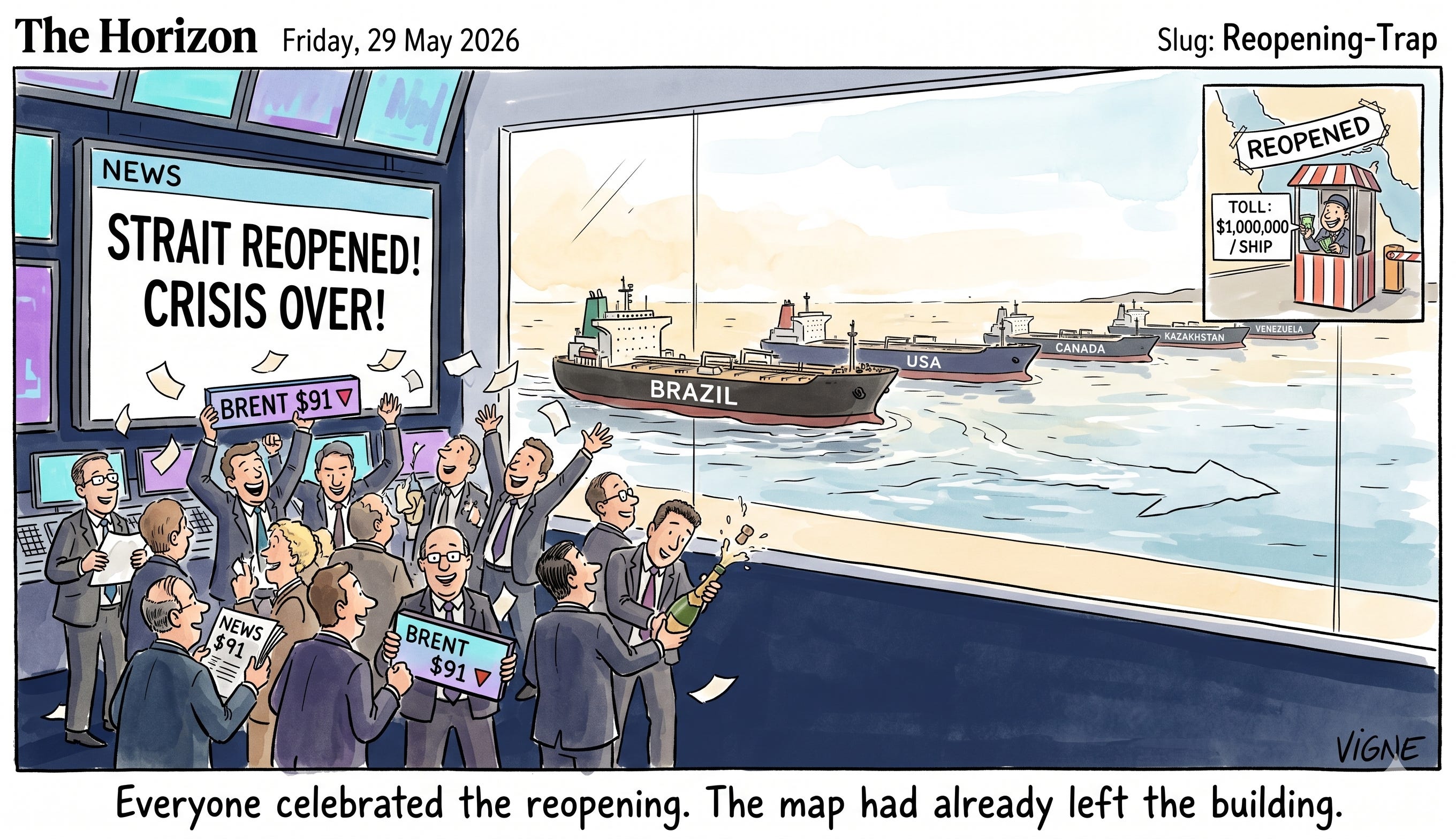

President Trump says the deal to reopen the Strait of Hormuz is “largely negotiated.” The screens lit green. The story writes itself from there. Iran blinks, the tankers sail, the premium bleeds out, and we all go back to arguing about the 2027 demand peak over lunch.

I have sat through enough of these to recognize the shape of it. The all-clear is the most expensive sound in this business.

Read Tehran, not Washington

Read what Tehran actually said, not what Washington announced. Iran’s own Fars agency called the reopening “incomplete and inconsistent with reality.” Iran still claims management of the strait. Iran still charges over a million dollars per ship to cross it. Sit with that number for a second. A waterway you must pay a seven-figure ransom to use is not open. It is a tollbooth wearing the costume of a trade route.

And here is the part the price action is missing. While the desk stared at the ceasefire ticker, the physical map of crude moved. It did not ask anyone for permission.

The hole, and what walked into it

Global supply fell another 1.8 million barrels a day in April, down to 95.1. Gulf output is running 14.4 million barrels a day below where it sat before the shooting started. Saudi Arabia, Iraq, Kuwait, Qatar, the UAE and Bahrain shut in 10.5 million barrels a day in April alone. That is not a rounding error. That is close to a tenth of the world’s oil sitting behind a closed door.

Into that hole walked the Atlantic Basin. Since February, crude exports from this side of the world have risen by 3.5 million barrels a day. The United States, Brazil, Canada, Kazakhstan and Venezuela are filling tankers and pointing them East of Suez, toward the refineries that used to drink Gulf barrels and now cannot get them. Brazil pumped a record 4.24 million barrels a day in March. Pre-salt is now roughly four fifths of the country’s output. The barrels I spent a career arguing were strategic are, this quarter, the marginal barrel keeping Asian refineries lit.

I will say the quiet part about my own country out loud, because it cuts both ways. Brazil sold a record 1.92 million barrels a day abroad last year and earned close to $45 billion doing it. China took about 44 percent of that. Concentration like that is a strength when Beijing is desperate and a liability the day it is not. The pre-salt is low cost and lower carbon, which is precisely why buyers under pressure reached for it first. But a producer that lets a single customer take nearly half its export book is renting its pricing power, not owning it. The opportunity for Brazil this year is to convert a crisis windfall into diversified, contracted demand before the windfall ends. That window is open now. It does not stay open.

Figure 1. The unwind that is not an all-clear. Source: live exchange quotes (Brent $91.87, WTI $86.95, OPEC basket $105.80, 29 May 2026), EIA STEO and IEA OMR (May 2026).

The cartel lost a cylinder

The group that was supposed to be the shock absorber just lost one. The UAE walked out of OPEC on the first of this month. Abu Dhabi held real, usable spare capacity. With it gone, the cushion the market quietly leans on shrinks from a forecast 3.8 million barrels a day to roughly 2.5 for 2027. The safety net got smaller in the same season the house caught fire.

The wrong question, and the right one

So the question that matters for Monday is not the one the cable channels are asking. “Will the strait reopen” is the wrong question. It is a binary the market has already priced as a yes, which is exactly why it is no longer where the money is.

The right question is colder. What survives the reopening?

Which part of this premium is permanent. Which barrels never sail home. Which producers were just handed pricing power they have no intention of returning. Which buyers spent ninety days rebuilding their supply chains around the Atlantic and will not tear them out because a politician held a press conference.

That is the trade for next week. Not the headline. The residue.

This is where the free read stops. What follows is written for the operator who has to act on Monday, not react to it: the trader, the refiner’s supply manager, the treasurer hedging a fuel bill, the executive who has to explain the curve to a board.

Below the wall: the five specific variables I am watching when the desks open Monday, the two ceasefire outcomes that would still leave Brent structurally bid, the single Atlantic Basin position I would not be caught without, and the freight and insurance signals that tell you the truth before flat price does.

This week’s companion deck: an eight-slide executive briefing for paid subscribers, including the “permanent premium” decomposition and the Brazil-as-swing-barrel map you can drop straight in front of your own board.

Energy Pipeline runs on two tiers. The Signal, at $8 a month, keeps you current. The Strategic tier, at $25 a month, gets you the flagship Wednesday analysis, the Friday Horizon in full, and the decks. Pick the one that matches how much of your P&L moves with this market.