UK Two-Front Shock

Why the UK Is the Most Exposed Energy Importer in Europe Right Now

The Horizon | Friday, May 8, 2026 | Scenario stress-test edition

A note before you read. What follows is a forward-looking stress-test scenario, not a chronicle of confirmed events. The UK structural exposures I describe (the North Sea run-down, the Qatar-via-Hormuz import architecture, the refining slate configuration, the sterling pass-through) are real and verifiable from public sources. The Iran-war trajectory, the Hormuz disruption to five percent of pre-war traffic, the post-Khamenei succession dynamics, and the EU twentieth-package enforcement timeline are scenario inputs I am using to stress-test how the UK energy import complex would respond if all of them unfolded simultaneously through Q2 2026. If you opened this on May 8 thinking you missed a news cycle, you did not. Read this as a what-if, written the way I would brief a counterparty before a difficult quarter.

I have priced cargoes from the Persian Gulf into refineries for years. The position the United Kingdom is now standing in is one I recognize. It is the position you find yourself in when your domestic supply has run down to a maintenance trickle, your gas import portfolio routes through a chokepoint that just closed, and your refining base was built on the assumption that the chokepoint would always be open. I have watched Brazil sit in versions of this position three times since the early 2000s. The fix is never quick and the cost lands in the operating margin before it lands at the pump. The UK is now learning that on its own clock.

No major European economy is worse positioned for a simultaneous Gulf and Eastern Europe energy shock than the UK, and the structural reasons have nothing to do with the current government.

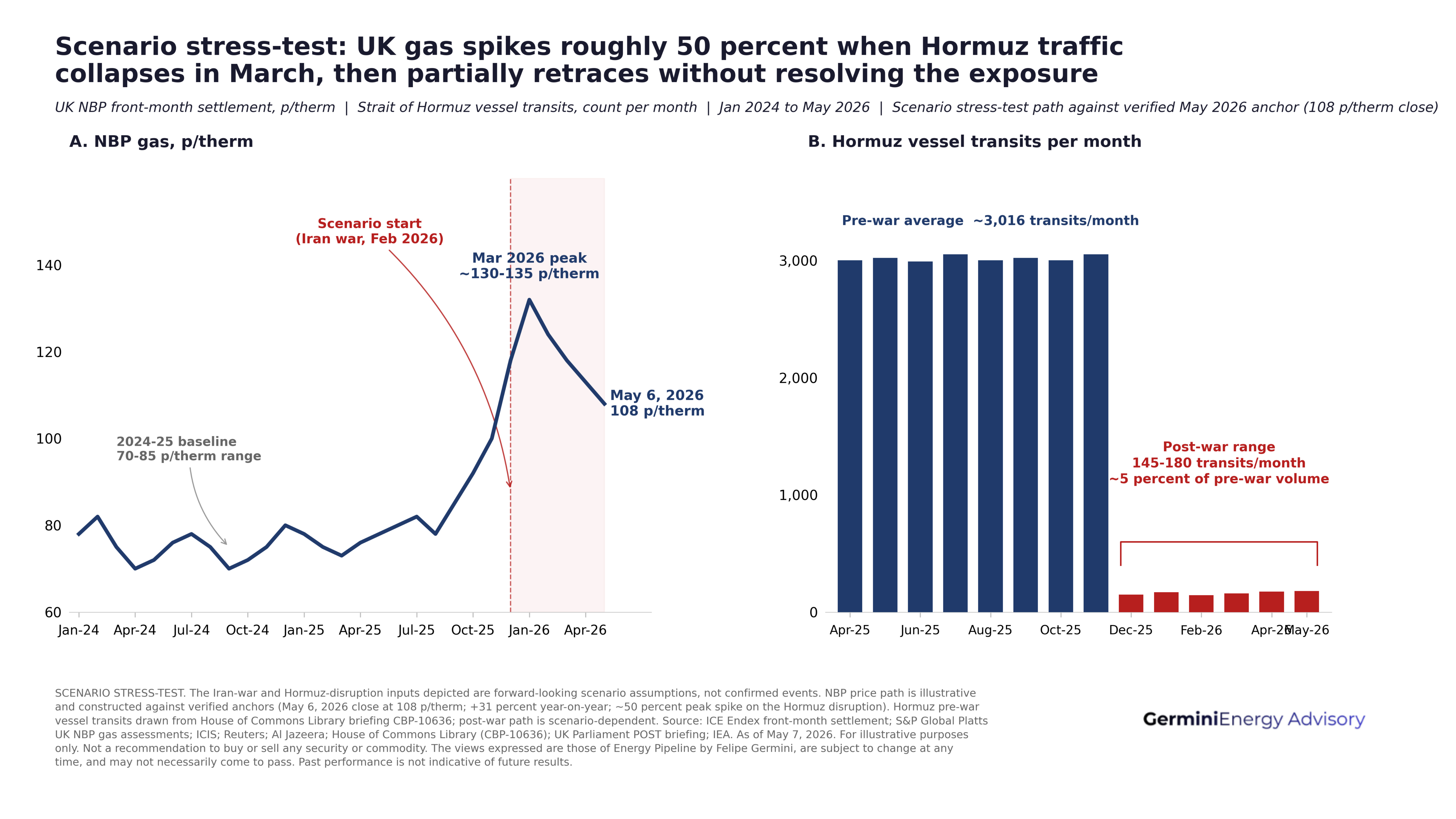

The texture of the new normal is visible in the cargo schedule. The Strait of Hormuz reopened to about five percent of its pre-war traffic last week. Then a French container ship took a hit on Tuesday. Then the IRGC-Quds command, which has run the operational picture in the Gulf for at least a decade and which retained its operational autonomy through the post-Khamenei succession process, issued another statement on Wednesday saying transit will be ensured. Anyone who has worked counterparty meetings out of Dubai or Doha for the past ten years knows the supreme leader’s office never controlled the operational picture in the strait. Khamenei’s death did not change that. It revealed it. Ten weeks into the air war on Iran, the chokepoint is functioning as a managed valve, with the United States escorting some traffic, Iran threatening selectively, and global insurers pricing in war risk that is no longer transient.

In Europe, the headlines have been on the Brussels announcement of the EU’s twentieth sanctions package against Russia, the LNG tanker maintenance ban, and the rollover of the United States waiver on seaborne Russian crude through May 16. Both wars are now in their compounding phase. They are no longer separate stories. The country that gets squeezed hardest by the combination is the United Kingdom, and the reason is structural rather than political.

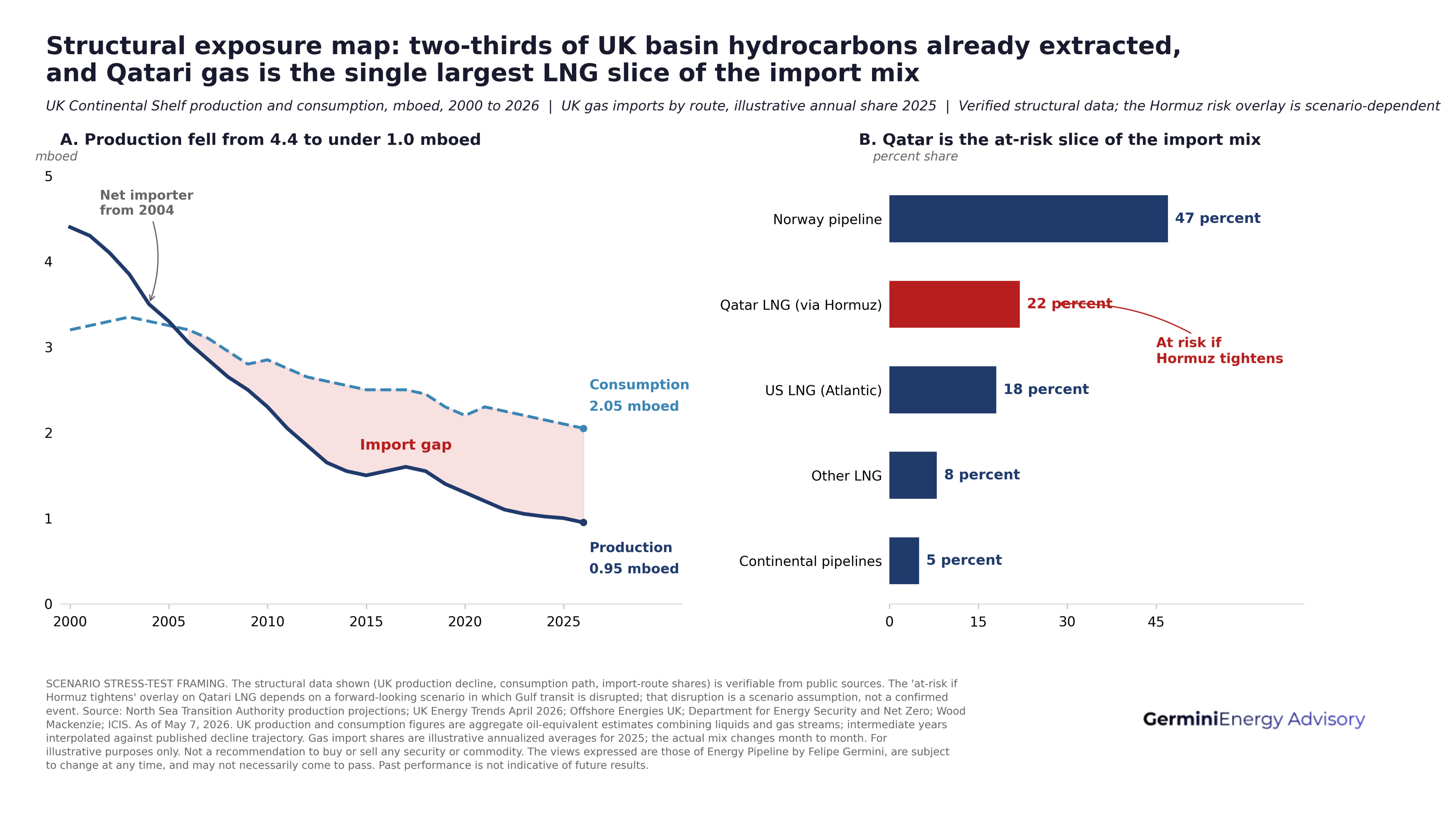

I started my career cementing wells. You learn to read the shape of a basin from the inside. When investment falls below the maintenance threshold, the basin is coasting on residual production and there is no recovery without a price signal large enough to reactivate idle drilling capacity. The UK has been past that point for several years. Production fell from a peak of 4.4 million barrels of oil equivalent per day in 2000 to about 1 million in 2025. Industry analysts now expect 2026 to be the last calendar year that the basin clears the 1 million boe/d threshold. Investment will fall below 3.5 billion dollars this year, the lowest real-terms commitment to the basin since the 1970s. The North Sea Transition Authority’s own projections put remaining recoverable resource at 65 to 75 percent of original recoverable, depending on the price assumption, with gas production specifically set to be roughly half of 2025 levels by 2030 even with new drilling. Brownfield work continues at Rosebank and Cambo. Those volumes are timing-shifted into the late decade and do not rescue the next eight weeks. What you have is a basin that imports nearly everything that moves through a pipeline or a tanker, with a domestic supply curve that is structurally falling rather than holding.

The geometry of the import portfolio is the second exposure, and it sits closest to my professional ground. I have sat across the table from Qatari counterparties on cargo terms. Anyone who has negotiated lift schedules out of Ras Laffan knows the export choreography is one of the most tightly run in global energy. When the main corridor closes, you re-route through the Cape, absorb the freight differential, and pay the premium until something gives. The Isle of Grain, South Hook, and Dragon LNG terminals were built between 2005 and 2009 to bring Qatari molecules into the British grid. That import architecture is now sitting on the wrong side of a closed strait. When Hormuz traffic collapsed to five percent of pre-war volumes on March 4, around a fifth of global LNG supply went off the board, and UK gas prices ran up roughly fifty percent before retracing. NBP closed at 108 pence per therm on May 6, still about 31 percent above year-ago levels. The substitute supply exists in the Atlantic basin. I have priced Atlantic basin LNG into Brazilian terminals for years and the freight differential against Qatar runs around two dollars per mmbtu most quarters. That is not catastrophic on a single-cargo basis. It is catastrophic across a winter when every other Atlantic basin importer is bidding for the same molecules.

The third exposure is the refining slate, and this is where Brazil’s experience matters most. The five major UK refineries, Phillips 66 Humber, Prax Lindsey, ExxonMobil Fawley, Valero Pembroke, and Petroineos Grangemouth, were built and configured around a Middle Eastern crude diet. Brazil’s refining base was never built on that assumption. Brazil never had the luxury of a stable Gulf supply, and as a consequence the Brazilian refining slate has run a multi-source diet for thirty years. We figured out how to flex between Middle Eastern grades, West African medium-sweets, USGC light tight oil, and our own pre-salt barrels because we had to. The UK refineries are now learning that their hydrocrackers, configured for Arab Light yields, do not flex cheaply. When you switch a hydrocracking complex to Norwegian, West African, or Brazilian Tupi and Búzios cargoes, you lose yield on the high-value product slate. My estimate sits at the four-to-seven dollar per barrel margin compression range based on what I have seen in Brazilian refinery operations on similar substitution cycles. The compression is asymmetric. Pembroke and Fawley take the deeper end. Grangemouth has more flexibility on the FCC and absorbs the shallower end. Three more weeks of Hormuz traffic at five percent and the Pembroke and Fawley complexes will be running off intermediate-distillate substitution slates that were designed for emergency, not as a base case.

The forward question for the UK is how these structural exposures compose with what is happening in the cargo schedule over the next eight weeks.

This is for the UK utility CFO who needs to brief their board on why the next eight weeks decide their hedging strategy through 2027, and for the allocator who is looking at this map and wants to know where to put 100 million dollars.

Below the cut: the political read on what the current government can and cannot do, the week-in-review on the post-Khamenei Iranian decision channel and the EU 20th-package enforcement question, how I would size three positions on this view, the three-scenario probability matrix for the next eight weeks, the variables I am watching with the thresholds that flip the call, the strategic calls per actor type, and the single number that tells you which scenario is unfolding four to six weeks before the price catches up.

Paid subscribers also receive this edition’s presentation pack, eleven slides covering the scenario probability matrix, the UK exposure decomposition by import route, and the variable-watch dashboard, formatted for boardroom use.

Upgrade to read the full edition.