Two Waivers in Two Months. Sanctions Just Became a Negotiating Chip.

The Signal | Monday, May 18, 2026 | Premium Edition Pack The architecture the market priced as permanent is now a chip. The book that assumed otherwise is wrong.

Two waivers in two months, on producers the United States spent the better part of a decade trying to throttle. A third producer, Venezuela, sitting under a general license issued before the war was even seventy days old.

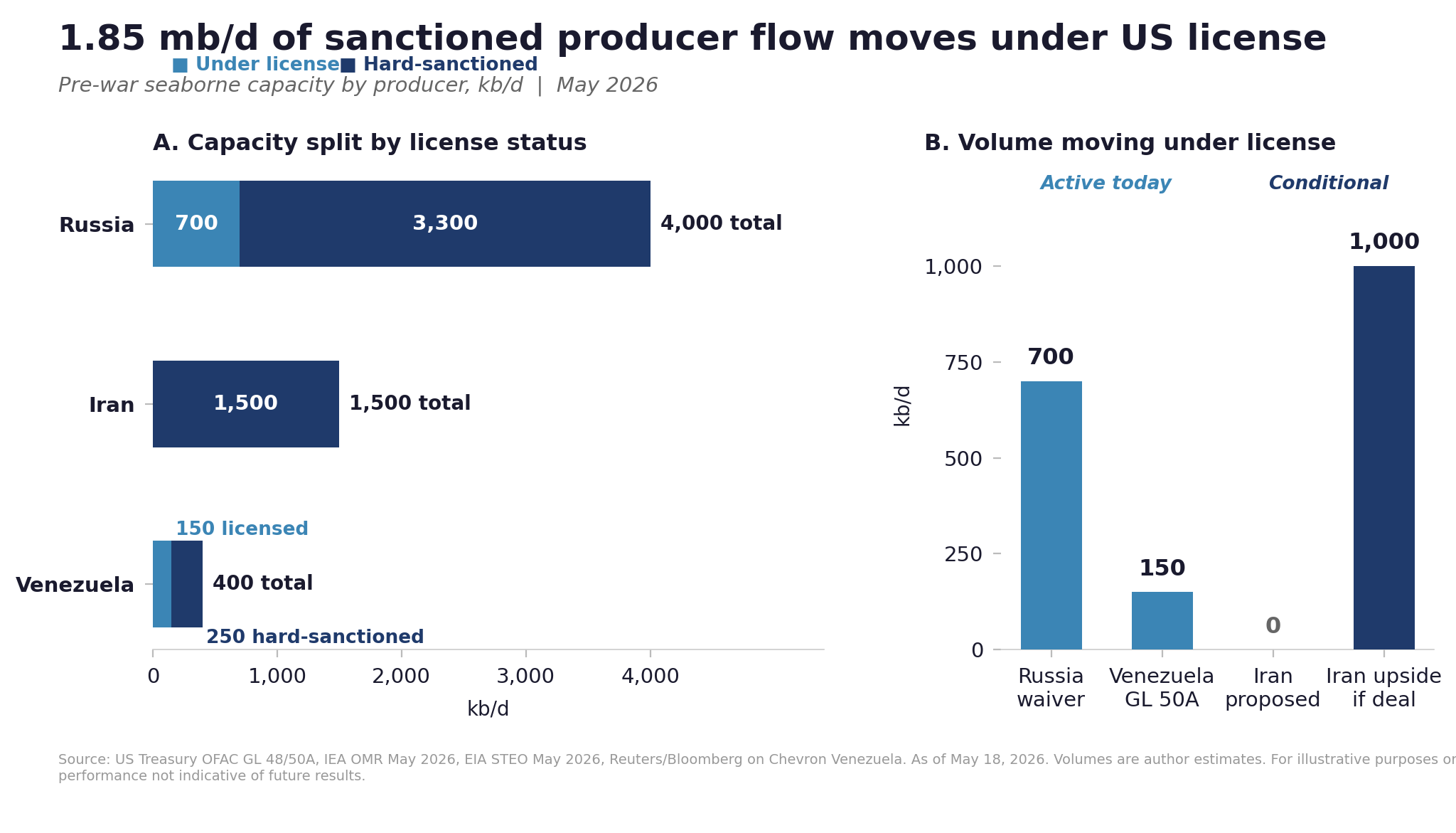

The procedural details are dull and the architecture they describe is not. The Office of Foreign Assets Control issued General License 50A on February 18, naming six majors, BP, Chevron, Eni, Repsol, Shell, Maurel & Prom, and authorizing transactions tied to Venezuelan upstream operations. By mid-March, US Treasury had waived sanctions on Russian crude already loaded onto tankers, roughly five to six days of normal Strait of Hormuz throughput. That waiver was extended to April 11. Then extended again to May 16.

The market is still pricing the sanctions architecture as if maximum pressure is the default and waivers are deviation. That has the geometry backwards. What 2026 has done, in plain sight, is reclassify sanctions from policy instrument to negotiating chip. Once something is a chip, it is on the table.

The Russia waiver tells you the price of the chip

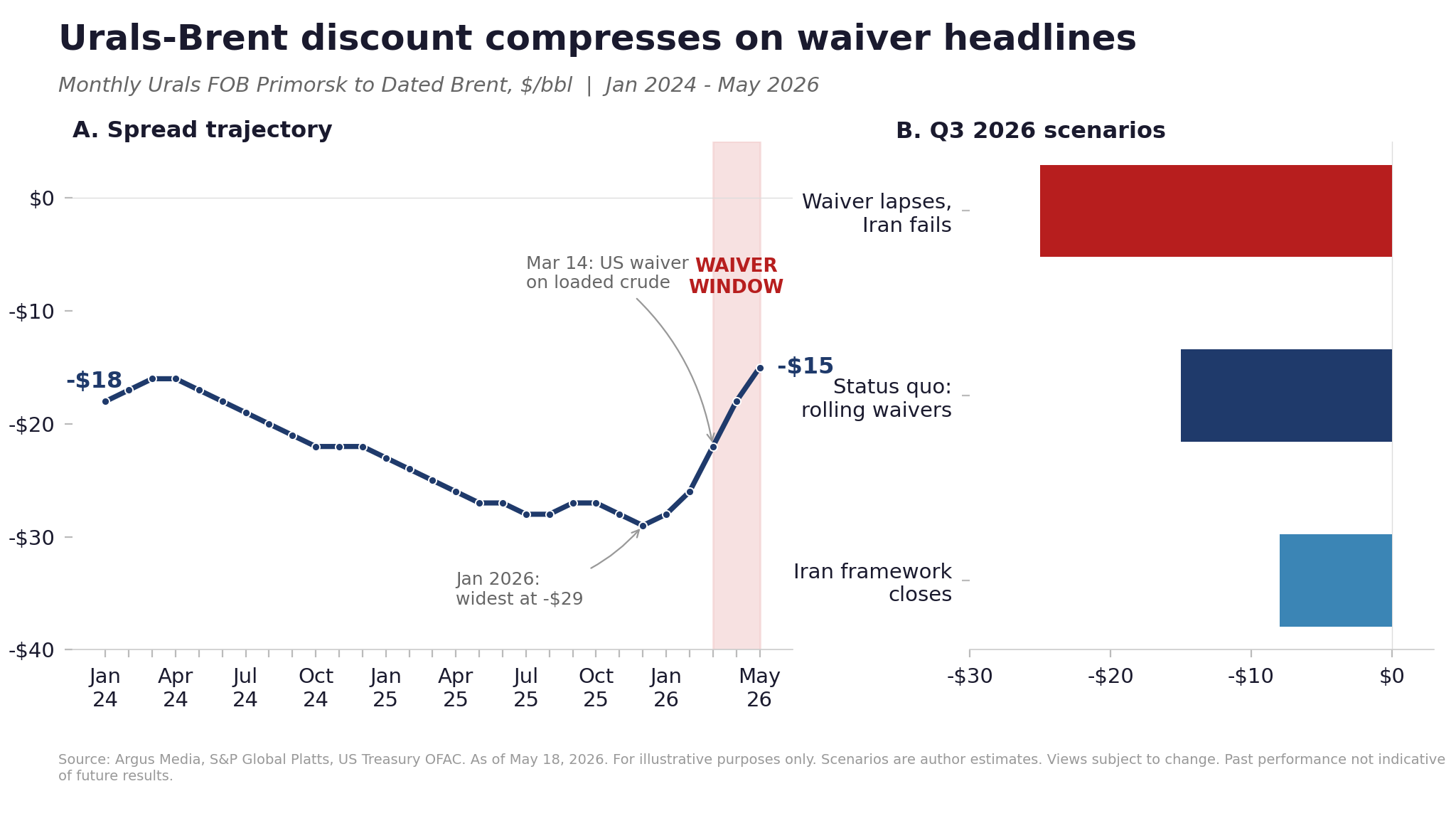

Start with the part of the architecture that has been live the longest. The Russia oil sanctions framework built between 2022 and 2025 was sold to the market as permanent. The G7 price cap. The EU sixth, eighth, twelfth, fourteenth packages. The shadow fleet designations that hit 623 vessels in 2025 alone. The Urals discount that sat at twenty-eight dollars below Dated Brent as recently as January. A trade book that read all of that as durable structure was a defensible book. It is not a defensible book today.

The March waiver did one specific thing. It allowed cargoes already on the water, already underwritten by Western P&I clubs before the Hormuz event reset insurance pricing, to deliver into refineries that needed the diesel and the gasoil. The Treasury framing was operational. The signal was strategic. Sanctions that produce a barrel shortage in your own refining base will be relaxed when the shortage becomes inconvenient enough. Anyone running a Russia short on the assumption that the price cap would expand rather than contract has watched the Urals discount compress on every extension headline.

What the waiver does not do is restore Russian crude to the pre-war architecture. The shadow fleet is still under EU pressure. Forty percent of last year’s Russian tonnage is on a sanctions list somewhere. P&I cover is still expensive. The waiver is conditional and explicitly time-bound. What it has done is teach the market that the cap is negotiable in both directions, and the direction depends on whose refineries are short.

If you have been pricing Russian flows as if the cap is policy, reprice. The cap is now an option that Washington holds and Washington exercises situationally.

The Iran proposal is not a deal yet. It is already a price.

Iran’s Tasnim news agency reported on May 18, citing a source close to the negotiating team, that Washington had floated a temporary lift on Iran’s oil sanctions until a final agreement is reached. Washington has not confirmed. Tasnim is Iranian semi-official media with a structural incentive to publish anything favorable to Tehran’s negotiating position, and the careful reader should treat the single-source report as a tradable headline rather than a confirmed framework.

The headline moved Brent six dollars in a session anyway. The size of the move on a single unverified source is itself the asymmetry the careful reader should price. That is how thin the consensus is on the durability of the sanctions stack.

The fourth round of talks in Oman on May 11 closed with both sides calling it “difficult but constructive,” which in negotiating language means there is a framework on the table and neither side wants to be seen as the party that walked away. The Axios reporting on the one-page memo describes four moving pieces: a moratorium on Iranian uranium enrichment, a lift on US oil sanctions, a release of frozen Iranian funds, and the part the market cares about, a reopening of the Strait of Hormuz under terms acceptable to both navies.

That last piece is what moves the curve. Iran’s lifted oil flow, on its own, is roughly 1.5 mb/d of incremental seaborne crude into Asia, mostly heavy sour grades that compete with Venezuelan Merey and with Saudi Arab Heavy. The flow is not the trade. The Hormuz reopening is the trade. Aramco’s twelve million barrels of nominal capacity, the East-West pipeline at seven million, the Iraqi southern grades, the Kuwaiti exports, all of it sitting behind a strait that has been functionally closed since February 28. Lift the strait and the supply side of the chart redraws in three weeks. Leave the strait shut and Iranian crude is a sideshow.

Trump’s Truth Social post on Sunday, “Clock is Ticking,” read like pressure on Tehran. Read it the other way around. The clock is also ticking on Aramco’s tank tops, on Indian and Chinese refining margins, on the war-risk premium that has lifted P&I cover by 60 to 220 percent depending on hull and routing.

The administration that offered the waiver is also under time pressure, and that is the asymmetry the market is not pricing. Hormuz remaining shut into Q4 costs Washington more than it costs Tehran. Tehran has spent two decades operating under sanctions architecture. Washington has spent ten weeks watching its own refining margins, its Asian alliance economics, and its midterm political clock tighten. The deal asymmetry runs the way most commentary assumes it does not.

Venezuela is the tell

The Venezuela story is the easiest to read because the architecture is older and the moves are more visible. General License 50A reauthorized Chevron, Eni, Repsol, BP, Shell, and Maurel & Prom to operate inside their existing projects. General License 48 reauthorized the technology and services transfers that make those operations work. Chevron is exporting roughly 150 kb/d under that framework. PDVSA itself is still embargoed. The structural sanctions remain.

Read it as a template. Washington has built a sanctions architecture that can be selectively reopened at the project level, at the company level, at the cargo level. The blanket framework remains in place. The exceptions are surgical and reversible. The system is designed to be relaxed without being repealed. That is the architecture coming to Russia. That is the architecture coming to Iran if a deal closes. Permanent sanctions are no longer the default state. Managed sanctions are.

For an operator working physical product flows, the legal status of counterparties has shifted from static to case-by-case. Cargoes that were untouchable in 2024 may now be addressable under specific license. The compliance overhead is heavier. The documentation trail is longer. The timing is political rather than commercial. This is descriptive of what the licensing architecture has actually changed; readers acting on any of it are on the hook for their own counsel and their own KYC, and the editorial is not a substitute for either.

The durability case deserves an honest hearing

There is a coherent reading of the same evidence that says nothing structural has changed. The Russia waiver covered cargoes already on the water and nothing else. The Iran proposal is unconfirmed by Washington. Venezuela’s general licenses have been pulled before, including in early 2025. From that vantage, the three waivers are tactical operational exceptions, not a regime shift. The trade book reverts to the 2024 posture and the careful reader stays positioned for renewed maximum pressure into year-end.

The case against that reading rests on three things. The speed of the policy reuse, two waivers and a general-license package inside ninety days. The publicness of the Iran proposal, which Washington has not denied even as it has not confirmed. And Treasury’s institutional preference for surgical exceptions over outright repeal, which is visible across three different administrations and four different sanctions stacks. The reader who holds the durability view should price for a regime snap-back in Q3. The reader who holds the managed-sanctions view should price for continued partial relaxation with policy reversal as a tail risk. The editorial is built for the second view. The first deserves to be in the book.

What the trade book looks like if you take this seriously

A few specifics for the reader who has to position rather than comment.

On the curve. The forward Brent curve is still pricing tightness through late 2026 and easing into 2027. That curve embeds a base case that Hormuz reopens by Q3 and that Iranian and Russian volumes rebuild slowly under residual sanctions friction. The reflexive bull and the reflexive bear are both wrong because the curve is currently pricing neither outcome, just a slow muddle that may not exist. A book that takes the managed-sanctions view positions short front, long back, on calendar spreads into Q4, sized to survive a single-headline reversal.

On Urals differentials. The Urals-Brent spread sat at minus twenty-eight in January, compressed to roughly minus fifteen by mid-April on waiver headlines, and has stayed there. A formal Iran deal that includes Hormuz reopening tightens that spread further toward minus eight or minus ten. A deal collapse blows it back to minus twenty-five. The structure: long Urals-Brent flat into Q3, stop at minus twenty-eight, target minus eight. Sized smaller than a 2024 conviction trade because the binary on the Iran framework is real and unhedgeable through the headline.

On freight. War-risk premiums on VLCC Hormuz transits, as quoted into the Lloyd’s market, jumped from 0.125 percent to between 0.2 and 0.4 percent of hull value. P&I cover was cancelled on March 5. That structure does not unwind on a waiver headline. It unwinds on physical reopening of Hormuz, on insurance market reassessment, on the absence of a second incident inside the strait. Even if a deal closes this quarter, freight rates remain elevated through the second half of the year. The structure: long TC18 calls into October. The freight book is a longer-dated trade than the crude book.

On Brazilian arbitrage. The USGC-Santos MR route is a direct beneficiary of the structure above. ULSD ex-Houston into Suape or Santos via 38kt MR, priced off TC18, has held a workable arbitrage even on weaker spreads, with Middle East barrels delayed and global freight elevated. The window is narrower than 2024, but it is open in a way that surprised most analysts in February.

On counterparty selection. The most important shift is the cleanest to miss. A counterparty list that was static for three years is now dynamic. Russian-origin barrels under license, Venezuelan barrels under license, Iranian barrels potentially under license. Each carries paperwork, compliance overhead, and reputational drag. The operators that built compliance muscle into the trade in 2023 and 2024 are positioned to read the relaxation as it happens. The operators that simply blocklisted three flag states for ease of administration are going to spend the second half of 2026 catching up.

The risk on the other side

The architecture is reversible. That is the discipline.

A Russian waiver that expires on May 16 and is not renewed pushes the Urals discount back to minus twenty-five inside a week. An Iran framework that collapses on enrichment compliance leaves Hormuz shut and Brent retesting one hundred and twenty. Venezuela’s general licenses are reviewed by OFAC on a rolling basis and have been pulled before. None of this is permanent. None of this is durable. The waivers are exactly what Washington calls them, temporary measures tied to specific outcomes.

What that means for the trade book is straightforward. Position size has to reflect the optionality on both sides, not just the direction of the most recent headline. A book sized for a Iran-deal-closes scenario that does not close will lose more than a book sized for cap-extension that does not extend. The right size is smaller than either reflex would suggest, with longer-dated exposure structured to survive a reversal.

The framework also creates a new political risk that did not exist when sanctions were policy. Sanctions as policy are slow to write and slow to repeal. Sanctions as chips can be rewritten in a press conference. The market that priced regulatory durability has lost it. The trade now has to price the half-life of an administration’s negotiating position, which is a much shorter half-life than statute.

This is not a complaint about the architecture. It is logically coherent and it gives Washington positions in talks that it would not otherwise hold. From a free-market posture, it is in some ways an improvement over the blunt instrument of total embargoes. But it is not the architecture the trade book was sized for, and there is no point pretending otherwise.

The Signal

Two waivers in two months is not a coincidence. It is a structural shift, executed deliberately, applied to the most politically charged producers in the world. The sanctions architecture that defined 2022 to 2025 has been overwritten. What replaced it is more flexible, more reversible, and explicitly conditional on what Washington wants out of the producer at any given moment.

For the operator, the dealmaker, the trader, the refiner, the implication is the same. The list of barrels you can touch is longer than it was six months ago. The paperwork is heavier. The timing is more political and less commercial. The book sized for permanent maximum pressure is wrong. The book sized for permanent relaxation is also wrong.

The book sized for managed sanctions, partial, conditional, reversible, deliberately ambiguous, is the book that survives 2026.

That is the Signal this week. The rest of the week’s editorials will build from it.

Paid subscribers receive the full presentation pack for this edition. Ten slides covering the sanctions architecture map, the Russia-Urals discount trajectory under each waiver scenario, and the four-quadrant counterparty playbook for relaxed-but-reversible regimes.

Upgrade to read the rest of the week’s editorials and receive the slides: fgermini.substack.com

About the author

Felipe Germini is a Brazilian energy executive with 25+ years operating across the full oil and gas value chain, from rig sites and production operations to trading desks, boardrooms, and geopolitical analysis. He built his career at Schlumberger, rising to Country Managing Director for Brazil with full P&L responsibility over deepwater and onshore operations. He later moved into downstream commodities, M&A advisory, and executive consulting, working across Brazil, Latin America, Russia, Africa, the Middle East, and the United States. An IBGC-certified board member, he has advised on operational turnarounds, corporate divestments, and cross-border business development at the C-suite level. Today, Felipe is the Founder and Managing Director of Germini Energy, a boutique brokerage specialized in crude oil and refined products into Brazil and Latin America. He publishes Energy Pipeline by Felipe Germini on Substack.